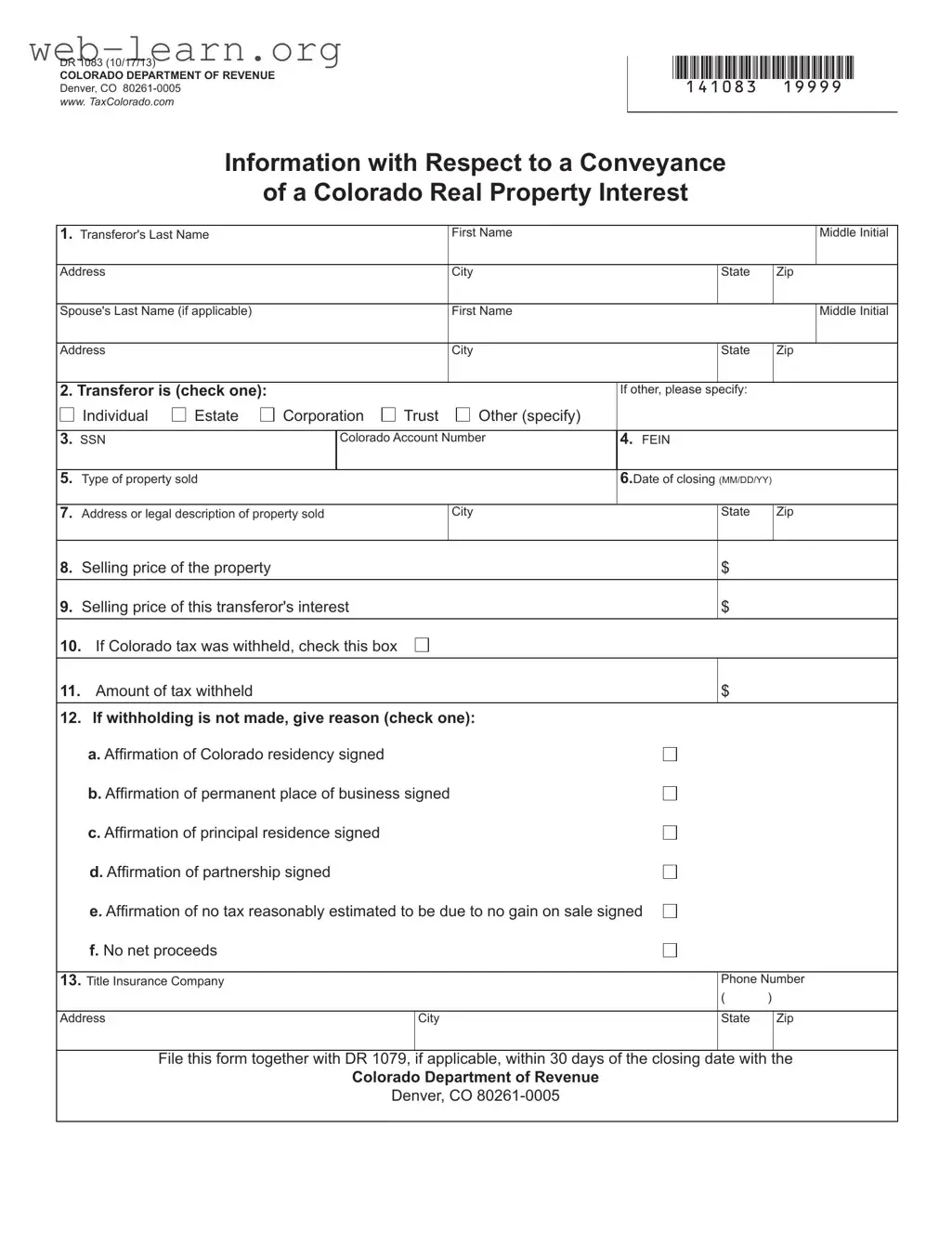

The DR 1083 form is a crucial document for anyone involved in the sale of real property in Colorado, especially for non-residents. It serves to report the transfer of a real property interest and addresses the withholding tax that may apply to the transaction. This form requires detailed information about the transferor, including names, addresses, and whether the transferor is an individual, corporation, estate, or trust. Key aspects include the selling price of the property and the transferor's interest, as well as any Colorado tax withheld during the sale. The form also features affirmations that the transferor can sign to assert residency or business status in Colorado, which can exempt them from withholding requirements. To ensure compliance, the completed DR 1083 must be filed with the Colorado Department of Revenue within 30 days of the closing date. Understanding the specifics of this form is essential for a smooth transaction and to avoid potential penalties for failure to comply with Colorado tax regulations.

| Fact Name | Description |

|---|---|

| Form Purpose | The DR 1083 form is used to report the conveyance of a real property interest in Colorado. |

| Governing Law | This form is governed by Colorado Revised Statutes, specifically §39-22-604.5. |

| Transferor Information | Transferors must provide their full names, addresses, and, if applicable, the names of their spouses. |

| Type of Transferor | The form allows for various types of transferors, including individuals, estates, corporations, and trusts. |

| Tax Withholding Requirement | Sales of Colorado real property valued at $100,000 or more by nonresidents are generally subject to tax withholding. |

| Exemptions from Withholding | There are several exemptions, including when the selling price is below $100,000 or when the transferor has a Colorado address. |

| Filing Deadline | The form must be filed within 30 days of the closing date of the transaction. |

| Signature Requirement | Transferors must sign the form under penalty of perjury, affirming the accuracy of the provided information. |

| Tax Amount Calculation | The amount withheld is the lesser of 2% of the selling price or the net proceeds due to the transferor. |

| Contact Information | For further assistance, individuals can visit the Colorado Department of Revenue website or call their service number. |

Completing the DR 1083 form is an important step when dealing with the sale of real property in Colorado. Once you have gathered the necessary information, follow these steps to ensure that the form is filled out correctly and submitted on time.

Once you have completed the form, ensure that it is submitted to the Colorado Department of Revenue within 30 days of the closing date, along with any other required forms. This step is crucial to avoid penalties and ensure compliance with state tax regulations.

What is the purpose of the DR 1083 form?

The DR 1083 form is used to report the conveyance of a real property interest in Colorado. It is primarily intended for transactions involving properties valued at $100,000 or more, particularly when the transferor is a nonresident of Colorado. The form helps ensure that any applicable Colorado income tax withholding is properly reported and remitted to the Colorado Department of Revenue.

Who needs to complete the DR 1083 form?

Any transferor who is selling real property in Colorado must complete the DR 1083 form if Colorado tax is withheld from the sale proceeds. This includes individuals, estates, corporations, and trusts. If multiple transferors are involved, each must submit a separate DR 1083, unless they are spouses holding the property jointly and both are subject to the same withholding rules.

What information is required on the DR 1083 form?

The form requires various details, including:

Completing these sections accurately is crucial to ensure compliance with Colorado tax regulations.

What happens if the DR 1083 form is not filed on time?

If the DR 1083 form is not filed within 30 days of the closing date, the title insurance company or the individual responsible for closing may face penalties. The penalty can be either $500 or 10% of the amount that was required to be withheld, up to a maximum of $2,500. Timely submission of the form is essential to avoid these penalties and ensure compliance with state tax laws.

Filling out the DR 1083 form in Colorado can be a straightforward process, but many individuals make common mistakes that can lead to complications. One frequent error is failing to provide accurate names and addresses. The form requires the transferor's full name and address, and if multiple transferors are involved, each must be listed separately unless they are spouses holding the property jointly. Omitting or miswriting this information can delay processing.

Another common mistake occurs with the selection of the transferor type. The form has specific checkboxes for individuals, estates, corporations, and trusts. Failing to check the appropriate box or incorrectly specifying "other" without clarity can lead to confusion regarding the transferor's legal status, potentially complicating the transaction.

Many people also overlook the importance of providing the correct Social Security Number (SSN) or Colorado Account Number. This information is crucial for identification purposes. If the transferor is a corporation, the Federal Employer Identification Number (FEIN) must be provided. Missing or incorrect numbers can result in delays or penalties.

Another significant error involves the property type description. The form asks for the type of property sold—residential, commercial, etc. Providing vague or inaccurate descriptions can lead to misunderstandings about the tax implications of the sale.

Additionally, mistakes often occur in the selling price section. The selling price of the property must reflect the contract sales price accurately. Some individuals mistakenly include interest or other unrelated fees, which can skew the figures and lead to incorrect tax calculations.

Completing the affirmation section also presents challenges. Transferors must select the correct affirmation type based on their residency or business status. Misunderstanding which affirmation applies can lead to incorrect withholding tax assessments.

People frequently neglect to check the box indicating whether Colorado tax was withheld. This oversight can result in complications, especially if the tax is indeed withheld but not reported correctly on the form.

Another mistake involves the submission deadline. The DR 1083 must be filed within 30 days of the closing date. Failing to meet this deadline can lead to penalties, which can be significant. Individuals often underestimate the importance of timely filing.

Lastly, individuals sometimes forget to include the necessary supporting documentation, such as the DR 1079, if applicable. This omission can result in the form being returned or delayed, causing further issues with the transaction.

By being aware of these common pitfalls and taking care to avoid them, individuals can ensure a smoother process when completing the DR 1083 form for Colorado real property transactions.

The DR 1083 form is essential for reporting the conveyance of real property interests in Colorado. When completing this form, you may also need to use several other documents to ensure compliance with state regulations. Below is a list of commonly used forms that accompany the DR 1083.

Using these forms alongside the DR 1083 helps ensure a smooth transaction and compliance with Colorado tax laws. Make sure to complete each document accurately and submit them within the required timeframes to avoid any penalties.

The DR 1083 form from Colorado serves a specific purpose in the context of real property transactions. Several other documents share similarities with this form, primarily in their function related to property transfers and tax implications. Below is a list of seven documents that are similar to the DR 1083 form, along with explanations of their similarities.

When filling out the DR 1083 form for Colorado, it’s essential to follow specific guidelines to ensure accuracy and compliance. Here’s a list of things you should and shouldn’t do:

Here are five common misconceptions about the DR 1083 Colorado form:

This is not true. While the form is often used by Colorado residents, it is also required for nonresidents who sell real property in Colorado. Nonresidents may still be subject to Colorado income tax on gains from the sale.

Many believe that the form is only necessary when tax is withheld. However, it must be filed whenever Colorado tax would have been withheld, even if an affirmation is signed that exempts the transferor from withholding.

Some people think there's no rush to file. In reality, the DR 1083 must be submitted within 30 days of the closing date. Missing this deadline can lead to penalties.

This is a common misunderstanding. Corporations, estates, and trusts also need to complete this form if they are involved in the sale of Colorado real estate.

Many assume that the DR 1083 is standalone. However, it often needs to be filed alongside the DR 1079 form, especially when tax is withheld. Both forms work together to ensure compliance.

Filling out the DR 1083 form is an important step when transferring real property in Colorado. Here are some key takeaways to help you navigate the process:

By following these guidelines, you can ensure that you fill out the DR 1083 form accurately and comply with Colorado regulations.