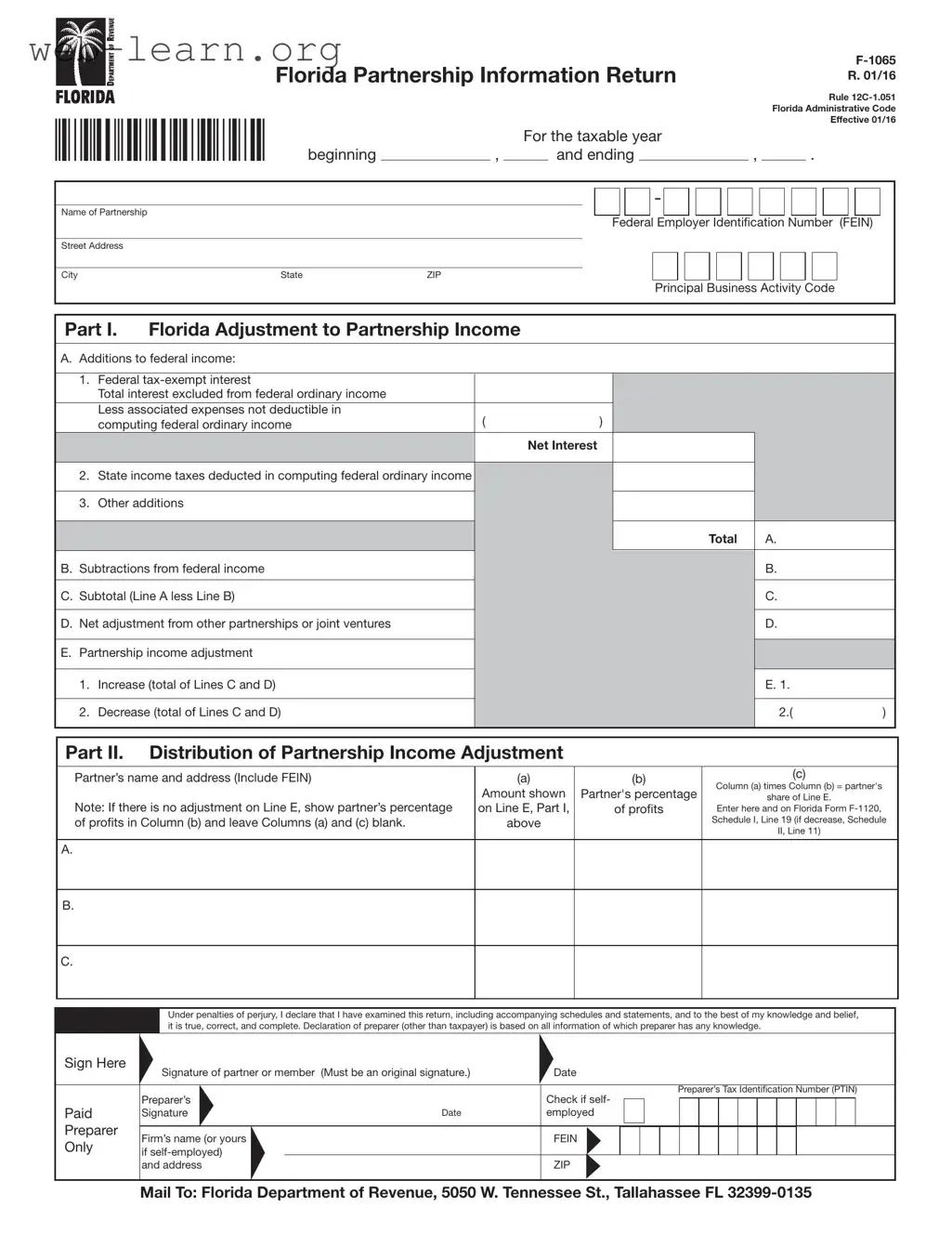

The Florida F 1065 form, officially known as the Florida Partnership Information Return, is a crucial document for partnerships operating within the state. This form must be filed by any Florida partnership that has partners subject to the Florida Corporate Income Tax Code. It captures essential information about the partnership's income, deductions, and apportionment factors. In its structure, the form includes sections that address adjustments to federal income, distributions of partnership income adjustments, and apportionment information for partners. Each partnership must detail additions and subtractions from federal income, which are necessary for calculating the adjusted income that will be passed through to partners. Additionally, the form requires partnerships to report their business activities both within and outside Florida, using a three-factor formula to determine how income is apportioned. The F 1065 form is not just a tax document; it plays a vital role in ensuring that partnerships comply with state tax laws while accurately reflecting their financial activities. Completing this form correctly is essential for partnerships to avoid penalties and ensure that their tax obligations are met efficiently.

| Fact Name | Description |

|---|---|

| Form Purpose | The Florida F-1065 form is used for reporting partnership income and adjustments for tax purposes. |

| Governing Law | This form is governed by Rule 12C-1.051 of the Florida Administrative Code. |

| Filing Requirement | Every Florida partnership with a partner subject to Florida Corporate Income Tax must file this form. |

| Filing Deadline | The form must be filed on or before the first day of the fifth month after the close of the taxable year. |

| Extension Application | To extend the filing deadline, Florida Form F-7004 must be submitted. |

| Signature Requirement | An original signature is required from an authorized officer or partner on the form. |

| Income Adjustments | Part I of the form is used to report additions and subtractions from federal income. |

| Apportionment Information | Part III provides details on how to apportion income for partnerships doing business both within and outside Florida. |

| Average Value of Property | The average value of property in Florida is calculated based on the property's original cost. |

| Sales Definition | Sales include gross receipts, rental income, and service income, among others, without regard to returns or allowances. |

Completing the Florida F-1065 form requires careful attention to detail. This form is essential for partnerships operating in Florida, as it helps report the partnership's income and adjustments. Follow these steps to ensure you fill it out correctly and submit it on time.

After submitting the form, keep a copy for your records. Be mindful of deadlines to avoid penalties. If you need more time, consider applying for an extension using Florida Form F-7004. Always double-check your entries for accuracy before mailing the form.

What is the Florida F-1065 form?

The Florida F-1065 form is the Partnership Information Return that partnerships operating in Florida must file. This form reports the partnership's income, deductions, and adjustments for state tax purposes. It is essential for partnerships that have partners subject to Florida's Corporate Income Tax Code.

Who is required to file the F-1065 form?

Every Florida partnership with any partner subject to the Florida Corporate Income Tax must file this form. Additionally, limited liability companies classified as partnerships for federal tax purposes must also file. If a foreign corporation is a partner in a Florida partnership, it is subject to the Florida Income Tax Code and must file a Florida Corporate Income/Franchise Tax Return.

When is the F-1065 form due?

The F-1065 form is due on or before the first day of the fifth month following the close of the partnership's taxable year. If the due date falls on a weekend or holiday, the form is considered timely if postmarked on the next business day.

How can a partnership request an extension for filing the F-1065?

To request an extension, partnerships must complete Florida Form F-7004, which is the application for an extension of time to file. It is important to note that a federal extension does not automatically extend the time for filing the Florida return. Extensions are valid for five months, and only one extension is allowed.

What information is needed to complete the F-1065 form?

Partnerships will need their Federal Employer Identification Number (FEIN), Principal Business Activity Code, and details regarding income, deductions, and adjustments. Additionally, they must provide information about property, payroll, and sales if doing business outside Florida.

What are the key parts of the F-1065 form?

The F-1065 form consists of several parts:

Each part serves a specific purpose in reporting the partnership's income and how it is allocated among partners.

How does a partnership determine its income adjustments?

Part I of the F-1065 form requires partnerships to make adjustments to their federal income. This includes adding or subtracting specific items, such as federal tax-exempt interest or state income taxes. The final adjustment is calculated by combining these additions and subtractions to arrive at the partnership's adjusted income.

What is the significance of apportionment information on the F-1065?

Apportionment information is crucial for partnerships doing business both in and out of Florida. It determines how much of the partnership's income is subject to Florida tax based on property, payroll, and sales ratios. This ensures that only the income attributable to Florida is taxed.

What should partnerships do if they cease operations?

If a partnership ceases to exist, it must indicate this by writing "FINAL RETURN" at the top of the F-1065 form. This signals to the Florida Department of Revenue that it is the last return for the partnership.

Where should partnerships mail the completed F-1065 form?

Partnerships must mail the completed F-1065 form to the Florida Department of Revenue at the following address: 5050 W. Tennessee St., Tallahassee, FL 32399-0135. Ensuring that it is sent to the correct address is vital for timely processing.

Filling out the Florida F 1065 form can be a complex process, and several common mistakes can lead to complications. One frequent error occurs when individuals fail to enter the Federal Employer Identification Number (FEIN). This number is crucial for identifying the partnership and must be included accurately. Omitting it or entering an incorrect number can delay processing and create issues with the Florida Department of Revenue.

Another common mistake involves the Principal Business Activity Code. Many filers either leave this section blank or enter an incorrect code. This code is essential for classifying the partnership’s activities and ensuring compliance with state regulations. An accurate code helps the state assess the appropriate tax obligations.

Inaccurate calculations in Part I of the form can also lead to significant problems. Filers often miscalculate the additions and subtractions from federal income. Each line must be carefully reviewed to ensure that all relevant amounts are included or excluded correctly. Mistakes in these calculations can result in overpayment or underpayment of taxes, leading to potential penalties.

Moreover, failing to provide complete information about each partner in Part II can create complications. Each partner's name, address, and percentage share must be reported accurately. Incomplete or incorrect information may hinder the distribution of income adjustments and affect the partners' tax returns.

Another mistake that occurs frequently is the failure to sign the form. An original signature from a partner or authorized member is required for the return to be valid. Submitting the form without a signature can lead to rejection or delays in processing.

Additionally, not adhering to the filing deadlines is a common oversight. The Florida F 1065 form must be filed by the first day of the fifth month following the close of the taxable year. Missing this deadline can result in penalties and interest on any taxes owed.

Lastly, many partnerships neglect to attach necessary schedules or statements. If the lines on the F 1065 form are insufficient, attachments must be included to provide all required information. Failing to do so can lead to incomplete submissions, requiring further clarification and potentially delaying processing.

The Florida F-1065 form is a crucial document for partnerships operating within the state, as it provides necessary information for tax purposes. In addition to this form, there are several other documents that partnerships may need to complete or reference. Below is a list of commonly used forms and documents that often accompany the Florida F-1065.

Understanding these documents can help partnerships ensure compliance with state and federal regulations. Each form serves a specific purpose and contributes to the overall tax reporting process for partnerships operating in Florida.

When filling out the Florida F 1065 form, there are several important practices to keep in mind. Below is a list of what to do and what to avoid.

This is not true. Any partnership with a partner subject to Florida Corporate Income Tax must file the F 1065 form, even if it operates outside Florida.

While the F 1065 form shares similarities with the federal return, it includes specific adjustments and requirements unique to Florida tax laws. It is essential to follow Florida's guidelines when completing this form.

Filing the F 1065 form is mandatory for partnerships that have any partners subject to the Florida Corporate Income Tax Code. Failure to file can result in penalties.

This is incorrect. To extend the filing deadline for the F 1065, you must complete Florida Form F-7004 specifically. A federal extension does not apply to Florida returns.

Partnerships must report income adjustments from other partnerships or joint ventures. This is crucial for determining the accurate partnership income adjustment on the F 1065 form.

Each return must include an original signature from a partner or authorized member. Photocopies or facsimiles are not acceptable.

If the lines on the F 1065 form are insufficient, partnerships can attach additional schedules. These must follow the required format and contain all necessary information.

Who Must File: Every Florida partnership with any partner subject to the Florida Corporate Income Tax Code must complete the F-1065 form.

Filing Deadline: Submit the F-1065 form by the first day of the fifth month following the end of your taxable year.

Extensions: To extend your filing time, complete Florida Form F-7004. A federal extension does not apply to Florida returns.

Original Signatures Required: Ensure that the form is signed by an authorized person. Photocopies or stamps are not accepted.

Adjustments to Income: Use Part I to report any additions or subtractions to federal income, which will affect the partnership income adjustment.

Apportionment Information: Complete Parts III and IV if your partnership operates both within and outside Florida to determine how to apportion income.

Attachments: If necessary, attach additional statements or schedules that contain all required information. Do not attach your federal return.