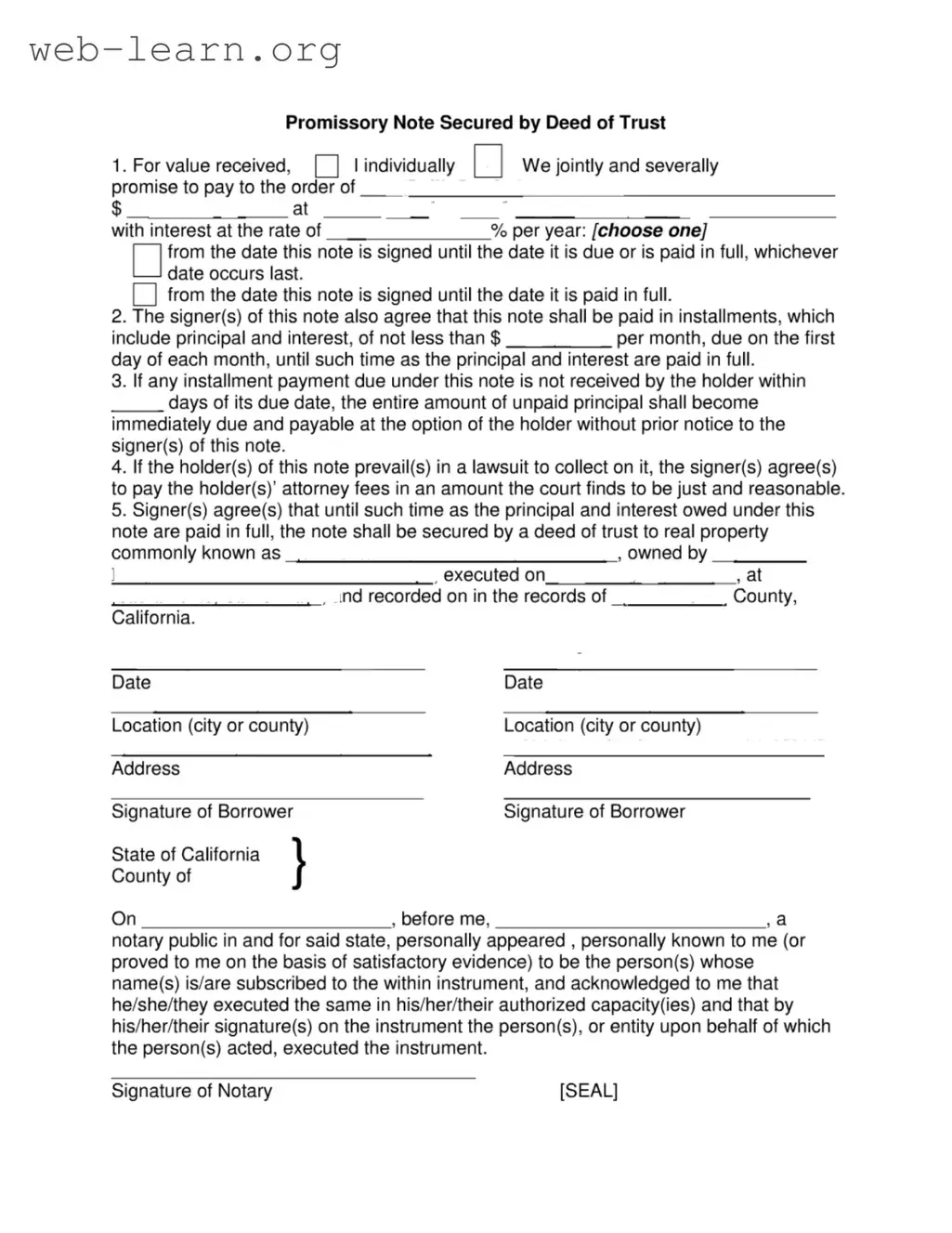

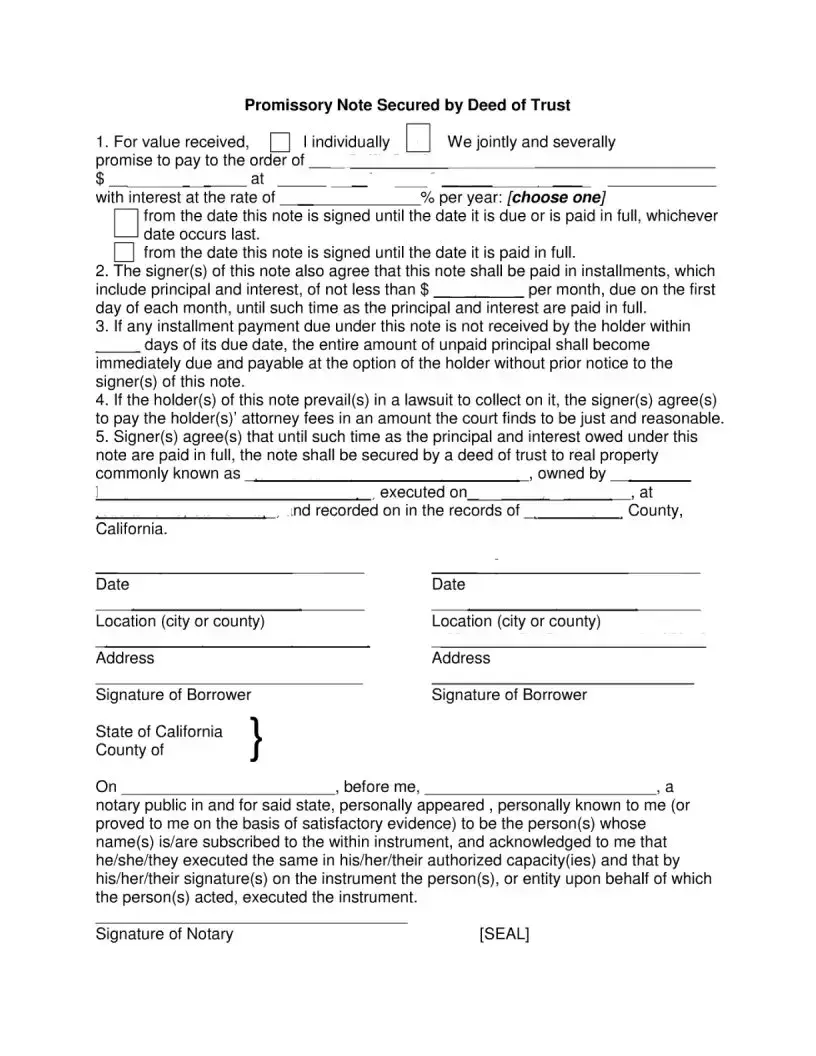

The California Note Secured form is a crucial document for individuals entering into a promissory note backed by a deed of trust. This form outlines the borrower's commitment to repay a specified amount of money, detailing the interest rate and payment structure. Borrowers agree to make monthly payments that cover both principal and interest, ensuring that the loan is paid off over time. Should any payment be missed, the lender has the right to demand the full outstanding balance immediately, without prior notice. Additionally, if the lender must resort to legal action to collect the debt, the borrower is responsible for covering the lender's attorney fees. Importantly, the note is secured by a deed of trust to a specific piece of real property, providing the lender with a safeguard in case of default. This combination of terms creates a clear framework for both parties, promoting accountability and transparency in the lending process.

| Fact Name | Details |

|---|---|

| Purpose | This form serves as a Promissory Note that is secured by a Deed of Trust, ensuring that the lender has a claim on the property if the borrower defaults. |

| Payment Structure | Borrowers agree to pay the loan in installments, which include both principal and interest, with payments due monthly. |

| Interest Rate | The interest rate is determined by the borrower and lender at the time the note is signed, allowing for flexibility in terms. |

| Late Payment Consequences | If an installment is not received within a specified number of days after its due date, the entire unpaid principal may become due immediately. |

| Attorney Fees | Should the lender need to pursue legal action to collect on the note, the borrower agrees to cover reasonable attorney fees as determined by the court. |

| Secured by Real Property | The note is secured by a Deed of Trust to a specific piece of real property, providing additional security for the lender. |

| Governing Law | This form is governed by California law, specifically the California Civil Code sections related to promissory notes and deeds of trust. |

| Notary Requirement | The signatures of the borrowers must be notarized, ensuring the authenticity of the document and the identities of the signers. |

Filling out the California Note Secured form requires careful attention to detail. This form serves as a legal document outlining the terms of a promissory note secured by a deed of trust. Once completed, it must be signed and notarized to ensure its validity.

The California Note Secured form is a legal document that outlines a promissory note secured by a deed of trust. This form is typically used when a borrower agrees to repay a loan with interest over a specified period. The note details the amount borrowed, the interest rate, and the repayment schedule. It also includes provisions for what happens if payments are missed, including the possibility of the entire loan amount becoming due immediately.

The form contains several important elements:

If a payment is missed, the lender has the right to declare the entire unpaid principal amount due immediately. This means that the borrower may need to pay off the entire loan balance rather than just the missed installment. The specific timeframe for how long the lender will wait before taking this action is typically outlined in the form. It is crucial for borrowers to understand this provision and communicate with their lender if they anticipate difficulty making a payment.

The deed of trust serves as security for the loan. Essentially, it gives the lender a legal claim to the property if the borrower defaults on the loan. This means that if the borrower fails to repay the loan as agreed, the lender can initiate foreclosure proceedings to recover the owed amount by selling the property. The deed of trust is recorded in the county where the property is located, ensuring that the lender's interest in the property is legally recognized.

Completing the California Note Secured form requires careful attention to detail. One common mistake individuals make is leaving the amount owed blank. This figure is crucial as it specifies the total sum that the borrower agrees to repay. Without this information, the note lacks clarity and can lead to disputes later on. Ensure that this amount is filled in accurately to avoid complications.

Another frequent error involves the interest rate. Borrowers sometimes forget to specify the rate or select an inappropriate one. This omission can create confusion regarding the total cost of the loan over time. It is essential to clearly state the interest rate to provide transparency and to comply with legal requirements.

Additionally, many people overlook the section regarding installment payments. Failing to indicate the minimum monthly payment can result in misunderstandings about the payment structure. It is vital to specify not only the amount but also the due date to ensure that both parties are on the same page regarding repayment expectations.

Another mistake involves the security details of the note. When identifying the property secured by the deed of trust, individuals may neglect to provide complete and accurate information. This includes the property’s address and details about its ownership. Incomplete information can complicate the enforcement of the note if issues arise.

Finally, the notary section is often filled out incorrectly. Borrowers may forget to include the notary's signature or seal, which is essential for the document's validity. Ensuring that this section is properly completed adds an important layer of legal protection for both the borrower and the lender.

The California Note Secured form is an essential document in real estate transactions, particularly when a borrower takes out a loan secured by a property. Along with this form, several other documents often accompany it to ensure clarity and legal protection for all parties involved. Below is a list of these documents, each with a brief description.

These documents work together to create a clear framework for the loan agreement, ensuring that all parties understand their rights and obligations. By having these forms in place, both borrowers and lenders can navigate the complexities of real estate financing with greater confidence.

The California Note Secured form shares similarities with several other financial documents. Each of these documents serves a purpose related to loans, security interests, or payment obligations. Here’s a list of nine documents that are similar:

When filling out the California Note Secured form, it’s important to follow certain guidelines to ensure accuracy and legality. Here are six things to keep in mind:

By following these guidelines, you can help ensure that the California Note Secured form is completed correctly and is legally binding. If you have any questions, consider seeking assistance from a qualified professional.

This form can be used for any amount of money. It is not limited to large loans, making it accessible for various financial situations.

While the terms are binding once signed, parties can negotiate modifications later. Changes must be documented properly to be enforceable.

The lender can only demand full payment if the borrower misses a payment. This is outlined in the agreement, which protects the borrower from sudden demands.

Borrowers have rights in legal proceedings. They can present their case, and the court will consider both sides before making a decision.

The deed of trust secures the loan with real property. If the borrower defaults, the lender can take action against the property, making it a significant aspect of the agreement.

Here are some key takeaways for filling out and using the California Note Secured form: