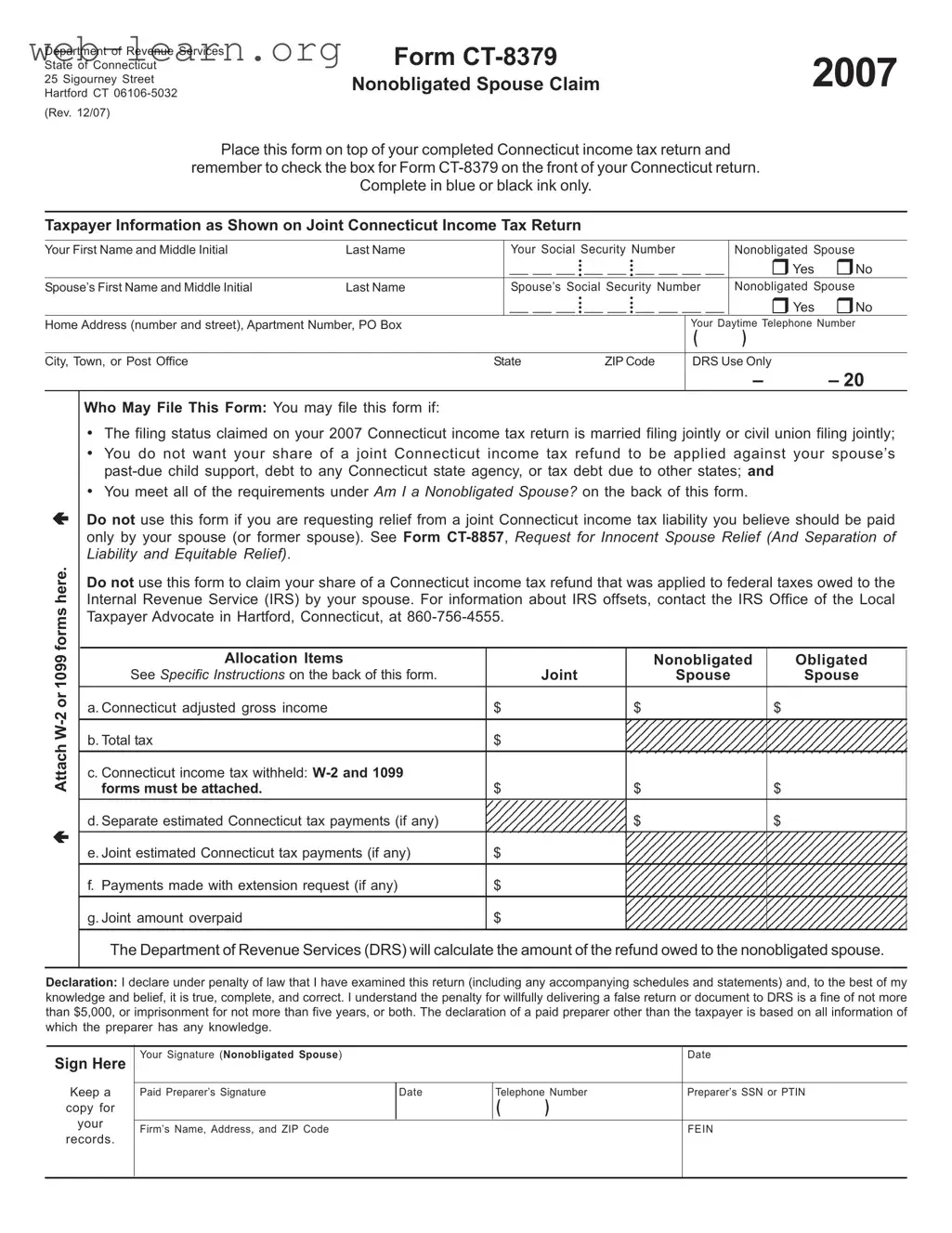

The Connecticut 8379 form, officially known as the Nonobligated Spouse Claim, serves a vital purpose for individuals who find themselves in a challenging financial situation due to their spouse’s debts. Specifically designed for those who filed a joint income tax return, this form allows the nonobligated spouse to claim their rightful share of any tax refund that may be applied against their partner's past-due obligations, such as child support or tax debts owed to the state. To utilize this form, it is essential to meet specific criteria, including having filed jointly while not being responsible for any debts themselves. When completing the form, taxpayers must provide accurate information regarding their income, tax payments, and any relevant documentation, such as W-2 or 1099 forms, to ensure a smooth processing of their claim. This form must be placed on top of the completed Connecticut income tax return, making it clear to the Department of Revenue Services that a claim is being made. Understanding the intricacies of the Connecticut 8379 form can empower individuals to reclaim their financial standing and ensure that they are not unfairly penalized for their spouse's financial missteps.

| Fact Name | Details |

|---|---|

| Form Purpose | The Connecticut Form CT-8379 is designed for nonobligated spouses to claim their share of a joint tax refund that may have been applied against their spouse's past-due debts. |

| Eligibility Criteria | To file this form, the taxpayer must have filed a joint return and must not owe any past-due child support or debts to Connecticut state agencies. |

| Filing Requirements | This form must be placed on top of the completed Connecticut income tax return and the box for Form CT-8379 must be checked on the front of the return. |

| Governing Law | Form CT-8379 is governed by Connecticut General Statutes, specifically those relating to tax refunds and obligations of spouses in tax matters. |

| Nonobligated Spouse Definition | A nonobligated spouse is one who meets specific criteria, including not owing any debts that would affect the joint tax refund. |

| Refund Calculation | The Department of Revenue Services will compute the refund owed to the nonobligated spouse based on the joint overpayment reported on the tax return. |

Filling out the Connecticut 8379 form is an important step in ensuring that your share of a joint tax refund is processed correctly. Once you have completed the form, it should be placed on top of your Connecticut income tax return. Remember to check the box indicating that you have included Form CT-8379 on your return.

What is the purpose of the Connecticut 8379 form?

The Connecticut 8379 form, also known as the Nonobligated Spouse Claim, is used to request a refund of your share of a joint tax overpayment. This form is specifically for individuals who filed a joint income tax return but do not want their refund applied to their spouse's past-due debts, such as child support or state taxes. If you meet certain criteria, this form helps ensure that your portion of the refund is returned to you.

Who is eligible to file the Connecticut 8379 form?

You may file this form if:

If you believe your spouse should be solely responsible for the tax liability, you should not use this form. Instead, consider filing Form CT-8857 for Innocent Spouse Relief.

How do I file the Connecticut 8379 form?

To file the Connecticut 8379 form, place it on top of your completed Connecticut income tax return. Make sure to check the box indicating that you are submitting Form CT-8379 on your tax return. If you have already filed your tax return, you will need to mail the form separately to the Department of Revenue Services. Remember to attach copies of all W-2 and 1099 forms showing Connecticut income tax withheld.

What information do I need to provide on the form?

When completing the form, you will need to provide:

Ensure that all information matches what is on your joint tax return to avoid any processing delays.

What happens after I submit the Connecticut 8379 form?

Once submitted, the Department of Revenue Services will review your form and calculate the refund owed to you as the nonobligated spouse. They will determine your share of the joint overpayment. It’s important to keep a copy of the form for your records. If you have any questions about the status of your claim, you can contact the Department of Revenue Services directly.

Filling out the Connecticut 8379 form can be a straightforward process, but many people make common mistakes that can delay their claims or even lead to denials. One frequent error is failing to place the form on top of the completed Connecticut income tax return. This simple step is crucial, as it ensures that the Department of Revenue Services (DRS) processes your claim correctly. Without this, your submission may not be reviewed in a timely manner.

Another common mistake involves not checking the box for Form CT-8379 on the front of the Connecticut return. This box is a signal to the DRS that you are submitting this specific claim. If you neglect to check it, your request for a refund may be overlooked, and you could miss out on the funds that are rightfully yours.

Additionally, many individuals incorrectly fill out the taxpayer information section. It's vital to enter the names and Social Security Numbers exactly as they appear on the joint tax return. Any discrepancies can lead to confusion and delays in processing. Remember, accuracy in this section is essential.

Some people also forget to attach the required W-2 or 1099 forms showing Connecticut income tax withheld. These documents are necessary for the DRS to calculate the refund owed to the nonobligated spouse. Failing to include them can result in a rejection of your claim or a significant delay in processing.

Another mistake is misallocating income and tax amounts. It’s important to ensure that the Connecticut adjusted gross income and tax amounts are accurately reported and allocated between the nonobligated and obligated spouse. Miscalculations here can lead to incorrect refund amounts and may require you to start the process over.

People sometimes overlook the requirement for a signature. The nonobligated spouse must sign the form for it to be valid. If you forget this step, the DRS will not process your claim, and you could face further complications.

Lastly, some individuals fail to keep a copy of the completed form for their records. This oversight can be problematic if there are questions or issues later on. Keeping a copy allows you to reference your submission and provides proof of what was filed. Avoiding these common mistakes can make the process of claiming your share of a tax refund much smoother and more efficient.

The Connecticut 8379 form is an important document for individuals who want to claim their share of a tax refund while protecting it from being applied to their spouse's debts. However, it is often used in conjunction with other forms and documents that help facilitate the tax filing process. Here’s a list of some common forms and documents that might accompany the Connecticut 8379 form.

Understanding these forms and documents can simplify the tax filing process and ensure that all necessary information is submitted correctly. Always keep copies of everything you file for your records, and consult a tax professional if you have questions about your specific situation.

The Connecticut 8379 form, known as the Nonobligated Spouse Claim, shares similarities with several other tax-related documents. Each of these forms serves specific purposes related to tax filings and claims. Below is a list of seven documents that are similar to the Connecticut 8379 form:

Each of these forms plays a role in the broader context of tax filing and management, ensuring that taxpayers can navigate their obligations and rights effectively.

Filling out the Connecticut 8379 form can be straightforward if you keep a few essential guidelines in mind. Here’s a list of dos and don’ts to help you navigate the process smoothly.

By following these guidelines, you can help ensure that your claim is processed quickly and accurately. Remember, attention to detail is key!

Understanding the Connecticut 8379 form can be challenging, especially with the various misconceptions surrounding it. Here’s a list of common misunderstandings to clarify the purpose and use of this form.

By dispelling these misconceptions, individuals can better understand their rights and responsibilities when it comes to filing the Connecticut 8379 form. Always consider seeking professional advice if there are uncertainties about the process.

When filling out and using the Connecticut 8379 form, keep these key points in mind: