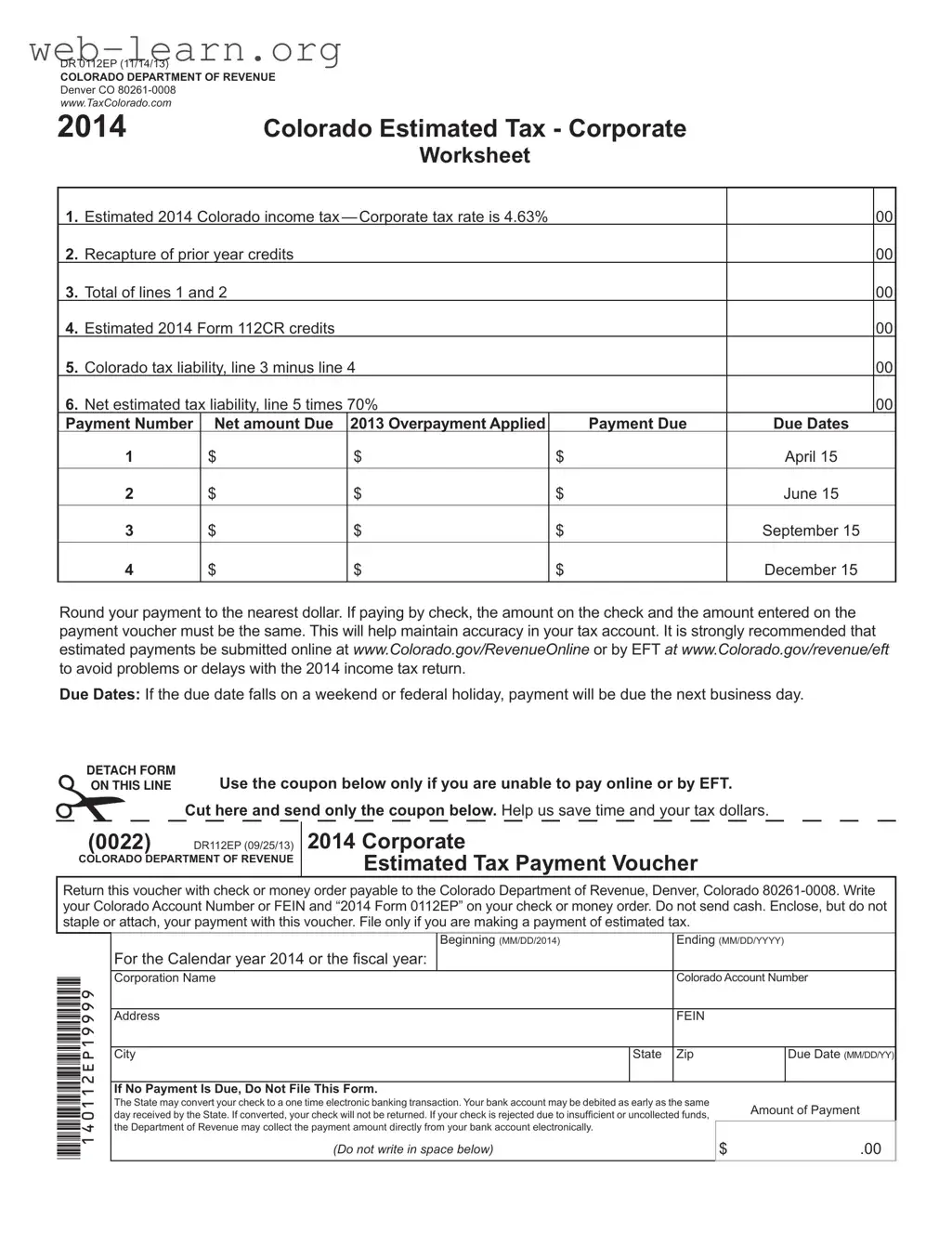

The Colorado 1Dr 0112Ep form serves as a vital tool for corporations in managing their estimated tax obligations for the year 2014. This form outlines the necessary steps and calculations for determining the estimated Colorado income tax liability, which is set at a corporate tax rate of 4.63%. Corporations must account for prior year credits, ensuring that these are recaptured appropriately. The form provides a structured worksheet where businesses can detail their estimated tax liability and the applicable credits, ultimately leading to the net estimated tax owed. Payment deadlines are clearly specified, with quarterly payments due on April 15, June 15, September 15, and December 15. It is essential for corporations to adhere to these deadlines to avoid penalties. The form also encourages electronic payments to streamline the process and reduce the likelihood of errors. By utilizing the Colorado 1Dr 0112Ep form, corporations can effectively manage their tax responsibilities while ensuring compliance with state regulations.

| Fact Name | Details |

|---|---|

| Form Purpose | The DR 0112EP form is used for making estimated tax payments for corporations in Colorado for the year 2014. |

| Tax Rate | The corporate tax rate for Colorado is set at 4.63% for the year 2014. |

| Payment Due Dates | Payments are due on April 15, June 15, September 15, and December 15 of 2014. |

| Payment Method | It is recommended to submit payments electronically via the Colorado Department of Revenue's website to avoid issues. |

| Governing Law | The form is governed by Colorado Revised Statutes related to corporate income tax and estimated payments. |

Completing the Colorado 1Dr 0112Ep form requires careful attention to detail. This form is used for submitting estimated corporate tax payments for the year 2014. After filling out the form, ensure that you submit it according to the specified due dates to avoid any penalties.

The Colorado 1Dr 0112Ep form, also known as the Corporate Estimated Tax Payment Voucher, is used by corporations to calculate and remit estimated tax payments for the tax year 2014. This form is essential for corporations that expect to owe more than $5,000 in Colorado income tax.

Corporations that anticipate a net tax liability exceeding $5,000 for the year must file this form. This requirement applies even if the corporation has a short taxable year or if there has been a change in the accounting period. In such cases, income must be estimated as if it were for a full 12-month year.

To calculate your estimated tax liability, follow these steps:

Payments are due on the following dates:

If a due date falls on a weekend or federal holiday, the payment is due the next business day.

It is highly recommended to submit payments online through the Colorado Department of Revenue's website or via Electronic Funds Transfer (EFT). If you are unable to pay online, you may use the payment voucher and send a check or money order. Ensure that the amount on your check matches the amount entered on the payment voucher.

Failure to remit estimated tax payments on time will result in an Estimated Tax Penalty. This penalty is calculated for each missed or late payment. For specifics on penalty calculations, refer to Form 205, Underpayment of Corporate Estimated Tax.

Yes, electronic payments are encouraged. You can make payments online at www.Colorado.gov/RevenueOnline or set up EFT payments. EFT services are free and allow for scheduling payments up to 12 months in advance.

Additional information, forms, and FYI publications are available at www.TaxColorado.com. For assistance, you may also contact the Colorado Department of Revenue at 303-238-SERV (7378).

Filling out the Colorado 1Dr 0112Ep form can be a straightforward process, but mistakes can lead to complications. One common error is failing to include the correct Colorado Account Number or Federal Employer Identification Number (FEIN). This information is essential for the Colorado Department of Revenue to accurately process your payment. Omitting or miswriting these numbers can delay processing and create issues with your tax account.

Another frequent mistake is neglecting to calculate the estimated tax liability accurately. Taxpayers should ensure that they follow the calculation steps outlined in the form. Specifically, they must correctly add the estimated income tax and any recapture of prior year credits. Errors in these calculations can lead to underpayment or overpayment, both of which can have financial consequences.

Some individuals also overlook the importance of rounding the payment amount to the nearest dollar. The instructions clearly state this requirement, yet many people still submit amounts that do not comply. This can result in confusion and may require additional correspondence with the Department of Revenue.

Moreover, failing to submit the payment on time is another mistake that can lead to penalties. The due dates for payments are set, and if they fall on a weekend or holiday, payments are due the next business day. Missing these deadlines can incur late fees, which can add up quickly.

In addition, some taxpayers mistakenly think they can file the form even if no payment is due. The instructions clearly state that if no payment is due, the form should not be filed. Ignoring this guideline can lead to unnecessary complications and additional paperwork.

Using an incorrect method of payment is also a common error. Taxpayers should ensure that the payment method they choose matches the method indicated on the form. For instance, if you are paying by check, the amount on the check must match the amount entered on the voucher. Discrepancies can cause processing delays.

Another mistake involves not keeping a copy of the submitted form and payment for personal records. This is essential for tracking purposes and for any future inquiries regarding your tax account. Without proper documentation, it may be challenging to resolve any issues that arise later.

Some people also fail to take advantage of electronic payment options. Submitting payments online or via Electronic Funds Transfer (EFT) can reduce the likelihood of errors and provide instant confirmation of payment. Ignoring these options can lead to unnecessary complications.

Lastly, not reviewing the form for completeness before submission is a critical oversight. Each section should be double-checked to ensure that all required fields are filled out correctly. A thorough review can prevent many of the issues mentioned above and facilitate a smoother process.

The Colorado 1Dr 0112Ep form is an essential document for corporations to estimate their tax liabilities for the year. However, several other forms and documents may accompany it to ensure compliance and accuracy in tax reporting. Here are five commonly used documents:

Utilizing these documents alongside the Colorado 1Dr 0112Ep form can help corporations navigate their tax responsibilities more effectively. Staying organized and informed is key to maintaining compliance and avoiding penalties.

The Colorado 1Dr 0112Ep form, used for corporate estimated tax payments, shares similarities with several other tax-related documents. Each of these forms serves a unique purpose but often overlaps in functionality or intent. Here’s a breakdown of seven documents that are similar:

Understanding these forms can help navigate the complexities of tax obligations, ensuring compliance and potentially reducing liabilities. Each document has its own nuances, but they all play a crucial role in the tax landscape.

When filling out the Colorado 1Dr 0112Ep form, there are several important do's and don'ts to keep in mind to ensure a smooth process.

Many people have misunderstandings about the Colorado 1Dr 0112Ep form. Here are some common misconceptions, along with clarifications to help you better understand this important tax document.

This form is required for all corporations that expect their net tax liability to exceed $5,000, not just large corporations.

There are specific due dates for payments, typically on April 15, June 15, September 15, and December 15. Missing these dates can result in penalties.

Even if you filed last year, you must make estimated payments if your tax liability is expected to exceed $5,000 this year.

The form specifically states that cash should not be sent. Payments must be made by check or money order.

If no payment is due, you do not need to file the form. However, you should keep track of your tax liability to avoid future issues.

It is essential to use the provided worksheet to calculate the estimated tax owed before submitting the form.

Payments must be submitted using the same account number as will be used on the annual income tax return, Form 112.

Online payments are a secure option. They reduce errors and provide instant confirmation of your payment.

Understanding these points can help ensure compliance and avoid unnecessary penalties. If you have further questions, consider seeking assistance from a tax professional.

When filling out the Colorado 1Dr 0112Ep form, consider the following key takeaways: