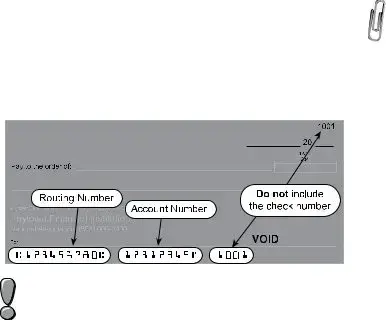

The Colorado Tax form encompasses a range of essential documents designed for individuals filing their state income tax returns. Central to this process is the DR 0104 form, which serves as the primary vehicle for reporting income and calculating tax liability for full-year residents, part-year residents, and nonresidents. Accompanying this form are various related schedules, including the DR 0104CH for voluntary contributions, the DR 0900 for individual income tax payments, and the DR 0104AD for subtractions from income. Taxpayers may also need to utilize the DR 0104PN for part-year residents and nonresidents to accurately calculate their tax obligations based on income earned within Colorado. Additionally, the DR 0104CR allows for the reporting of individual tax credits, while the DR 0104US is designated for consumer use tax reporting. The instructions booklet provides detailed guidance on completing these forms, including information about filing deadlines, residency requirements, and the necessary documentation for various credits and deductions. Understanding these components is crucial for ensuring compliance and optimizing potential tax benefits in the state of Colorado.

| Fact Name | Description |

|---|---|

| Form Types | The Colorado Tax form includes several components: DR 0104, DR 0104CH, DR 0900, DR 0104AD, DR 0158-I, DR 0104PN, DR 0104US, and DR 0104CR. |

| Filing Deadline | Tax returns must be postmarked by April 15. An automatic extension to file until October 15 is available, but payment is still due by April 15. |

| Residency Status | Taxpayers must indicate their residency status on the form, which affects how income is taxed in Colorado. |

| Mailing Addresses | Forms must be mailed to specific addresses based on whether payment is included: one for with payment and another for without payment. |

| Governing Law | The Colorado Individual Income Tax is governed by Colorado Revised Statutes Title 39, Article 22. |

| Electronic Filing | Taxpayers are encouraged to file electronically via Revenue Online to reduce errors and processing delays. |

Filling out the Colorado Tax form is an important task that requires careful attention to detail. Completing this form accurately will help ensure that your tax return is processed smoothly and efficiently. Follow the steps below to fill out the form correctly.

After completing these steps, you can file your tax return electronically or by mail. If you choose to mail it, ensure it is postmarked by the due date. Filing electronically is recommended to minimize errors and speed up processing. Be sure to keep a copy of your completed form and any supporting documents for your records.

The Colorado Tax Form, specifically the DR 0104, is used for filing individual income tax returns for Colorado residents, part-year residents, and nonresidents who earn income from Colorado sources. This form allows taxpayers to report their income, claim deductions and credits, and calculate their tax liability based on their federal taxable income.

Individuals must file a Colorado income tax return if they meet any of the following criteria:

Even if there is no Colorado tax liability, residents must file if they are required to file a federal income tax return with the IRS.

The Colorado Tax Form is due on April 15 each year. If taxpayers need more time to file, they can request an automatic extension until October 15. However, it is important to note that this extension does not apply to the payment of taxes owed, which are still due by April 15.

Taxpayers have several options for filing their Colorado income tax return:

Filing electronically is recommended as it significantly reduces the chance of errors. If electronic filing is not possible, taxpayers can mail their completed forms as instructed.

Legal representatives or surviving spouses can file a Colorado income tax return on behalf of a deceased individual. They must indicate the deceased status on the return and attach a copy of the death certificate. It is also necessary to mark the box next to the deceased person's name and write "DECEASED" clearly on the return. For claiming refunds, the death certificate must accompany the return.

Filling out the Colorado Tax Form can be a daunting task, and many people make mistakes that can lead to processing delays or even penalties. One common error occurs when individuals do not accurately report their federal taxable income. It is crucial to refer to your federal income tax return to complete this line correctly. If you enter a total income amount instead of the taxable income, your tax liability could be overstated. This mistake can easily be avoided by double-checking the relevant line on your federal return before transferring the information.

Another frequent mistake involves the residency status selection. Taxpayers must mark the appropriate box to indicate whether they are full-year residents, part-year residents, or nonresidents. Failing to do so can lead to incorrect tax calculations, as the tax rates and obligations differ based on residency status. Always ensure that your residency status is accurately represented on the form to avoid complications.

Many people also neglect to include necessary supporting documentation when claiming certain tax credits or subtractions. For example, if you are claiming credits from a pass-through entity, you must attach the federal Schedule K-1 or another statement that details the type and amount of the credit. Without this documentation, your claim may be denied, resulting in a higher tax liability than anticipated.

Additionally, some taxpayers make the mistake of not filing electronically. While it is possible to submit a paper return, electronic filing significantly reduces the risk of errors. The Colorado Department of Revenue provides a secure online filing option that is user-friendly and helps ensure that all necessary information is accurately reported. If you are able to file electronically, it is highly recommended.

Another common pitfall is not properly calculating the Colorado taxable income. This figure is derived from your federal taxable income and requires careful attention to detail. Be sure to subtract any applicable subtractions from the DR 0104AD schedule accurately. An error in this calculation can lead to an incorrect tax amount owed, which could result in penalties or interest on unpaid taxes.

Lastly, some taxpayers overlook the importance of keeping a copy of their submitted tax return and all supporting documents. This practice is essential for future reference, especially if the Colorado Department of Revenue has questions or requires additional information. Maintaining thorough records can save you time and stress should any issues arise after filing.

When preparing to file your Colorado tax return, you may encounter several additional forms and documents that can assist you in accurately reporting your income and claiming any applicable credits or deductions. Below is a list of these forms, along with a brief description of each.

Understanding these forms and how they relate to your Colorado tax return can significantly streamline the filing process. Each document serves a specific purpose and can help ensure that you are compliant with state tax regulations while maximizing your potential refunds or minimizing your tax liabilities.

When filling out the Colorado Tax form, it’s important to follow certain guidelines to ensure a smooth process. Here’s a list of things you should and shouldn’t do:

By following these tips, you can navigate the Colorado Tax form with greater ease and confidence.

This is not true. The form is designed for full-year residents, part-year residents, and non-residents who earn income in Colorado. Anyone who has taxable income from Colorado sources must file.

An extension allows extra time to file your return, but it does not extend the time to pay any taxes owed. Payments are still due by the original deadline to avoid penalties and interest.

Not all income is taxable. Certain types of income, such as some retirement benefits or specific types of disability payments, may be exempt. It's essential to review the guidelines to determine what qualifies.

This is incorrect. Tax credits can be claimed regardless of whether you file electronically or on paper. However, electronic filing may simplify the process and reduce the risk of errors.

Many deductions and credits require additional documentation to substantiate your claims. Failing to provide this can lead to processing delays or denial of those deductions and credits.

When filling out the Colorado Tax form, consider the following key takeaways: