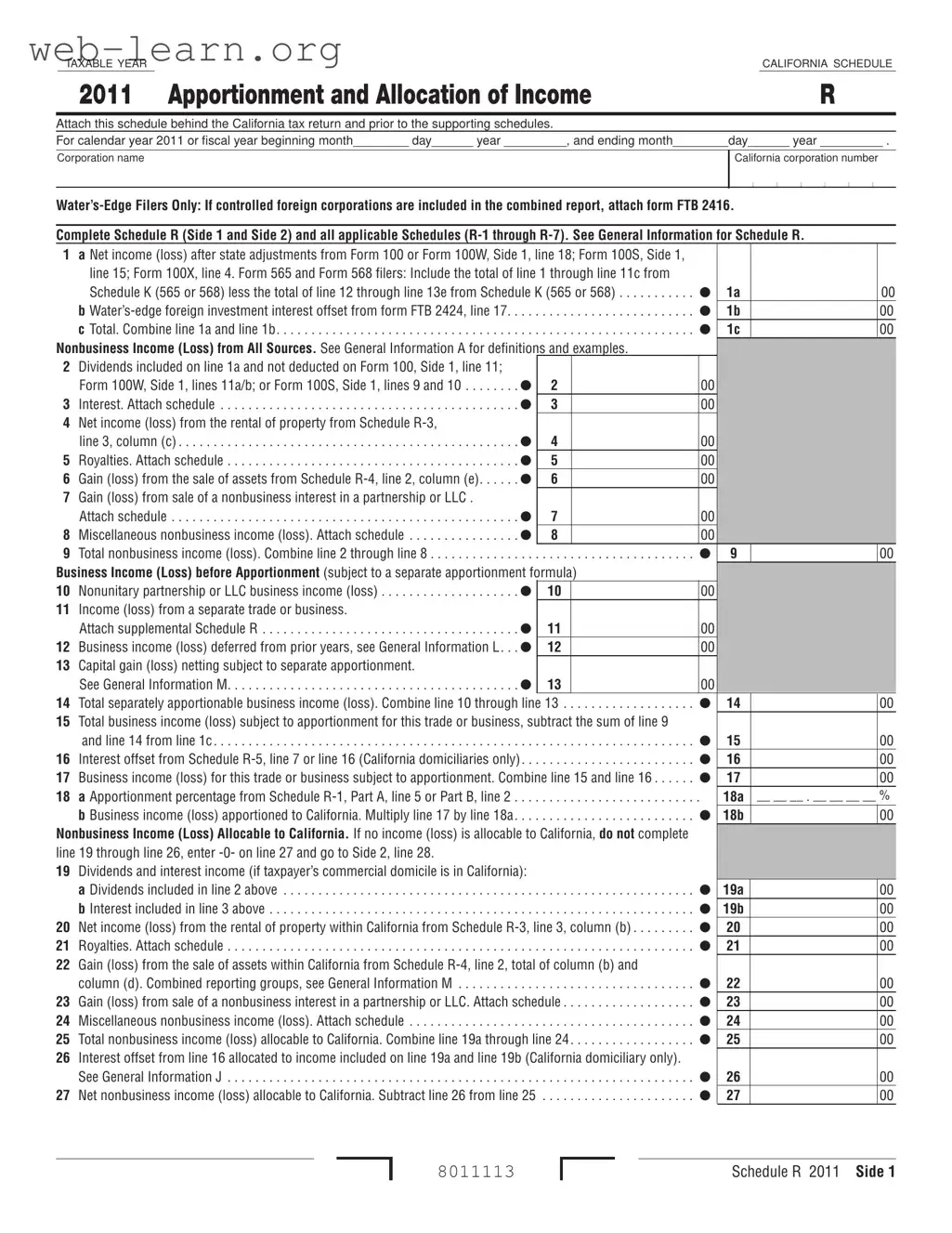

The California Schedule R form is an essential component for corporations operating within the state, particularly those engaged in multi-state activities. This form is designed to facilitate the apportionment and allocation of income, ensuring that businesses accurately report their income derived from California sources. It must be attached to the California tax return, specifically behind Form 100 or Form 100W, and is applicable for both calendar and fiscal years. Corporations must provide a comprehensive account of their net income or loss after state adjustments, incorporating various income sources such as dividends, interest, and rental income. Additionally, Schedule R includes provisions for reporting nonbusiness income and business income before apportionment, alongside detailed calculations for determining the appropriate apportionment percentage. For corporations electing the Water’s-Edge method, specific instructions regarding controlled foreign corporations must also be adhered to. Completing this form involves not only filling out the primary lines but also potentially attaching several supplementary schedules that delve deeper into the intricacies of income allocation and apportionment. Understanding the nuances of Schedule R is vital for compliance and for optimizing tax obligations in California.

| Fact Name | Description |

|---|---|

| Purpose of Schedule R | The California Schedule R is used for the apportionment and allocation of income for corporations. It must be attached to the California tax return to report business income and nonbusiness income accurately. |

| Applicable Forms | Corporations must refer to various forms when completing Schedule R, including Form 100, Form 100W, and Form 100S. Additionally, filers of Forms 565 and 568 should also include specific income calculations from their respective schedules. |

| Filing Requirements | Schedule R must be completed and submitted with the California tax return for the taxable year. It is critical to ensure that all relevant sections, including Schedules R-1 through R-7, are filled out as necessary. |

| Governing Law | The California Schedule R is governed by the California Revenue and Taxation Code, particularly sections related to corporate income taxation and apportionment rules. |

Completing the California Schedule R form involves several steps to ensure accurate reporting of income and apportionment. Follow these instructions carefully to fill out the form correctly.

The California Schedule R form is used by corporations to report the apportionment and allocation of income. It helps determine how much of a corporation's income is subject to California tax based on its business activities within and outside the state.

Corporations that conduct business in California and have income that needs to be apportioned or allocated must file Schedule R. This includes both California corporations and foreign corporations doing business in California.

Schedule R reports both business and nonbusiness income. Business income includes income from activities conducted in California, while nonbusiness income may include dividends, interest, and rental income from properties located in California.

The apportionment percentage is calculated using either a three-factor formula (property, payroll, and sales) or a single-sales factor formula. The corporation must choose one method and apply it consistently across reporting periods.

The Water’s-Edge election allows certain corporations to limit their reporting to income from U.S. sources, excluding foreign income. This can simplify tax reporting and potentially reduce tax liability for qualifying corporations.

Corporations must complete all applicable Schedules R-1 through R-7 alongside Schedule R. Each schedule addresses different aspects of income apportionment and allocation, ensuring comprehensive reporting.

Yes, a corporation can amend its Schedule R if it discovers errors or needs to adjust its reported income. This is typically done by filing an amended tax return with the corrected Schedule R attached.

Failure to file Schedule R can result in penalties, interest on unpaid taxes, and potential audits by the California Franchise Tax Board. It is crucial to file accurately and on time to avoid these issues.

Schedule R should be attached to the corporation's California tax return (Form 100, Form 100W, or Form 100S) and submitted to the California Franchise Tax Board as part of the overall tax filing process.

Filling out the California Schedule R form can be challenging, and mistakes can lead to delays or inaccuracies in tax filings. Here are five common errors to avoid.

One frequent mistake is failing to include all necessary schedules. Schedule R requires the completion of additional Schedules R-1 through R-7. Omitting any of these can result in incomplete information, which may trigger requests for further documentation or corrections from the tax authority.

Another common error involves miscalculating income figures. Taxpayers sometimes confuse net income with gross income or fail to accurately report nonbusiness income. It is essential to ensure that all figures align with the corresponding lines on the main tax return and any applicable schedules. Double-checking these numbers can prevent discrepancies.

Many people also overlook the apportionment percentage. This percentage is crucial for determining how much income is taxable in California. If the apportionment percentage is incorrectly calculated or not reported at all, it can lead to significant errors in tax liability. Make sure to follow the guidelines for calculating this percentage carefully.

Additionally, inconsistent reporting across different tax years can create complications. Taxpayers should maintain consistency in how they report income and deductions from year to year. Any changes in reporting methods should be clearly explained in the form to avoid confusion.

Lastly, neglecting to review the General Information section can lead to misunderstandings of specific requirements or definitions. This section provides vital context and instructions that can help clarify what is needed for accurate reporting. Taking the time to read this information can save headaches later on.

The California Schedule R form is an essential document for corporations filing their taxes in California, particularly for those with complex income streams. Alongside this form, several other documents are often required to ensure accurate reporting and compliance with state tax regulations. Below is a list of commonly associated forms that help clarify various aspects of a corporation's financial activities.

Each of these forms plays a crucial role in the overall tax reporting process for California corporations. Together, they provide a comprehensive view of a corporation's financial activities, ensuring compliance and facilitating accurate tax calculations.

The California Schedule R form is a critical document for corporations filing taxes in California. It focuses on the apportionment and allocation of income. Several other forms share similarities with Schedule R in terms of purpose and content. Below is a list of documents that are comparable to the California Schedule R form:

Each of these forms plays a role in the overall process of reporting and allocating income for tax purposes in California, similar to the function of the California Schedule R form.

When filling out the California Schedule R form, there are important dos and don'ts to keep in mind. Here’s a straightforward list to guide you:

This form is applicable to various types of corporations, including smaller businesses that need to report their apportionment and allocation of income in California.

For corporations that are required to apportion income, completing Schedule R is mandatory. It must be attached to the California tax return.

Each tax year may have specific requirements or changes in the form. It’s important to use the correct version of Schedule R for the applicable tax year.

Nonbusiness income must be reported on Schedule R, as it can affect the overall tax liability of the corporation.

Schedule R requires reporting both California and non-California income, as the apportionment process considers the total income from all sources.

The apportionment percentage can vary based on various factors, including the business activities and the location of sales, property, and payroll.

Corporations can amend their Schedule R if they discover errors or need to make adjustments. However, it’s essential to follow the proper procedures for amendments.

Understand the Purpose: The California Schedule R form is essential for corporations to report their apportionment and allocation of income. It helps determine how much income is taxable in California versus other states.

Complete All Sections: Ensure that both sides of Schedule R are filled out completely. This includes reporting net income, nonbusiness income, and any applicable schedules (R-1 through R-7) that provide further details.

Follow Instructions Carefully: Pay close attention to the instructions provided in the General Information section. Each line has specific requirements, and missing information can lead to delays or errors in processing your tax return.

Attach Necessary Forms: If your corporation includes controlled foreign corporations in its combined report, remember to attach form FTB 2416. Additionally, any schedules related to nonbusiness income or specific deductions should also be included.