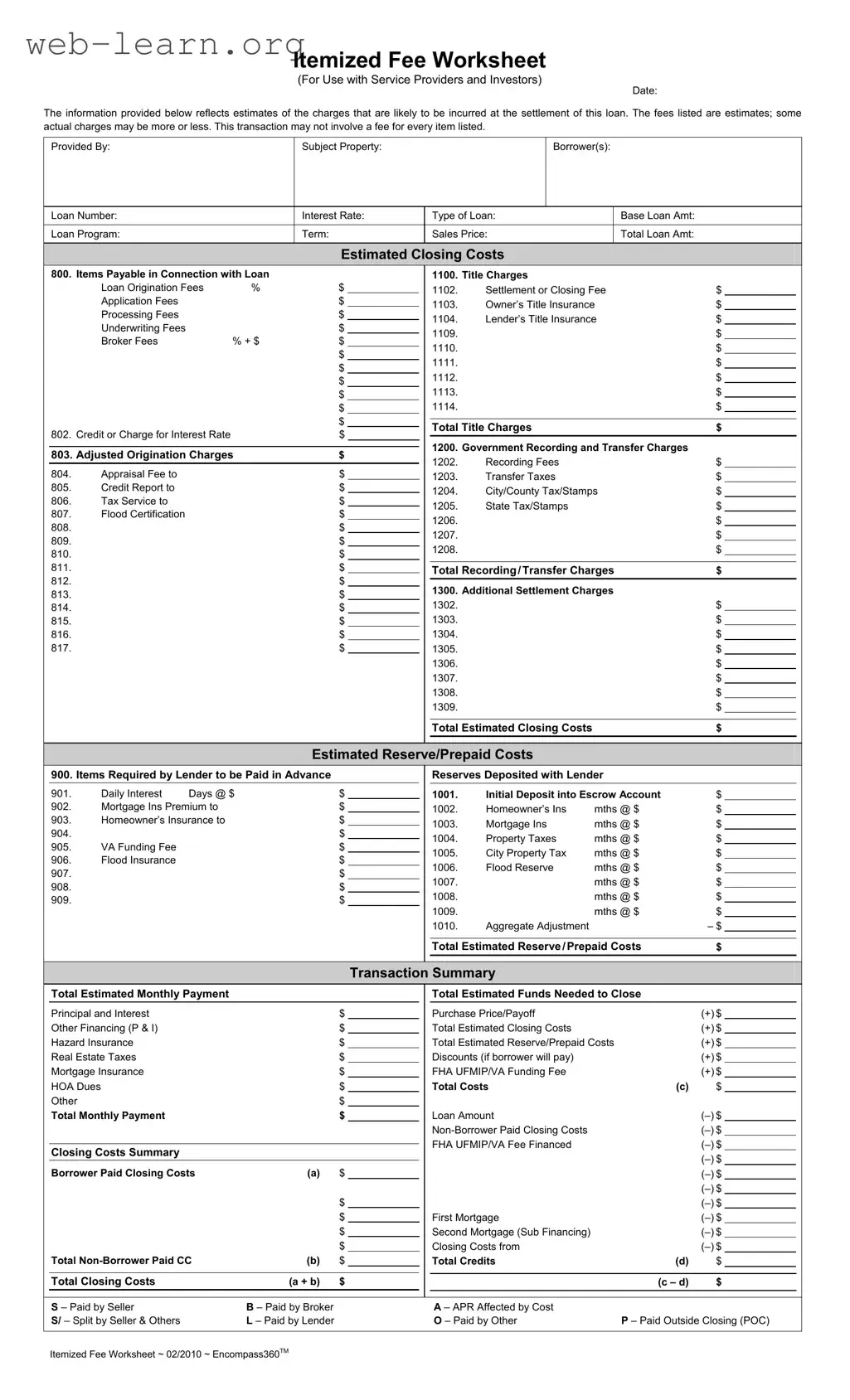

The Fee Worksheet form serves as a crucial tool for individuals navigating the complexities of loan settlements. It provides a detailed breakdown of estimated charges that borrowers can expect to incur during the closing process. This worksheet not only lists various fees associated with the loan but also categorizes them into specific sections such as title charges, recording and transfer charges, and additional settlement charges. Each item is designed to give clarity on costs like loan origination fees, appraisal fees, and title insurance, among others. Additionally, the form accounts for estimated reserves and prepaid costs, ensuring that borrowers understand their financial obligations before finalizing a loan. By offering a comprehensive overview, the Fee Worksheet empowers borrowers to make informed decisions and prepares them for the financial aspects of their real estate transactions.

| Fact Name | Description |

|---|---|

| Purpose | The Fee Worksheet is designed to provide an itemized estimate of charges that may be incurred during the settlement of a loan. |

| Estimates | The fees listed are estimates. Actual charges may vary, and not all items may incur a fee. |

| Applicable Laws | This form is governed by the Real Estate Settlement Procedures Act (RESPA) and varies by state regulations. |

| Components | The worksheet includes sections for loan charges, recording fees, and estimated closing costs among other details. |

Filling out the Fee Worksheet form is an essential step in the loan process. This form helps you estimate the various costs associated with your loan, ensuring you have a clear understanding of what to expect at closing. Follow these steps to complete the form accurately.

Once you have completed the Fee Worksheet, review all entries for accuracy. This will help ensure that you have a comprehensive understanding of your financial obligations as you move forward in the loan process.

What is the purpose of the Fee Worksheet form?

The Fee Worksheet form serves as a detailed estimate of the charges associated with a loan settlement. It provides a breakdown of potential costs that borrowers may incur, helping them understand the financial obligations related to their loan.

Who should use the Fee Worksheet form?

This form is primarily intended for use by service providers and investors involved in real estate transactions. Borrowers can also benefit from reviewing this document to gain clarity on the estimated costs of their loan.

What types of fees are included in the Fee Worksheet?

The Fee Worksheet includes various categories of fees, such as:

Each category provides a detailed list of specific charges that may apply.

Are the fees listed in the Fee Worksheet final?

No, the fees presented in the Fee Worksheet are estimates. Actual charges may vary and could be higher or lower than those listed. It is important for borrowers to review their final closing statement for the exact amounts.

How can I determine my total estimated closing costs?

Total estimated closing costs can be calculated by summing all the fees listed under the “Estimated Closing Costs” section of the Fee Worksheet. This includes items payable in connection with the loan, title charges, and any additional settlement charges.

What are reserve/prepaid costs?

Reserve/prepaid costs are amounts that the lender requires to be paid in advance. These may include items such as mortgage insurance premiums, homeowner’s insurance, and property taxes. These costs are typically deposited into an escrow account to cover future payments.

Can I negotiate any of the fees listed in the Fee Worksheet?

Yes, many fees can be negotiated. It is advisable for borrowers to discuss potential adjustments with their lender or service provider. This may include loan origination fees, closing costs, or other charges that can vary by lender.

What should I do if I notice discrepancies in the Fee Worksheet?

If you find discrepancies in the Fee Worksheet, it is crucial to address them promptly. Contact your lender or service provider to clarify any inconsistencies. Open communication can help resolve issues before the closing process begins.

How does the Fee Worksheet affect my overall loan process?

The Fee Worksheet plays a significant role in your loan process by providing transparency regarding costs. Understanding these fees helps borrowers make informed decisions and prepares them for the financial responsibilities associated with their loan.

Filling out the Fee Worksheet form can be a daunting task, and many people make mistakes that can lead to confusion or delays in the loan process. One common mistake is failing to provide accurate information in the “Subject Property” section. This information is crucial for identifying the property involved in the transaction. If the details are incorrect, it can cause issues down the line, including problems with title searches or closing documents.

Another frequent error occurs in the section for “Estimated Closing Costs.” People often overlook the importance of itemizing each fee accurately. It is essential to list all applicable fees, including loan origination fees and title charges. Neglecting to include these can result in an underestimation of the total costs, which can surprise borrowers at closing.

Many individuals also make the mistake of not updating the “Interest Rate” and “Loan Amount” fields. These figures can change frequently, and using outdated numbers can lead to significant discrepancies in the final loan terms. Always double-check these amounts before submitting the form.

Another area where errors often occur is in the “Items Required by Lender to be Paid in Advance” section. Borrowers may forget to include necessary reserves or prepaid costs, such as homeowner's insurance or property taxes. These costs are critical for ensuring that the lender receives all required payments upfront.

In addition, people sometimes fail to account for “Non-Borrower Paid Closing Costs.” This section is important for accurately reflecting who is responsible for which costs. Not including these costs can lead to confusion and disputes later in the process.

Lastly, borrowers may misinterpret the “Transaction Summary” section. This part consolidates all costs, payments, and credits. If any part of this summary is filled out incorrectly, it can affect the overall understanding of the financial obligations involved in the loan.

By being aware of these common mistakes, individuals can take steps to fill out the Fee Worksheet form more accurately. Attention to detail is key. A thorough review can help ensure a smoother loan process and a more positive experience overall.

When preparing for a loan settlement, several documents complement the Fee Worksheet form. Each document serves a specific purpose and provides essential information that helps borrowers understand their financial obligations. Below are four common documents often used alongside the Fee Worksheet.

Understanding these documents can significantly ease the loan settlement process. Each plays a vital role in ensuring transparency and protecting the interests of all parties involved. Being informed helps borrowers make better decisions and prepares them for a successful closing experience.

The Fee Worksheet form is essential for understanding the costs associated with a loan settlement. Several other documents share similarities with this form, particularly in how they outline fees and charges. Here are five documents that are comparable:

When completing the Fee Worksheet form, attention to detail is essential. Here are five recommendations to ensure accuracy and compliance.

Understanding the Fee Worksheet form can be challenging, and misconceptions often arise. Here are ten common misunderstandings about this important document:

By addressing these misconceptions, borrowers and investors can approach their transactions with greater confidence and understanding. Awareness of the Fee Worksheet's purpose and limitations is essential for making informed financial decisions.

When using the Fee Worksheet form, it is essential to keep several key points in mind to ensure a smooth and accurate completion. Here are some important takeaways: