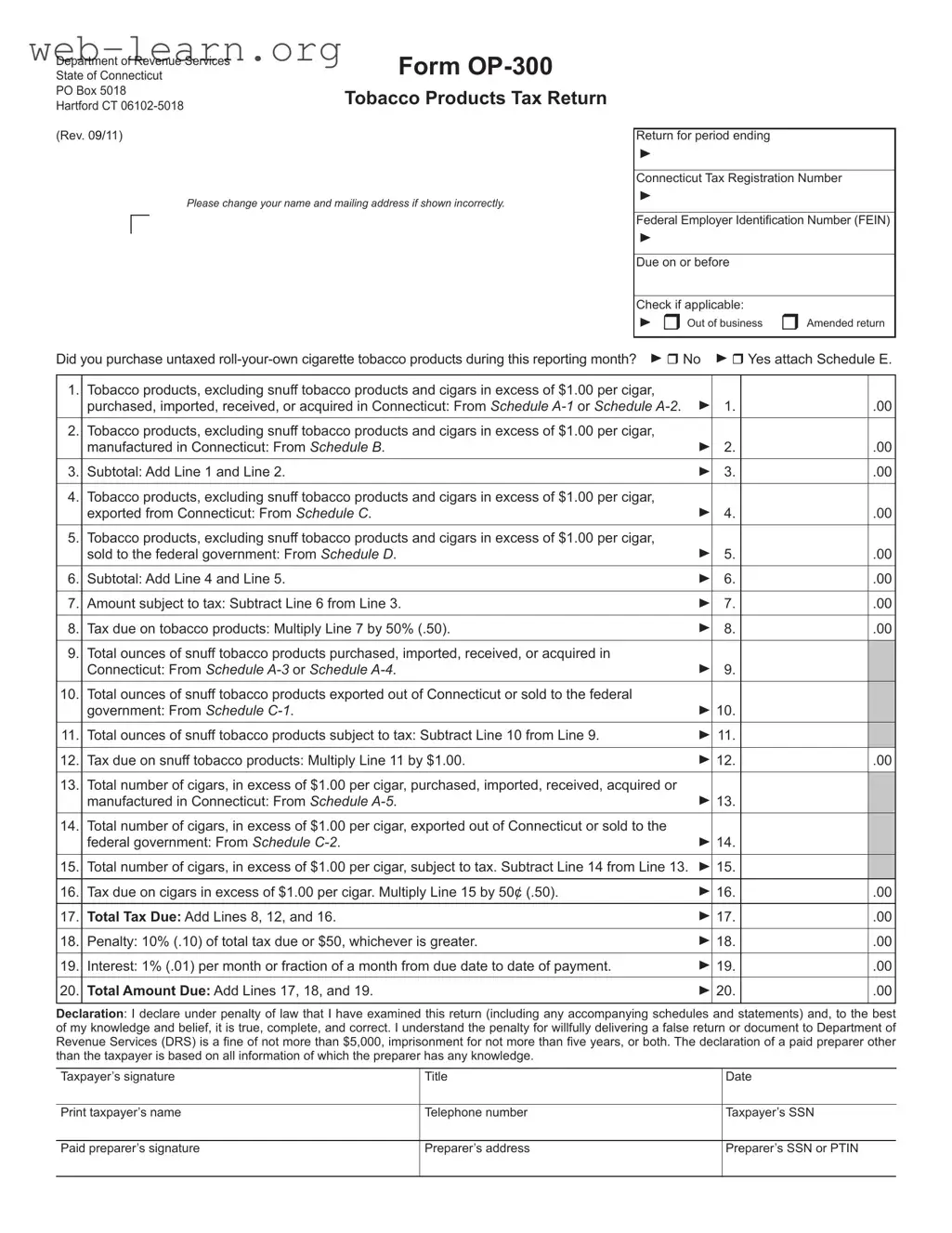

The Connecticut Op 300 form is a crucial document for businesses involved in the sale and distribution of tobacco products within the state. This form serves as the Tobacco Products Tax Return, requiring detailed reporting of various tobacco items, including cigars, snuff, and roll-your-own cigarette tobacco. Businesses must provide their Connecticut Tax Registration Number and Federal Employer Identification Number (FEIN) on the form. It is essential to indicate whether the business is out of operation or if the return is amended. The form requires taxpayers to report the total amount of tobacco products purchased, manufactured, and exported, along with the corresponding tax calculations. Each section of the form guides users through the necessary calculations, ensuring that all taxable amounts are accurately recorded. Additionally, it outlines the penalties and interest that may apply if payments are not made on time. By completing the Op 300 form accurately and submitting it by the due date, businesses can comply with state regulations and avoid potential penalties.

| Fact Name | Details |

|---|---|

| Governing Law | The Connecticut Op 300 form is governed by the Connecticut General Statutes, specifically §12-285, which pertains to the taxation of tobacco products. |

| Purpose | This form serves as the Tobacco Products Tax Return, allowing businesses to report and pay taxes on tobacco products sold or manufactured in Connecticut. |

| Filing Frequency | Taxpayers must file the Op 300 form monthly, with returns due by the 25th day of the following month. |

| Penalties for Late Filing | Failure to file by the due date may result in a penalty of 10% of the total tax due or a minimum of $50, whichever is greater. |

| Signature Requirement | The form must be signed by the taxpayer, who can be the owner, a partner, or a principal officer of the business. |

| Electronic Payment Option | Taxpayers can make electronic payments through the Taxpayer Service Center, facilitating easier and timely tax payments. |

| Supporting Schedules | Additional schedules, such as Schedule A-1 and Schedule B, must be attached to report specific details about tobacco products purchased or manufactured. |

Once you have gathered the necessary information, you can begin filling out the Connecticut Op 300 form. This form must be completed accurately and submitted on time to avoid any penalties or interest charges. Below are the steps to guide you through the process.

The Connecticut OP-300 form is used to report and pay the tobacco products tax in the state of Connecticut. This form is required for distributors who purchase, import, or manufacture tobacco products within the state. It ensures compliance with state tax regulations and provides a means for calculating the tax due on these products.

Any individual or business that acts as a distributor of tobacco products in Connecticut must file the OP-300 form. This includes those who purchase, import, or manufacture tobacco products, as well as those who sell to the federal government. Even if no tax is due, filing is still required.

The OP-300 form must be filed by the twenty-fifth day of the month following the reporting period. For example, the return for January must be submitted by February 25. Timely filing is essential to avoid penalties and interest.

If you are no longer in business, you should check the "Out of business" box on the OP-300 form. This indicates to the Department of Revenue Services that you will not be filing future returns. It is important to ensure that all prior obligations are settled before marking this box.

If you need to correct information on a previously filed OP-300 form, check the "Amended return" box. This will allow you to submit the corrected information and ensure that your tax records are accurate. Be sure to include all necessary schedules and documentation with your amended return.

The form requires various details, including your Connecticut Tax Registration Number, Federal Employer Identification Number (FEIN), and specific figures related to tobacco products purchased, manufactured, exported, or sold. Additionally, you must provide a declaration affirming the accuracy of the information submitted.

You can pay the tax electronically through the Taxpayer Service Center (TSC) by visiting www.ct.gov/TSC. Alternatively, if you prefer to pay by check, make it payable to the Commissioner of Revenue Services and mail it to the address specified on the form. Ensure that payment is made by the due date to avoid penalties.

Failure to file the OP-300 form by the due date may result in penalties and interest. The penalty is 10% of the total tax due or $50, whichever is greater. Additionally, interest accrues at a rate of 1% per month until the tax is paid. Timely filing and payment are crucial to avoid these additional costs.

If you need further assistance, you can contact the Excise Taxes Unit at 860-541-3224 during business hours. For forms and publications, visit the Department of Revenue Services website at www.ct.gov/DRS. There, you can download and print necessary documents and find additional information regarding tobacco tax regulations.

Completing the Connecticut OP-300 form can be a straightforward process, but many individuals make common mistakes that can lead to delays or complications. Understanding these pitfalls can help ensure that your submission is accurate and timely.

One frequent error is neglecting to check the appropriate box regarding the purchase of untaxed roll-your-own cigarette tobacco products. If you select "Yes," it is essential to attach Schedule E. Failing to do so may result in your form being returned or processed incorrectly. Always double-check this section to ensure compliance.

Another common mistake occurs when individuals forget to include their Connecticut Tax Registration Number and Federal Employer Identification Number (FEIN). These numbers are crucial for identifying your business and ensuring that your tax return is processed correctly. Leaving these fields blank can delay your filing and potentially incur penalties.

Many people also overlook the requirement to sign the form. The owner, partner, or principal officer must sign the return. A missing signature can lead to the return being considered incomplete, which may result in additional fines or complications.

Additionally, some taxpayers mistakenly assume that they do not need to file if no tax is due. This is not the case. All taxpayers are required to submit a return for each calendar month, regardless of whether any tax is owed. Ignoring this requirement can lead to penalties.

Another area where errors often occur is in the calculations of the tax due. It is vital to ensure that all figures are added and subtracted correctly. A simple miscalculation can result in underpayment or overpayment, both of which can create issues down the line. Taking the time to review your math can save you from future headaches.

Finally, many individuals fail to use blue or black ink when completing the form. This may seem trivial, but it is a requirement that helps ensure clarity and legibility. Using other colors can result in processing delays or misinterpretations of your information.

By being aware of these common mistakes, you can approach the Connecticut OP-300 form with confidence. Careful attention to detail will help ensure that your submission is accurate and complete, allowing you to fulfill your tax obligations smoothly.

The Connecticut OP-300 form is a crucial document for reporting tobacco products tax. However, several other forms and documents are often used alongside it to ensure compliance with state regulations. Below is a list of these related forms and documents.

Using these forms in conjunction with the OP-300 ensures accurate reporting and compliance with Connecticut tax laws. Proper documentation is essential for avoiding penalties and ensuring a smooth tax filing process.

The Connecticut Op 300 form is an important document for reporting tobacco product taxes. It shares similarities with several other forms used in tax reporting and compliance. Below is a list of six documents that are comparable to the Op 300 form, highlighting their key similarities.

When filling out the Connecticut Op 300 form, it is essential to follow specific guidelines to ensure accuracy and compliance. Below is a list of things you should and shouldn't do:

Misconceptions about the Connecticut OP-300 form can lead to confusion and errors in tax reporting. Here are six common misunderstandings:

Understanding these misconceptions can help ensure that taxpayers fulfill their obligations accurately and on time.

Here are key takeaways about filling out and using the Connecticut OP-300 form:

Ensure accuracy to avoid penalties, which can include fines or imprisonment for false reporting.