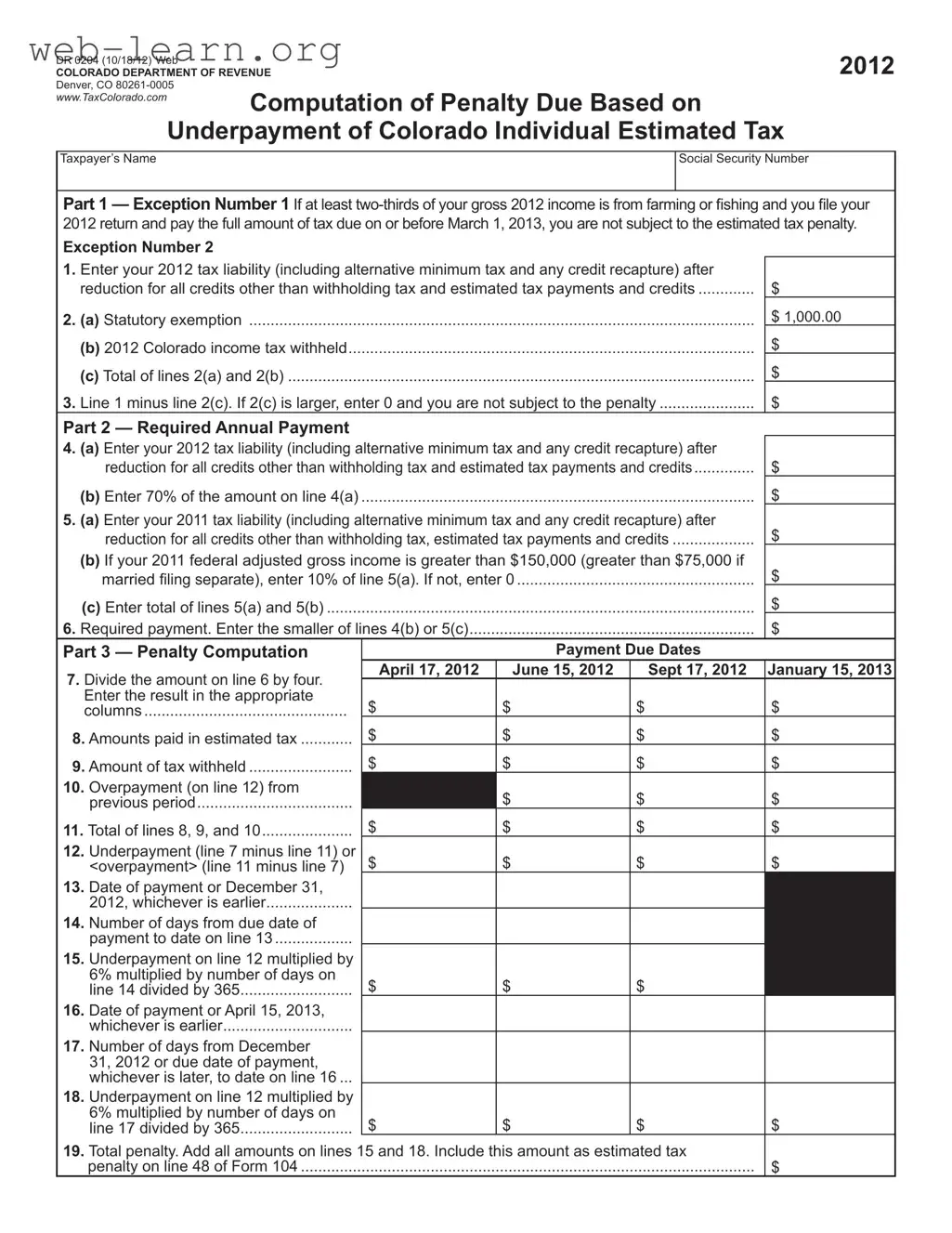

The Colorado DR 0204 form is a critical tool for taxpayers who need to compute penalties related to the underpayment of estimated individual income tax. This form outlines the specific conditions under which taxpayers may be exempt from penalties, particularly for those whose income primarily comes from farming or fishing. It breaks down the necessary calculations into clear parts, allowing individuals to determine their required annual payment based on their tax liability from the previous year or a percentage of their current year’s liability. Additionally, the form provides a detailed penalty computation section, which helps taxpayers understand how to calculate any penalties owed if they fail to meet their estimated tax payment obligations. By following the structured sections of the DR 0204, taxpayers can navigate their responsibilities and avoid unnecessary penalties, ensuring compliance with Colorado tax laws.

| Fact Name | Description |

|---|---|

| Purpose | The DR 0204 form is used to compute the penalty for underpayment of Colorado individual estimated tax. |

| Exceptions | Taxpayers are exempt from penalties if at least two-thirds of their gross income is from farming or fishing and they file their return by March 1, 2013. |

| Payment Schedule | Estimated tax payments are due in four installments: April 17, June 15, September 17, and January 15 of the following year. |

| Governing Laws | This form is governed by Colorado Revised Statutes, specifically those related to income tax and estimated tax payments. |

Filling out the Colorado DR 0204 form requires careful attention to detail. This form is used to compute any penalties due based on underpayment of Colorado individual estimated tax. It is important to ensure that all information is accurate and complete to avoid potential issues with the Department of Revenue.

After completing the form, review all entries for accuracy. It is advisable to keep a copy for your records before submitting it to the Colorado Department of Revenue.

What is the Colorado DR 0204 form?

The Colorado DR 0204 form is used to calculate penalties for underpayment of estimated taxes by individuals in Colorado. It outlines the process for determining if a taxpayer owes a penalty due to insufficient estimated tax payments throughout the year.

Who needs to file the DR 0204 form?

Taxpayers who are required to make estimated tax payments and who do not meet specific exceptions must file this form. If you underpaid your estimated tax payments, this form helps you compute any penalties owed.

What are the exceptions to the estimated tax penalty?

How is the required annual payment calculated?

The required annual payment is the lesser of:

What information is needed to complete the DR 0204 form?

You will need your tax liability for the current year, any estimated tax payments made, the amount of tax withheld, and details of any overpayments from the previous period. This information is used to compute both your required payments and any potential penalties.

How is the penalty for underpayment computed?

The penalty is calculated based on the amount of underpayment for each installment due date. The form provides a step-by-step method to determine the penalty, which includes multiplying the underpayment by a specified interest rate and the number of days late.

What are the due dates for estimated tax payments?

Estimated tax payments are typically due on the following dates:

Can I use the annualized installment method with this form?

Yes, if your income is not received evenly throughout the year, you may elect to use the annualized installment method. This allows you to calculate your estimated payments based on actual income received during specific periods.

Where can I find more information about the DR 0204 form?

Additional information is available on the Colorado Department of Revenue's website at www.taxcolorado.com. You can also refer to FYI Income 51 for more details regarding estimated tax payments and penalties.

Filling out the Colorado DR 0204 form can be a daunting task, and mistakes can lead to unnecessary penalties. One common mistake is failing to check eligibility for exceptions. Taxpayers who earn two-thirds of their income from farming or fishing may avoid penalties if they file their 2012 return by March 1, 2013. Not being aware of this exception can lead to an unexpected penalty.

Another frequent error is incorrectly calculating the tax liability. When entering the tax liability on line 1, it’s essential to include all relevant amounts, including alternative minimum tax and any credit recapture. Omitting any of these figures can result in an inaccurate calculation, leading to potential penalties.

People often miscalculate the required annual payment as well. Lines 4 and 5 require careful attention to detail. Entering the wrong figures from previous years can skew the required payment, making it larger than necessary. This mistake can lead to overpayment or additional penalties if the actual tax owed is underestimated.

Additionally, taxpayers sometimes overlook the importance of timely payments. Each estimated tax payment has specific due dates. Missing these deadlines can result in penalties, even if the form is filled out correctly. Keeping track of these dates is crucial to avoid unnecessary fees.

Some individuals also fail to properly account for amounts paid in estimated tax or withheld. Lines 8 and 9 must be accurately filled in to reflect actual payments made. If these amounts are underestimated, the underpayment on line 12 may be higher than it should be, leading to penalties.

Another common mistake involves misunderstanding the annualized installment method. Taxpayers who do not receive income evenly throughout the year may choose this method, but they must complete the corresponding schedule accurately. Failing to do so can result in incorrect calculations of the installment payments due.

Moreover, people often neglect to check the instructions thoroughly. Each part of the form has specific guidelines that must be followed. Ignoring these instructions can lead to errors in calculations and missed opportunities for exceptions.

Finally, a lack of attention to detail in the final calculations can lead to mistakes in the total penalty. Adding up the amounts on lines 15 and 18 must be done carefully. A simple miscalculation here can result in a larger penalty than necessary, impacting overall tax liability.

The Colorado DR 0204 form is essential for taxpayers to compute penalties related to underpayment of estimated taxes. However, several other forms and documents are often used in conjunction with it to ensure compliance with tax regulations and to facilitate accurate reporting. Below is a list of these documents, each accompanied by a brief description.

Understanding these forms and documents can significantly aid taxpayers in navigating their responsibilities and ensuring compliance with Colorado tax laws. Each document plays a unique role in the overall process of tax reporting and payment, making them integral to effective tax management.

When filling out the Colorado DR 0204 form, there are important dos and don'ts to keep in mind. Following these guidelines can help ensure that your submission is accurate and complete.

By following these guidelines, you can navigate the Colorado DR 0204 form with confidence and minimize any potential issues.

Understanding the Colorado DR 0204 form can be challenging, and several misconceptions exist about its purpose and requirements. Below are ten common misconceptions, along with clarifications.

By addressing these misconceptions, taxpayers can better understand their obligations and avoid unnecessary penalties related to estimated tax payments in Colorado.

When filling out the Colorado DR 0204 form, keep these key takeaways in mind: