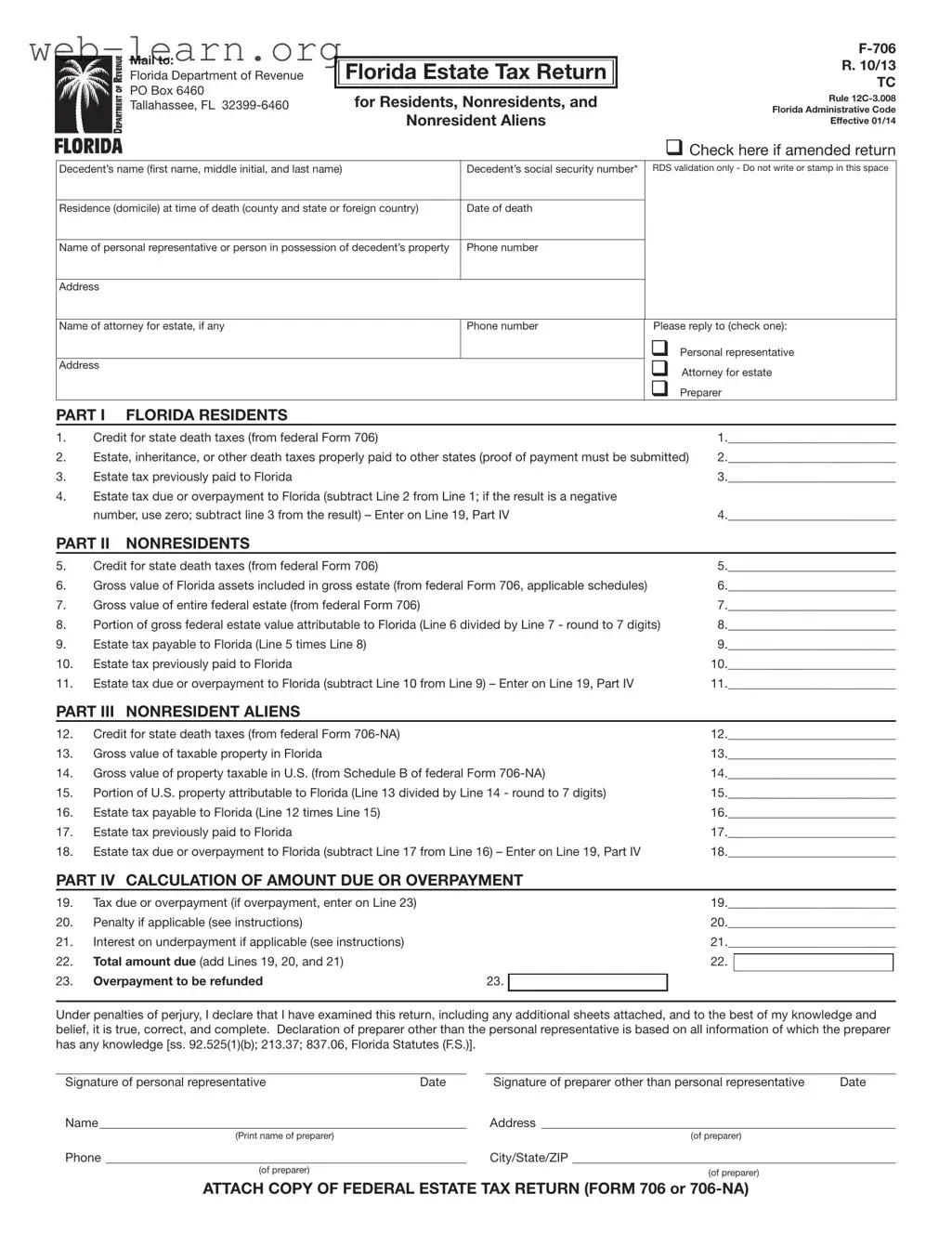

The Florida F 706 form serves as a crucial document for managing estate tax obligations in the state of Florida. This form is necessary for estates that are subject to federal estate tax filing requirements and must be filed by the personal representative of the decedent. The form collects essential information, including the decedent's name, social security number, and residence at the time of death. It also requires details about the personal representative and any attorneys involved in the estate. The F 706 is divided into three parts, catering to Florida residents, nonresidents, and nonresident aliens, each addressing specific tax credits and calculations based on the estate's value. Additionally, the form outlines the due dates for submission and payment, which is typically within nine months following the decedent's death. Failure to comply with these requirements can result in penalties and interest on unpaid taxes. To ensure accurate processing, the personal representative must also attach a signed copy of the federal estate tax return, either Form 706 or 706-NA. Understanding the intricacies of the F 706 form is essential for fulfilling legal obligations and managing the estate effectively.

| Fact Name | Description |

|---|---|

| Form Title | The official name of the form is the Florida Estate Tax Return, designated as F-706. |

| Governing Laws | This form is governed by Chapter 198 of the Florida Statutes. |

| Filing Requirement | Form F-706 must be filed for estates subject to federal estate tax filing requirements. |

| Filing Deadline | The form and payment are due within 9 months after the decedent’s death. |

| Amended Returns | If changes are necessary, an amended return can be filed by checking the appropriate box. |

| Penalties for Late Payment | A late payment penalty starts at 10% of the unpaid tax if not paid by the due date. |

| Interest on Late Payments | Interest accrues on any unpaid tax from the original due date until it is paid in full. |

| Non-Residents and Aliens | Special provisions exist for non-residents and non-resident aliens filing this form. |

| Where to File | The completed form should be mailed to the Florida Department of Revenue in Tallahassee. |

Filling out the Florida F 706 form is a crucial step in managing estate tax obligations. This process requires careful attention to detail to ensure compliance with state regulations. Once the form is completed, it should be submitted to the Florida Department of Revenue, along with any necessary documentation.

What is the Florida F-706 form?

The Florida F-706 form is the Florida Estate Tax Return. It is required for estates that are subject to federal estate tax filing requirements. This form is used to report the estate tax due to the Florida Department of Revenue, and it is applicable to residents, nonresidents, and nonresident aliens who have property in Florida. The form must be filed within nine months after the decedent's death if a federal estate tax return is required.

Who needs to file the F-706 form?

Filing the F-706 form is necessary for the estates of individuals who died on or before December 31, 2004. For those who passed away on or after January 1, 2005, the form is generally not required unless the estate is subject to federal estate tax. This includes Florida residents, nonresidents, and nonresident aliens with Florida property that necessitates filing a federal estate tax return.

What are the penalties for not filing the F-706 form on time?

If the F-706 form is not filed by the due date, which is nine months after the decedent's death, penalties may apply. A late payment penalty of 10% of the unpaid tax will be assessed initially. If the payment remains overdue for more than 30 days, this penalty increases to 20%. Additional penalties can be imposed for negligence or intentional disregard of tax laws, with a maximum penalty of 50% for unpaid tax due to negligence. Furthermore, interest accrues on any unpaid tax from the due date until it is paid.

How do I amend a previously filed F-706 form?

To amend a previously filed F-706 form, you must complete a new F-706 form and check the box indicating that it is an amended return. If the amendment is due to changes in the federal Form 706 or 706-NA, you should attach a statement explaining the reasons for the amendment, along with any relevant documents, such as correspondence from the IRS or the amended federal forms.

Where should I mail the completed F-706 form?

The completed F-706 form, along with any payment, should be mailed to the Florida Department of Revenue at the following address:

If you are requesting a nontaxable certificate, do not forget to include the $5.00 fee along with your submission.

What should I do if I have questions about the F-706 form?

If you have questions regarding the F-706 form or the estate tax process, you can visit the Florida Department of Revenue's website at floridarevenue.com for more information and resources. Additionally, you can contact Taxpayer Services at 850-488-6800 during regular business hours. For written inquiries, you may send your questions to:

Filling out the Florida F 706 form can be a daunting task, and many people make common mistakes that can lead to delays or complications. One frequent error is failing to include the decedent's complete name. It’s essential to write the full name, including the first name, middle initial, and last name. Omitting any part of the name can create confusion and may result in processing issues.

Another mistake is neglecting to provide the decedent’s social security number. This number is crucial for identification purposes and must be accurately recorded. Skipping this step can lead to unnecessary delays in processing the return.

Additionally, many individuals forget to check the appropriate box if they are submitting an amended return. If changes have been made to the original filing, indicating that it’s an amendment is vital. Failing to do so can lead to complications in the review process.

People often overlook the requirement to submit proof of any estate, inheritance, or other death taxes paid to other states. This documentation must accompany the return. Without it, the Florida Department of Revenue may reject the claim for a credit, resulting in a higher tax liability.

Another common error is incorrectly calculating the estate tax due or overpayment. This calculation is critical and involves several lines of the form. Miscalculating can lead to either underpayment or overpayment, both of which can have financial repercussions.

Many filers also fail to sign the form. The personal representative must sign the return declaration under penalties of perjury. If someone else prepares the return, that individual must also sign. A missing signature can halt the processing of the return.

People sometimes forget to attach a copy of the federal estate tax return (Form 706 or 706-NA). This attachment is not just a formality; it’s a requirement that supports the information provided on the Florida F 706 form. Without it, the return may be considered incomplete.

Another mistake is not paying attention to the due dates. The F 706 form and payment are due within nine months after the decedent’s death. If you miss this deadline, penalties and interest can accrue, complicating the situation further.

Finally, failing to check for any updates or changes in the form’s instructions can lead to errors. Tax laws can change, and staying informed is crucial for ensuring compliance and accuracy. By avoiding these common pitfalls, you can help ensure a smoother process when filing the Florida F 706 form.

When dealing with the Florida F 706 form, there are several other forms and documents that may be necessary to ensure a smooth process. Each of these documents serves a specific purpose and plays a vital role in estate tax proceedings. Here’s a brief overview of some commonly used forms alongside the Florida F 706.

Understanding these forms and their purposes can greatly simplify the estate tax filing process in Florida. Being prepared with the necessary documentation not only helps in compliance but also ensures that the estate is settled efficiently and correctly.

The Florida F 706 form, which is the Florida Estate Tax Return, shares similarities with several other documents related to estate and tax matters. Below are six documents that are comparable to the Florida F 706, along with explanations of their similarities:

When filling out the Florida F-706 form, it's essential to approach the task with care. Here are some key do's and don'ts to keep in mind:

Following these guidelines can help ensure a smoother filing process and reduce the risk of errors or penalties.

This form is required for residents, nonresidents, and nonresident aliens with Florida property, as long as they meet federal estate tax filing requirements.

The F 706 form must be filed if a federal estate tax return is required, regardless of whether any Florida estate tax is due.

Filing is mandatory for estates that fall under specific criteria, particularly if they are required to file a federal estate tax return.

There are penalties for late payment and filing, which can increase significantly over time. It’s important to file on time to avoid these penalties.

A signed copy of the federal estate tax return (Form 706 or 706-NA) must be attached when filing the F 706 form.

The form must be filed within nine months of the decedent’s death, aligning with the due date for the federal estate tax return.

Florida estate tax is only imposed on estates that are required to file a federal estate tax return and are entitled to a credit for state death taxes.

When dealing with the Florida F-706 form, there are several important points to keep in mind. Understanding these can help ensure that the process goes smoothly and that all necessary requirements are met.