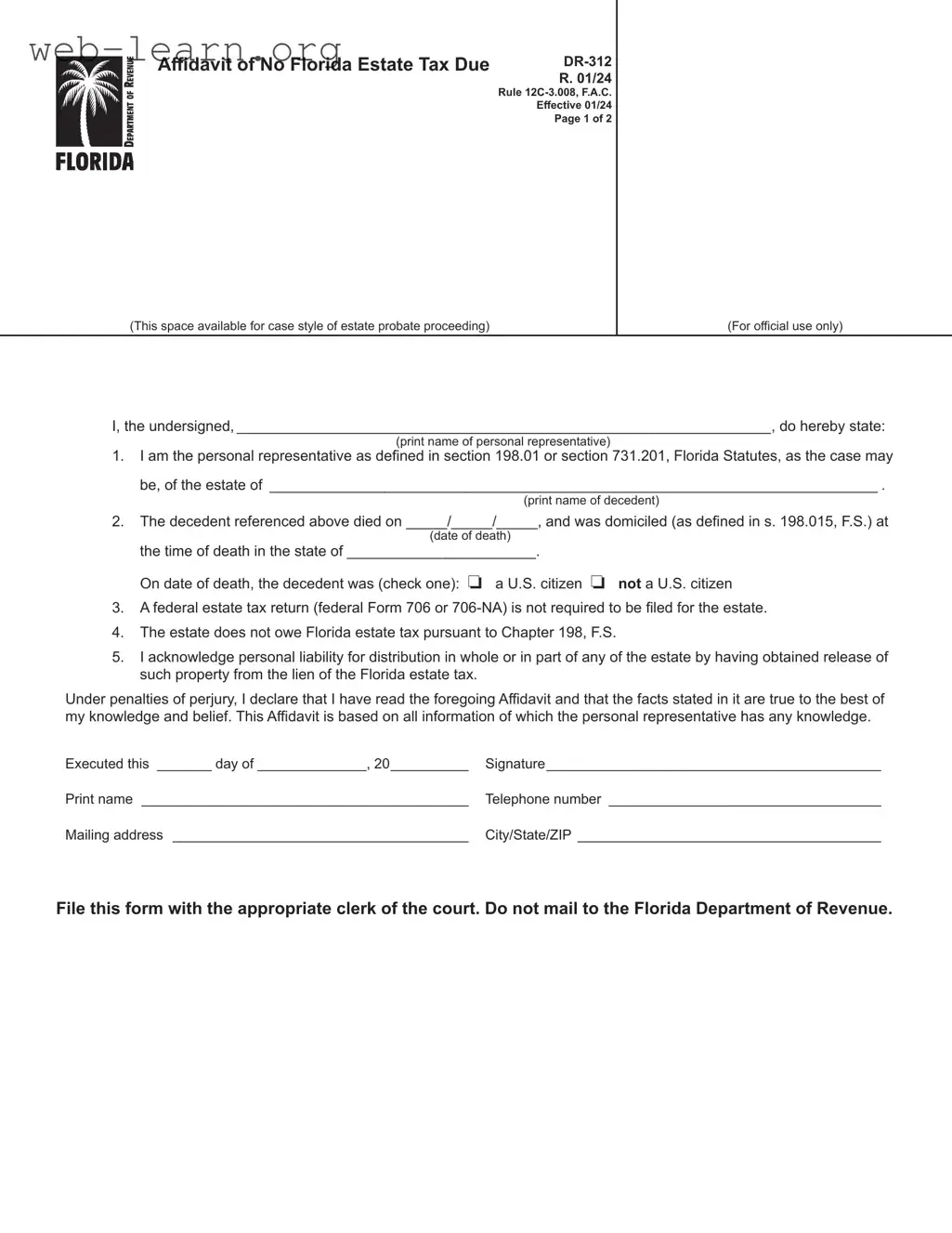

The FL DR 312 form, officially known as the Affidavit of No Florida Estate Tax Due, serves a crucial role in the estate administration process in Florida. Designed for personal representatives of estates, this form is necessary when there is no Florida estate tax owed and no requirement to file a federal estate tax return, specifically Form 706 or 706-NA. By completing this affidavit, the personal representative affirms that the decedent, who passed away while domiciled in Florida, does not have any outstanding estate tax obligations. The form requires essential details such as the decedent's name, date of death, and the representative's acknowledgment of personal liability for the distribution of estate property. Additionally, the FL DR 312 is admissible as evidence of nonliability for Florida estate tax, effectively removing any tax lien imposed by the Florida Department of Revenue. It is important to file this form with the appropriate clerk of the circuit court in the county where the decedent owned property, rather than sending it to the Florida Department of Revenue. Understanding the proper use and filing of the FL DR 312 can streamline the estate settlement process, ensuring compliance with state regulations while alleviating potential tax burdens.

| Fact Name | Details |

|---|---|

| Form Title | Affidavit of No Florida Estate Tax Due DR-312 |

| Governing Law | Chapter 198, Florida Statutes |

| Effective Date | January 2021 |

| Purpose | This form certifies that no Florida estate tax is due for the estate of the decedent. |

| Filing Requirement | File with the clerk of the circuit court in the county where the decedent owned property. |

| Federal Return Status | A federal estate tax return (Form 706 or 706-NA) is not required for the estate. |

| Personal Representative | The individual filing must be the personal representative as defined in Florida law. |

| Liability Acknowledgment | The personal representative acknowledges liability for distributions made from the estate. |

| Admissibility | This affidavit is admissible as evidence of nonliability for Florida estate tax. |

| Contact Information | For questions, contact Taxpayer Services at 850-488-6800. |

After completing the Fl Dr 312 form, you will need to file it with the appropriate clerk of the court in the county where the decedent owned property. This form serves as an affidavit confirming that no Florida estate tax is due. Make sure to follow the steps carefully to ensure that all required information is provided.

Once you have completed the form, submit it directly to the clerk of the circuit court. Do not mail it to the Florida Department of Revenue.

The FL DR 312 form, officially known as the Affidavit of No Florida Estate Tax Due, is used by personal representatives of estates to declare that no Florida estate tax is owed. This form is particularly relevant when a federal estate tax return is not required, indicating that the estate does not meet the threshold for tax liability under Florida law.

Eligibility to file the FL DR 312 form is granted to personal representatives as defined in Florida Statutes. This includes individuals who are in actual or constructive possession of the decedent’s property. Additionally, anyone who has been appointed to manage the estate can complete and submit this affidavit.

The form should be utilized when an estate is not subject to Florida estate tax under Chapter 198 of the Florida Statutes. It is also applicable when there is no requirement to file a federal estate tax return, specifically Forms 706 or 706-NA. If the estate meets the criteria for federal filing, this form cannot be used.

The FL DR 312 form must be filed with the clerk of the circuit court in the county or counties where the decedent owned property. It is important to note that this form should not be mailed to the Florida Department of Revenue.

Filing the FL DR 312 form serves as evidence of nonliability for Florida estate tax. It effectively removes the Department of Revenue’s estate tax lien from the estate’s property. Once filed, the Florida Department of Revenue will no longer issue Nontaxable Certificates for estates that have submitted this affidavit.

To complete the FL DR 312 form, the personal representative must provide specific details including their name, the name of the decedent, the date of death, the decedent’s domicile at the time of death, and whether the decedent was a U.S. citizen. Additionally, the representative must affirm that a federal estate tax return is not required and acknowledge personal liability for any distributions made.

Filling out the FL DR-312 form can be a straightforward process, but many individuals make common mistakes that can lead to delays or complications. Understanding these pitfalls can help ensure that the form is completed accurately and efficiently.

One frequent error is failing to provide the correct name of the decedent. It is crucial to ensure that the name printed matches the official documentation. Any discrepancies can result in the form being rejected or delayed. Additionally, omitting the date of death or providing an incorrect date can also cause significant issues. This date is essential for establishing the timeline of the estate and determining tax obligations.

Another mistake is neglecting to check the box indicating whether the decedent was a U.S. citizen. This detail is important as it can affect the estate's tax status. Furthermore, some individuals mistakenly believe that they can file the form with the Florida Department of Revenue. In reality, the FL DR-312 must be filed directly with the clerk of the court in the appropriate county.

Many people also overlook the requirement to acknowledge personal liability for the distribution of the estate. This acknowledgment is a critical component of the affidavit and must be understood fully before signing. Failing to read the affidavit carefully can lead to unintentional errors, such as signing without understanding the implications of personal liability.

Another common oversight involves not including complete contact information. The form requires a telephone number and mailing address, which are necessary for any follow-up communications. Incomplete information can hinder the processing of the form and lead to unnecessary delays.

Some individuals also forget to include the case style of the estate probate proceeding in the designated space. This detail is important for the court's records and should not be overlooked. Lastly, it's essential to remember that the form should not be altered in any way, especially in the designated area for the clerk of the court. Any markings in this area can lead to complications in processing the form.

By being aware of these common mistakes, individuals can navigate the completion of the FL DR-312 form more effectively. Attention to detail and careful review can save time and ensure that the estate is handled smoothly.

The FL DR 312 form, or Affidavit of No Florida Estate Tax Due, is essential for personal representatives of estates that are not subject to Florida estate tax. When utilizing this form, several other documents may be required or beneficial in the estate administration process. Below is a list of forms and documents that are commonly used alongside the FL DR 312.

These documents play a vital role in the estate administration process. Each serves a specific purpose, ensuring that the estate is managed according to legal requirements and the decedent's wishes. Personal representatives should ensure they have all necessary documentation to facilitate a smooth probate process.

The Florida Form DR-312, known as the Affidavit of No Florida Estate Tax Due, is similar to several other documents used in estate management and tax matters. Here are nine documents that share similarities with Form DR-312:

Each of these documents serves a specific purpose in the estate management process, similar to how Form DR-312 addresses the issue of Florida estate tax liability.

When filling out the FL DR 312 form, attention to detail is crucial. Here are six important dos and don'ts to keep in mind:

Following these guidelines will help ensure a smooth process when completing the FL DR 312 form.

Here are ten misconceptions about the Florida Form DR-312, Affidavit of No Florida Estate Tax Due, along with clarifications for each:

This form can be used for any estate that is not subject to Florida estate tax, regardless of size, as long as a federal estate tax return is not required.

In fact, this form should be filed directly with the clerk of the circuit court in the county where the decedent owned property.

The DR-312 only addresses Florida estate tax. Other taxes, such as income or inheritance taxes, may still apply.

It should be filed promptly after determining that no Florida estate tax is due and that no federal return is required.

This form cannot be used if a federal Form 706 or 706-NA is required to be filed.

Any person in actual or constructive possession of property in the decedent’s estate can complete this affidavit.

The DR-312 is a legal document that, when executed, serves as evidence of nonliability for Florida estate tax and can remove the tax lien.

While legal advice can be helpful, it is not necessary to have a lawyer complete and file this form.

This form is specific to Florida and should only be used for estates within the state.

A signature from the personal representative is mandatory, as it affirms the truthfulness of the information provided.

Form DR-312 is used to declare that no Florida estate tax is due for a decedent's estate.

This affidavit must be filed with the clerk of the circuit court in the county where the decedent owned property.

It is essential to ensure that a federal estate tax return (Form 706 or 706-NA) is not required before using this form.

Completing this form can help remove the Florida estate tax lien from the estate.

The personal representative must sign the form and provide their contact information.

Do not send Form DR-312 to the Florida Department of Revenue; it is only for the court clerk.