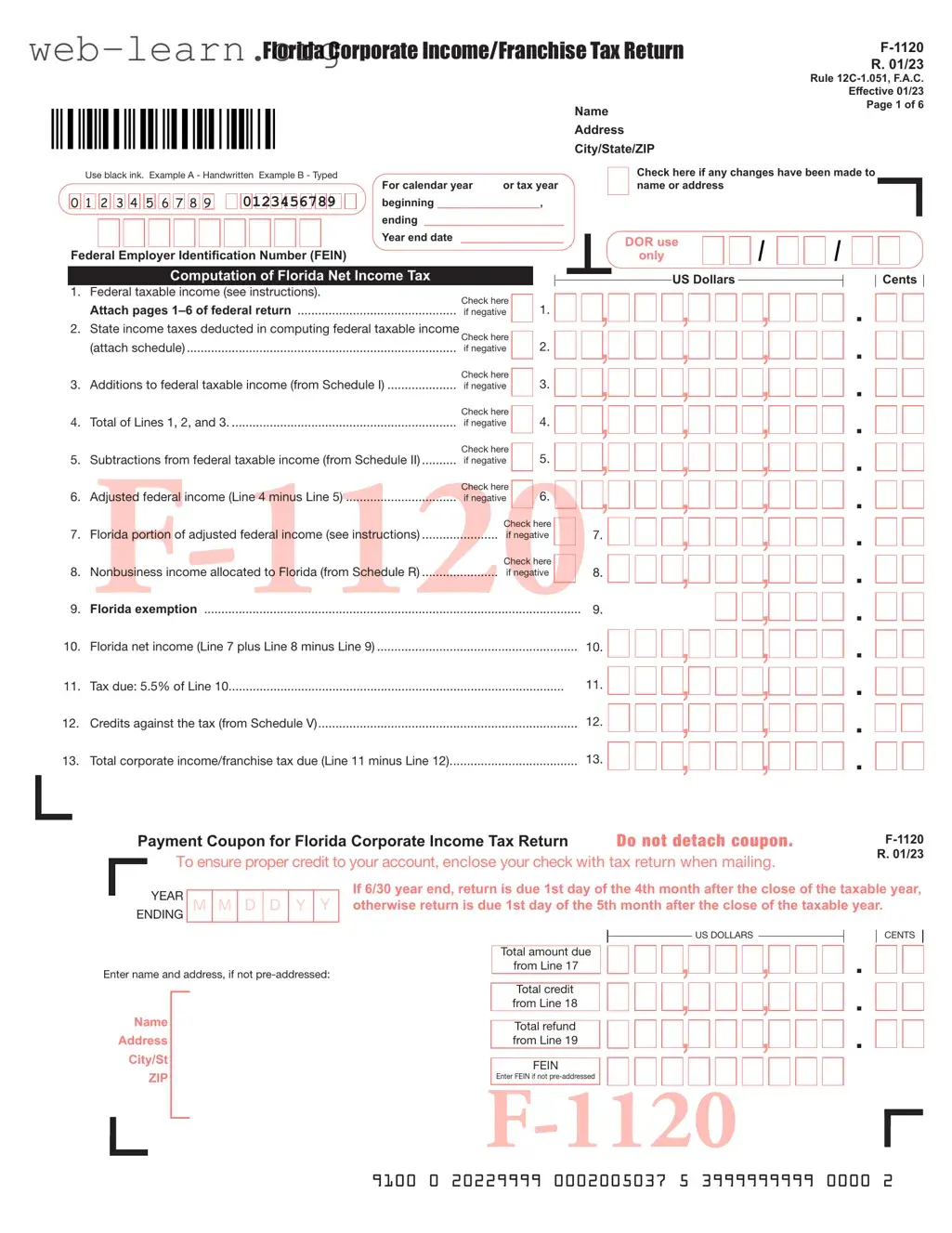

The Florida F 1120 form is essential for corporations operating in the state, as it serves as the Corporate Income/Franchise Tax Return. This form is used to report a corporation's income, deductions, and tax liabilities to the Florida Department of Revenue. When filling out the F 1120, businesses must detail their federal taxable income, make necessary adjustments, and calculate their Florida net income. The form includes various sections for additions and subtractions to federal taxable income, allowing corporations to account for specific credits and deductions. Additionally, it requires information about the corporation’s business activities, including its location, federal employer identification number, and any changes in name or address. Companies are also prompted to attach relevant schedules and their federal return to ensure completeness. Understanding and accurately completing the F 1120 is crucial for compliance and can help businesses manage their tax obligations effectively.

| Fact Name | Details |

|---|---|

| Form Purpose | The Florida F 1120 form is used for filing the Corporate Income/Franchise Tax Return for corporations operating in Florida. |

| Governing Laws | This form is governed by Rule 12C-1.051, Florida Administrative Code (F.A.C.), effective January 2020. |

| Filing Requirements | Corporations must attach a copy of their federal return to the F 1120 form. Incomplete returns may be subject to penalties. |

| Tax Rate | The tax rate for Florida Corporate Income Tax is 4.458% of the Florida net income as reported on Line 10 of the form. |

Completing the Florida F-1120 form requires careful attention to detail and accurate reporting of your corporate income and taxes. Once the form is filled out, it must be submitted to the Florida Department of Revenue along with any required attachments. Ensure all necessary information is accurate to avoid penalties.

What is the Florida F 1120 form?

The Florida F 1120 form is the Corporate Income/Franchise Tax Return used by corporations operating in Florida. This form is essential for reporting a corporation's income, calculating the tax owed, and ensuring compliance with state tax laws.

Who needs to file the F 1120 form?

Any corporation that conducts business in Florida must file the F 1120 form. This includes both domestic and foreign corporations that have income sourced from Florida. If your corporation is classified as a C corporation for federal tax purposes, you will typically need to complete this form.

When is the F 1120 form due?

The F 1120 form is generally due on the first day of the fourth month following the end of your corporation's fiscal year. For corporations operating on a calendar year, the due date is April 1. If you need additional time, you can file for an extension using Form F-7004.

What information is required to complete the F 1120 form?

To complete the F 1120 form, you will need to provide:

What happens if I don’t file the F 1120 form?

Failing to file the F 1120 form can lead to penalties, including fines and interest on any unpaid taxes. Additionally, your corporation may face legal consequences, such as loss of good standing with the state. It’s important to file on time to avoid these issues.

Can I e-file the F 1120 form?

Yes, the Florida Department of Revenue allows electronic filing for the F 1120 form. E-filing can streamline the process and reduce the chances of errors. Ensure that you have all required information ready before starting the e-filing process.

What are the tax rates for the Florida corporate income tax?

The corporate income tax rate in Florida is currently set at 4.458% of the Florida net income. This rate applies to the taxable income after all deductions and credits have been taken into account.

Are there any tax credits available for corporations filing the F 1120 form?

Yes, various tax credits may be available to corporations. These include credits for enterprise zone jobs, capital investment, and renewable energy production, among others. It's important to review the specific eligibility requirements for each credit to maximize potential savings.

What should I do if I made a mistake on my F 1120 form?

If you discover an error after submitting your F 1120 form, you should file an amended return as soon as possible. Use the appropriate form for amendments and provide a clear explanation of the changes made. This can help avoid penalties and interest on any underreported income.

Where do I send my completed F 1120 form?

Send your completed F 1120 form to the Florida Department of Revenue at the following address:

Florida Department of Revenue

5050 W Tennessee Street

Tallahassee, FL 32399-0135

If you are requesting a refund, send your return to:

Florida Department of Revenue

PO Box 6440

Tallahassee, FL 32314-6440

Completing the Florida F-1120 form can be a daunting task, and many individuals and businesses make mistakes that can lead to delays or penalties. One common error is failing to attach the required federal return. The instructions clearly state that the Florida F-1120 return is considered incomplete without a copy of the federal return. This oversight can result in the return being rejected or delayed, which can complicate tax obligations.

Another frequent mistake involves incorrect calculations of federal taxable income. Taxpayers often miscalculate their income or fail to account for additions and subtractions that impact their taxable income. It is crucial to double-check the numbers on Lines 1 through 10, as inaccuracies can lead to incorrect tax assessments. Ensuring that all required schedules are completed accurately is essential to avoid issues with the Florida Department of Revenue.

Many filers also overlook the importance of signing the return. A return that is not signed or is improperly signed can incur penalties. The declaration section emphasizes that the return must be signed by an authorized officer of the corporation. This step is not merely a formality; it is a legal requirement that validates the information provided.

Another mistake often made is neglecting to answer all questions in the taxpayer information section. Questions A through L must be answered fully to provide the Florida Department of Revenue with necessary information about the corporation. Incomplete responses can lead to additional inquiries or delays in processing the return.

Finally, failing to keep a copy of the submitted return and all accompanying documentation can create problems down the line. Taxpayers should retain copies for their records, as this can be invaluable in case of audits or discrepancies. Maintaining thorough documentation not only helps in managing tax responsibilities but also supports compliance with state regulations.

The Florida F-1120 form is essential for corporations filing their corporate income or franchise tax returns in Florida. Alongside this form, several other documents are commonly required to ensure accurate reporting and compliance with state tax regulations. Here’s a list of these documents and their purposes.

By preparing these documents carefully, corporations can navigate the complexities of Florida's tax requirements more effectively. Ensuring all necessary forms are included with the F-1120 can prevent delays and penalties, allowing for a smoother filing process.

When filling out the Florida F-1120 form, there are several important considerations to keep in mind. The following list outlines key actions to take and avoid during the process.

Here are six common misconceptions about the Florida F 1120 form:

Filling out the Florida F-1120 form requires careful attention to detail. Here are five key takeaways to help ensure a smooth process:

By following these guidelines, you can navigate the F-1120 form with greater confidence and accuracy.