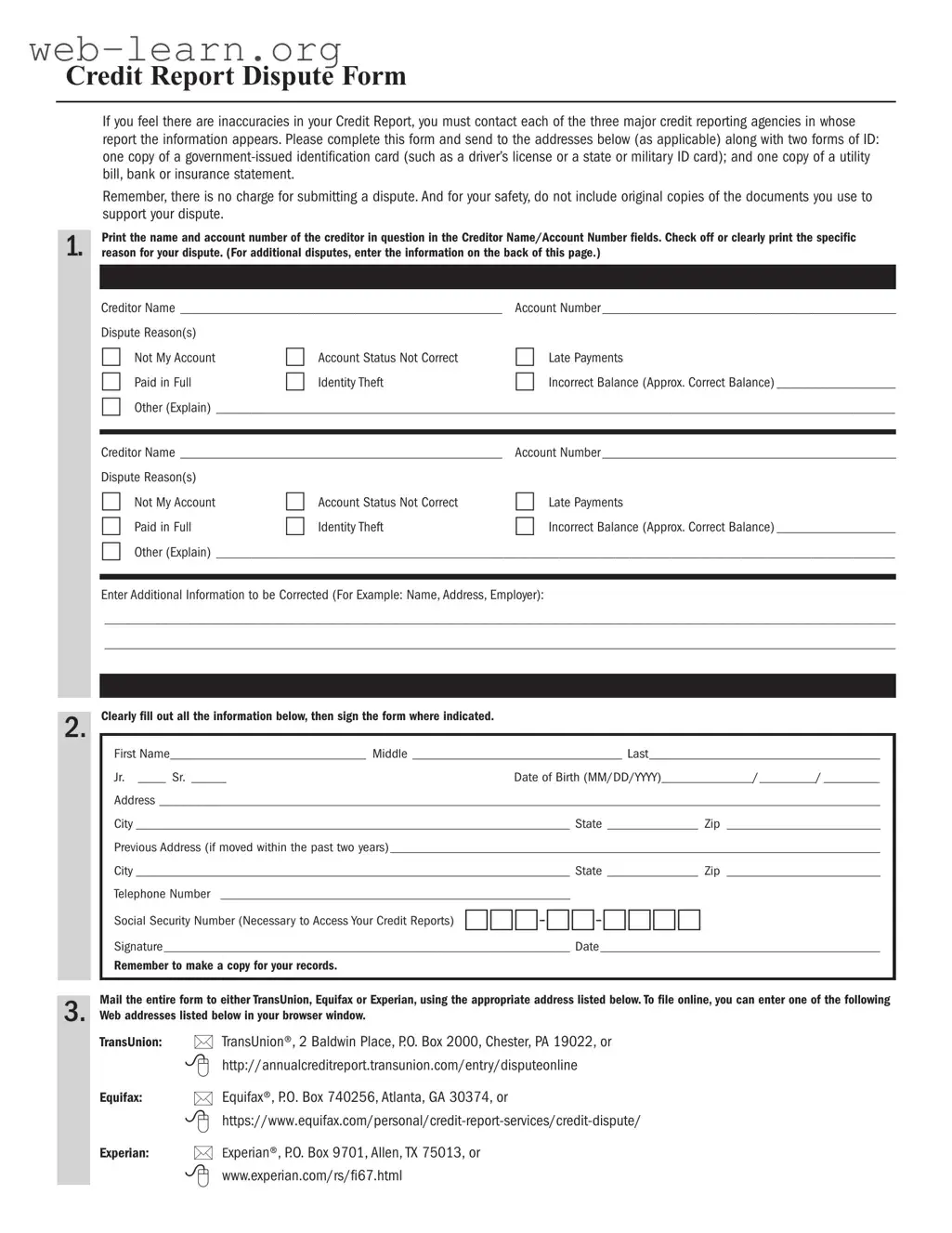

When reviewing your credit report, you may find inaccuracies that could negatively impact your credit score. The Credit Report Dispute form is an essential tool for addressing these discrepancies. This form allows you to formally challenge any incorrect information, whether it pertains to personal details, account statuses, or payment histories. By submitting this form, you initiate a process that requires credit reporting agencies to investigate your claims. It's important to include specific details about the inaccuracies, supporting documentation, and any relevant personal information. Completing the form accurately can help ensure that your dispute is taken seriously and resolved in a timely manner. Understanding how to effectively use the Credit Report Dispute form empowers you to take control of your financial future and protect your credit standing.

| Fact Name | Description |

|---|---|

| Purpose | The Credit Report Dispute form is used to challenge inaccuracies in a consumer's credit report. |

| Consumer Rights | Under the Fair Credit Reporting Act (FCRA), consumers have the right to dispute incorrect information. |

| Submission Process | Consumers can submit the dispute form online, by mail, or by phone, depending on the credit reporting agency. |

| Timeframe for Response | Credit reporting agencies must investigate disputes within 30 days of receiving the form. |

| Supporting Documentation | Consumers should include any supporting documents that substantiate their claims when submitting the form. |

| State-Specific Forms | Some states may have their own specific dispute forms, governed by state laws such as California's Consumer Credit Reporting Agencies Act. |

| Impact on Credit Score | Disputing an item does not directly affect a consumer's credit score, but the resolution may. |

| Multiple Agencies | Disputes must be filed with each credit reporting agency that contains the inaccurate information. |

| Follow-Up | Consumers should follow up with the credit reporting agency if they do not receive a response within the required timeframe. |

| Outcome Notification | After the investigation, consumers will receive a summary of the findings and any changes made to their credit report. |

Once you have the Credit Report Dispute form in hand, it’s time to start filling it out. This process is straightforward and can help you address any inaccuracies on your credit report. Take your time and ensure that all the information is accurate before submitting the form.

After completing the form, make a copy for your records before sending it to the appropriate credit reporting agency. Keep an eye on your mailbox or email for any updates regarding your dispute.

What is a Credit Report Dispute Form?

A Credit Report Dispute Form is a document that allows you to formally challenge inaccuracies or errors on your credit report. When you notice something that doesn’t seem right—like incorrect personal information, accounts that don’t belong to you, or wrong payment histories—you can use this form to notify the credit reporting agency. This process helps ensure that your credit report accurately reflects your financial history.

How do I fill out the Credit Report Dispute Form?

Filling out the Credit Report Dispute Form is straightforward. Start by providing your personal information, including your name, address, and Social Security number. Next, identify the specific items you wish to dispute. Clearly explain why you believe the information is incorrect. Attach any supporting documents, such as bank statements or payment receipts, to strengthen your case. Make sure to review the form for accuracy before submitting it.

What happens after I submit my dispute?

Once you submit your dispute, the credit reporting agency will investigate the claim. They typically have 30 days to respond. During this time, they will reach out to the creditor or lender involved to verify the information. If they find that your claim is valid, they will correct the error and send you an updated credit report. If the dispute is not resolved in your favor, you can ask for a statement of your dispute to be added to your credit report.

Can I dispute my credit report online?

Yes, many credit reporting agencies offer online dispute options. This can be a quicker way to submit your dispute compared to mailing a physical form. To do this, visit the agency's website, navigate to the dispute section, and follow the instructions provided. You will need to create an account or log in to submit your dispute online. Just remember to keep copies of any correspondence for your records.

Filling out a Credit Report Dispute form can be straightforward, but many people make common mistakes that can hinder their efforts. One frequent error is providing incomplete information. When personal details, such as name, address, or Social Security number, are missing, it can delay the dispute process.

Another mistake is failing to specify the items being disputed. It is essential to clearly identify the accounts or entries that are incorrect. Without this clarity, the credit bureau may not understand which items need to be investigated.

Some individuals neglect to include supporting documentation. Evidence such as payment receipts or correspondence with creditors can strengthen a dispute. Without these documents, the credit bureau may not have enough information to resolve the issue.

Additionally, people often overlook the importance of checking their credit report thoroughly before filing a dispute. Errors may be overlooked, leading to disputes that could have been avoided. A careful review helps ensure that only legitimate errors are challenged.

Another common oversight is not keeping a copy of the dispute form. Retaining a copy for personal records is crucial. This documentation can be useful if follow-up is needed or if the dispute is not resolved satisfactorily.

Some filers fail to provide a clear explanation of why they believe the information is incorrect. A concise and specific statement can guide the credit bureau in their investigation. A vague explanation may result in a lack of action.

People also sometimes forget to sign and date the form. An unsigned form can lead to automatic rejection. Ensuring that all required fields are filled out and signed is a vital step in the process.

Lastly, individuals often miss the deadline for submitting disputes. Credit bureaus have specific timelines for handling disputes. It is important to submit the form promptly to ensure that it is addressed in a timely manner.

When disputing information on your credit report, several other forms and documents may be helpful to support your case. These documents can provide additional context or evidence that can strengthen your dispute. Here’s a list of commonly used forms and documents that often accompany a Credit Report Dispute form:

Gathering these documents can help ensure that your dispute is well-supported and increases the chances of a successful resolution. Always keep copies of everything you submit for your records.

The Credit Report Dispute form is important for addressing inaccuracies in your credit report. Here are ten other documents that are similar to it, along with their similarities:

When filling out a Credit Report Dispute form, it is essential to approach the process carefully. Here is a list of things you should and shouldn't do to ensure your dispute is handled effectively.

By following these guidelines, you can improve the chances of a successful resolution to your credit report dispute.

Understanding the Credit Report Dispute form is crucial for anyone looking to correct inaccuracies in their credit report. However, several misconceptions can lead to confusion. Here are nine common misunderstandings:

By clarifying these misconceptions, individuals can better navigate the process of disputing inaccuracies in their credit reports and take control of their financial health.

When filling out and using the Credit Report Dispute form, it is essential to follow certain guidelines to ensure an effective process. Below are key takeaways to consider: