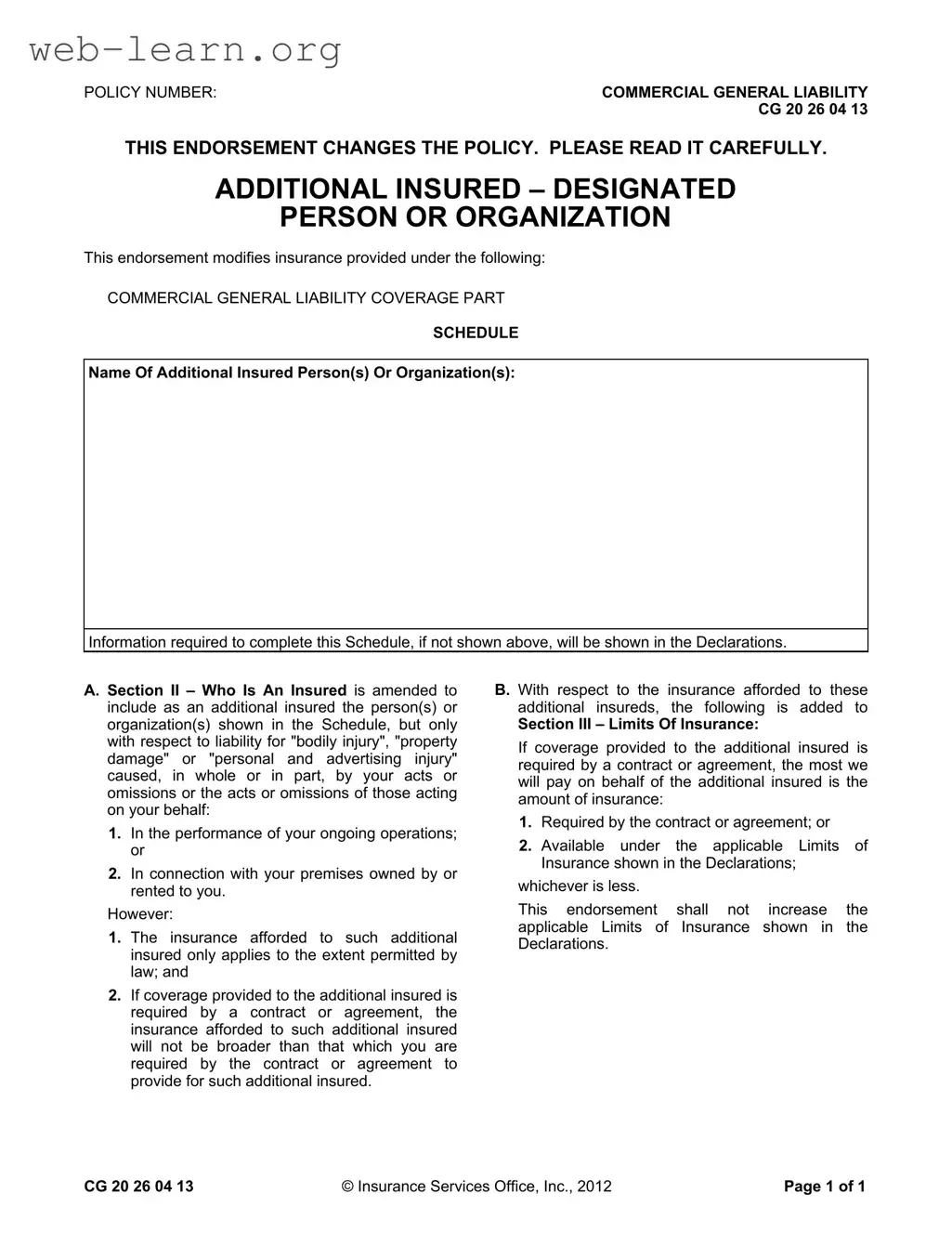

The CG 20 26 04 13 form is an important endorsement that modifies the standard Commercial General Liability (CGL) policy. This particular form introduces the concept of "additional insured," allowing specific individuals or organizations to be covered under the policy for certain liabilities. It is crucial for businesses to understand that this endorsement is not just a simple addition; it outlines specific conditions under which these additional insured parties are protected. The coverage applies primarily to liabilities arising from bodily injury, property damage, or personal and advertising injury that result from the named insured's actions or omissions, particularly in relation to ongoing operations or premises owned or rented by the insured. However, the form emphasizes that the protection granted to additional insureds is limited by existing laws and contractual obligations. If a contract stipulates certain coverage requirements, the insurance provided cannot exceed what is mandated. Additionally, the limits of insurance for these additional insured parties are clearly defined, ensuring that they align with the contractual obligations or the policy's declared limits, whichever is lower. Understanding the nuances of the CG 20 26 04 13 form is essential for businesses seeking to navigate their liability coverage effectively and ensure that all parties involved are adequately protected.

| Fact Name | Description |

|---|---|

| Policy Type | This form is an endorsement for a Commercial General Liability (CGL) policy. |

| Additional Insured | It allows for the inclusion of designated persons or organizations as additional insureds. |

| Coverage Scope | The coverage applies to bodily injury, property damage, or personal and advertising injury. |

| Performance Context | Coverage is applicable in connection with ongoing operations and premises owned or rented. |

| Contractual Limitations | Coverage for additional insureds is limited to what is required by contract or agreement. |

| Insurance Limits | The maximum payout for additional insureds is the lesser of contract limits or policy limits. |

| Legal Compliance | The endorsement only applies to the extent permitted by law. |

| Governing Law | This form is governed by the laws applicable to the state where the policy is issued. |

Filling out the CG 20 26 04 13 form is an important step in ensuring that the right individuals or organizations are covered under your commercial general liability insurance policy. Once you have completed the form, it will need to be submitted to your insurance provider for processing. Here’s how to fill it out correctly:

What is the purpose of the CG 20 26 04 13 form?

The CG 20 26 04 13 form is an endorsement to a Commercial General Liability (CGL) policy. Its primary purpose is to add designated persons or organizations as additional insureds. This means that these additional insured parties will have coverage under the policy for certain liabilities arising from the named insured's operations or premises. This endorsement modifies the existing insurance policy to extend protection to others, ensuring that they are covered for specific incidents related to the named insured's activities.

Who can be listed as an additional insured on this form?

The form allows for the inclusion of any person or organization specified in the Schedule section. Typically, these might include clients, contractors, or other parties that require additional coverage due to their relationship with the named insured. It is essential that the additional insureds are clearly identified in the policy declarations to ensure they receive the appropriate coverage.

What types of liabilities are covered for additional insureds?

Coverage for additional insureds under the CG 20 26 04 13 form includes liabilities for bodily injury, property damage, and personal and advertising injury. This coverage applies when these liabilities arise from the acts or omissions of the named insured or those acting on their behalf. The endorsement specifically covers incidents occurring during ongoing operations or in connection with premises owned or rented by the named insured.

Are there any limitations to the coverage provided?

Yes, there are limitations. The coverage for additional insureds is subject to the extent permitted by law. Additionally, if the coverage is required by a contract or agreement, it cannot exceed the level of insurance specified in that contract. Therefore, the protection afforded to additional insureds will not be broader than what the named insured is obligated to provide under any existing agreements.

How is the limit of insurance determined for additional insureds?

The limits of insurance for additional insureds are determined based on two factors: the amount required by the contract or agreement and the limits available under the CGL policy. The lesser of these two amounts will be the maximum that the insurer will pay on behalf of the additional insured. Importantly, this endorsement does not increase the overall limits of insurance stated in the policy declarations.

What should be done if there are changes to the additional insureds?

If there are changes to the additional insureds, it is crucial to update the Schedule section of the CG 20 26 04 13 form. This ensures that any new parties requiring coverage are properly documented and protected under the policy. Keeping this information current helps avoid potential gaps in coverage and ensures compliance with contractual obligations.

Filling out the CG 20 26 04 13 form can be straightforward, but several common mistakes can lead to complications. One frequent error is failing to include the policy number. This number is crucial for identifying the specific coverage and ensuring that the endorsement is properly attached to the right policy. Without it, the form may be considered incomplete.

Another mistake involves neglecting to accurately list the name of the additional insured. This section requires precise information. Any misspellings or incorrect titles can create issues when trying to enforce the coverage. It is essential to double-check the names against official documents to avoid any discrepancies.

People often overlook the importance of understanding the limits of insurance. The form includes specific language about the maximum amount payable to the additional insured. Failing to recognize these limits can lead to misunderstandings later on, especially if a claim arises. It is vital to read this section carefully to ensure compliance with contractual obligations.

In some cases, individuals may not fully grasp the implications of the contractual agreements mentioned in the form. If coverage for the additional insured is required by a contract, the insurance provided cannot exceed what is stipulated in that agreement. Ignoring this can result in inadequate coverage and potential liability issues.

Another common error is not providing sufficient detail regarding the scope of operations. The form specifies that the additional insured is covered only for liability arising from ongoing operations or premises owned or rented by the insured. Omitting details about these operations can lead to confusion and limit the effectiveness of the coverage.

Lastly, individuals sometimes fail to sign and date the form. A signature is necessary to validate the endorsement. Without it, the form may not be recognized as legitimate, which can cause significant delays in processing or claims.

By avoiding these mistakes, individuals can ensure that the CG 20 26 04 13 form is completed accurately and effectively, thereby safeguarding their interests and those of the additional insured.

The CG 20 26 04 13 form is an important document in the realm of commercial general liability insurance. It serves to add specific individuals or organizations as additional insured parties under a policy. However, there are other forms and documents that are frequently used alongside this endorsement to ensure comprehensive coverage and compliance with contractual obligations. Below is a list of such documents.

Understanding these documents is essential for businesses to navigate their insurance needs effectively. Each serves a unique purpose and collectively ensures that all parties involved are adequately protected against potential liabilities.

The CG 20 26 04 13 form is an endorsement that adds an additional insured to a commercial general liability policy. Several other documents share similar functions or purposes. Here are six such documents:

When filling out the CG 20 26 04 13 form, it is essential to follow specific guidelines to ensure accuracy and compliance. Here are four things you should and shouldn't do:

Understanding the CG 20 26 04 13 form is essential for anyone involved in commercial general liability insurance. However, several misconceptions often arise regarding its purpose and use. Here are ten common misconceptions clarified:

Being aware of these misconceptions can help you navigate the complexities of the CG 20 26 04 13 form more effectively. Always consult with an insurance professional for tailored advice regarding your specific situation.

Understanding the CG 20 26 04 13 form is essential for ensuring proper coverage under a Commercial General Liability policy. Here are key takeaways to consider: