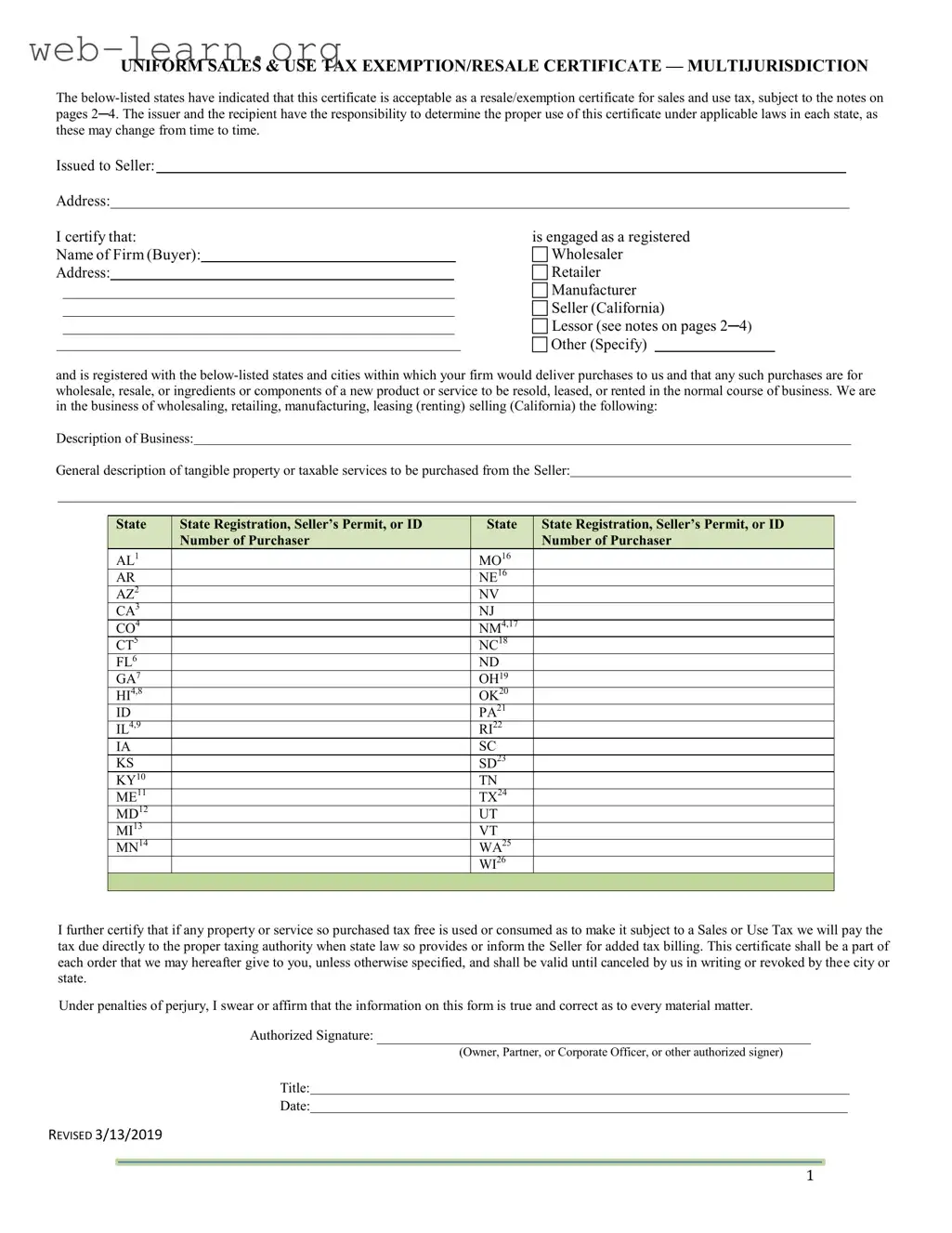

The California Sales Tax Certificate form, officially known as the Uniform Sales & Use Tax Exemption/Resale Certificate, serves as a crucial document for businesses engaged in the buying and selling of goods and services. This form allows purchasers to claim exemption from sales tax on items intended for resale, thereby streamlining the transaction process between buyers and sellers. It is essential that both the issuer and the recipient understand their responsibilities regarding the proper use of this certificate, as misuse can lead to significant tax liabilities. The form requires the buyer to provide their business name, address, and registration details, while also certifying that the purchases are meant for wholesale, resale, or as components in new products. Additionally, it outlines specific instructions and requirements for various states, emphasizing that the certificate must be retained by the seller to validate tax-exempt sales. Buyers must also be aware that if any exempt property is ultimately used or consumed in a manner that triggers sales tax, they are responsible for remitting that tax directly to the appropriate taxing authority. This certificate remains valid until revoked, ensuring that businesses maintain compliance with evolving tax regulations across multiple jurisdictions.

| Fact Name | Details |

|---|---|

| Purpose | This certificate is used to document that the Buyer is purchasing goods for resale, allowing them to avoid paying sales tax. |

| Validity in California | In California, this certificate is valid only as a resale certificate, not as an exemption certificate, under Title 18, California Code of Regulations, Section 1668. |

| Responsibility | Both the issuer and the recipient must ensure the proper use of this certificate, as laws may change over time. |

| Signature Requirement | The certificate must be signed by an authorized person, such as an owner or corporate officer, to be valid. |

| Expiration | This certificate remains valid until it is canceled in writing by the issuer or revoked by the state. |

| Consequences of Misuse | Improper use of the certificate can lead to penalties, including fines or imprisonment, depending on state laws. |

Filling out the California Sales Tax Certificate form requires careful attention to detail. This process ensures that the buyer can purchase goods without paying sales tax, provided they are for resale. The following steps will guide you through the completion of the form.

Once you have completed the form, submit it to the seller. They will retain it for their records, ensuring compliance with state tax laws. This certificate will remain valid until you cancel it in writing or the issuing authority revokes it.

If you are purchasing goods for resale, you should provide this certificate to your vendor. This will ensure that your vendor does not charge you sales tax on your purchase. Conversely, if you are a seller who has received this certificate from your buyer, you must keep the certificate on file for your records.

Yes, you can register for multiple states at the same time. For more details, visit www.sstregister.org. This resource provides guidance on how to navigate the registration process across various states.

After receiving the certificate from your customer, review it carefully. If you accept it in good faith, keep it on file as required by state laws. Generally, the relevant state will be where you are located or where the sales transaction occurred.

Your role depends on the transaction. If you are purchasing goods for resale, you are the Buyer. If you are selling goods to someone who intends to resell them, you are the Seller.

The primary purpose of this certificate is to serve as documentation that the Seller should not collect sales tax. This applies when the goods or services sold, or the Buyer, are exempt from sales tax.

The Buyer is responsible for completing the certificate. Fill in the "Issued to Seller" and "Name of Firm (Buyer)" sections, along with the necessary details about your business and the nature of the purchase.

Next to each state abbreviation, you should provide your state registration number, Seller’s Permit, or ID number as required by that state. This information is crucial for the validity of the certificate.

If you do not have an ID number for certain states, it is advisable to consult with a tax professional or the state’s tax authority for guidance. Each state has specific requirements, and it is important to comply with them.

This certificate should be used by businesses that are purchasing goods or services for resale. It is essential for both Buyers and Sellers to understand its proper use to avoid potential tax liabilities.

Filling out the California Sales Tax Certificate form can seem straightforward, but there are common mistakes that can lead to complications down the line. One significant error is leaving out critical information. Buyers often forget to provide their name, address, or the business type. Each of these details is essential for verifying the legitimacy of the claim. Omitting any of this information can result in the seller being required to collect sales tax, which defeats the purpose of the certificate.

Another frequent mistake is failing to specify the reason for exemption. The form allows for multiple business types, such as wholesaler or retailer, and not indicating which one applies can create confusion. Sellers need this information to ensure they comply with tax regulations. If the exemption reason isn’t clearly marked, the certificate may be rejected, leading to unnecessary tax charges.

Many buyers also neglect to include their state registration or seller’s permit number. This number is crucial as it verifies that the buyer is authorized to make tax-exempt purchases. Without it, the seller may not accept the certificate, and the buyer could end up paying sales tax unnecessarily. This step is often overlooked, but it is vital for maintaining compliance.

Additionally, buyers sometimes forget to sign the certificate. A signature is not just a formality; it affirms that the information provided is accurate and true. Without a signature, the certificate is incomplete and may not be honored by the seller. This can lead to complications and additional costs for the buyer.

Lastly, many individuals mistakenly believe that this certificate is a one-time document. In reality, it should be updated regularly, especially if any of the business details change. Keeping the certificate current is essential to avoid any issues with tax authorities. Ignoring this can lead to penalties or audits, which can be both time-consuming and costly.

The California Sales Tax Certificate is a crucial document for businesses engaged in the resale of goods. It serves to exempt buyers from paying sales tax on items purchased for resale. Several other forms and documents complement this certificate, ensuring compliance with tax regulations and proper record-keeping. Below is a list of commonly used documents alongside the California Sales Tax Certificate.

Understanding these documents and their purposes can facilitate smoother transactions and ensure compliance with California tax laws. Proper documentation not only protects businesses from potential tax liabilities but also supports the integrity of the resale process.

The California Sales Tax Certificate form shares similarities with several other documents used in various states for tax exemption purposes. Below is a list of seven documents that are comparable, along with their specific similarities:

When filling out the California Sales Tax Certificate form, it's important to be thorough and accurate. Here are some key dos and don'ts to keep in mind:

This is incorrect. The certificate is strictly a resale certificate and cannot be used to claim an exemption from sales tax.

This is not true. The certificate is only valid for purchases intended for resale or as ingredients in products for resale.

The certificate remains valid until canceled in writing by the issuer or revoked by the state. Regular updates are recommended.

Sellers must exercise due diligence to ensure the certificate is valid and applicable to the transaction. Failure to do so could lead to tax liability.

This is misleading. Some states have specific regulations regarding the use of this certificate, and it may not be accepted for certain types of purchases.

This is false. The certificate is only for business transactions involving resale or manufacturing.

Sellers are obligated to take the certificate seriously. Ignoring it can lead to penalties and tax liabilities.

This is incorrect. The certificate must be properly filled out and signed to be valid.

This is not the case. Sellers must keep the certificate on file and may need to provide it during audits or inquiries.

Understand the Purpose: The California Sales Tax Certificate is primarily used to certify that a purchase is intended for resale. This means that if you are buying goods to sell them, you should provide this certificate to the seller to avoid being charged sales tax.

Complete the Certificate Accurately: When filling out the form, ensure that all required fields are completed accurately. This includes your business name, address, and the nature of your business. Any errors or omissions can lead to complications down the line.

Keep Records: Once you provide this certificate to a seller, it is important for both parties to keep a copy on file. Sellers must retain these certificates as proof of the exemption, and buyers should also keep a record for their own accounting purposes.

Be Aware of State-Specific Rules: Different states have varying regulations regarding sales tax exemptions. While this certificate is valid in California, it may not apply in the same way in other states. Always check local laws to ensure compliance.