In California, the Deed in Lieu of Foreclosure form serves as a vital tool for homeowners facing financial distress. This legal document allows property owners to voluntarily transfer ownership of their home back to the lender, effectively avoiding the lengthy and often stressful foreclosure process. By opting for this route, homeowners can mitigate the impact on their credit scores and potentially negotiate terms that benefit both parties. The form outlines essential details such as the property description, the parties involved, and any outstanding obligations. It can also include provisions for the release of liability on the mortgage, providing peace of mind to the homeowner. Understanding the implications and requirements of this form is crucial for anyone considering it as a solution to their financial challenges. With the right information, homeowners can navigate this process more effectively and make informed decisions about their future.

California Deed in Lieu of Foreclosure Template

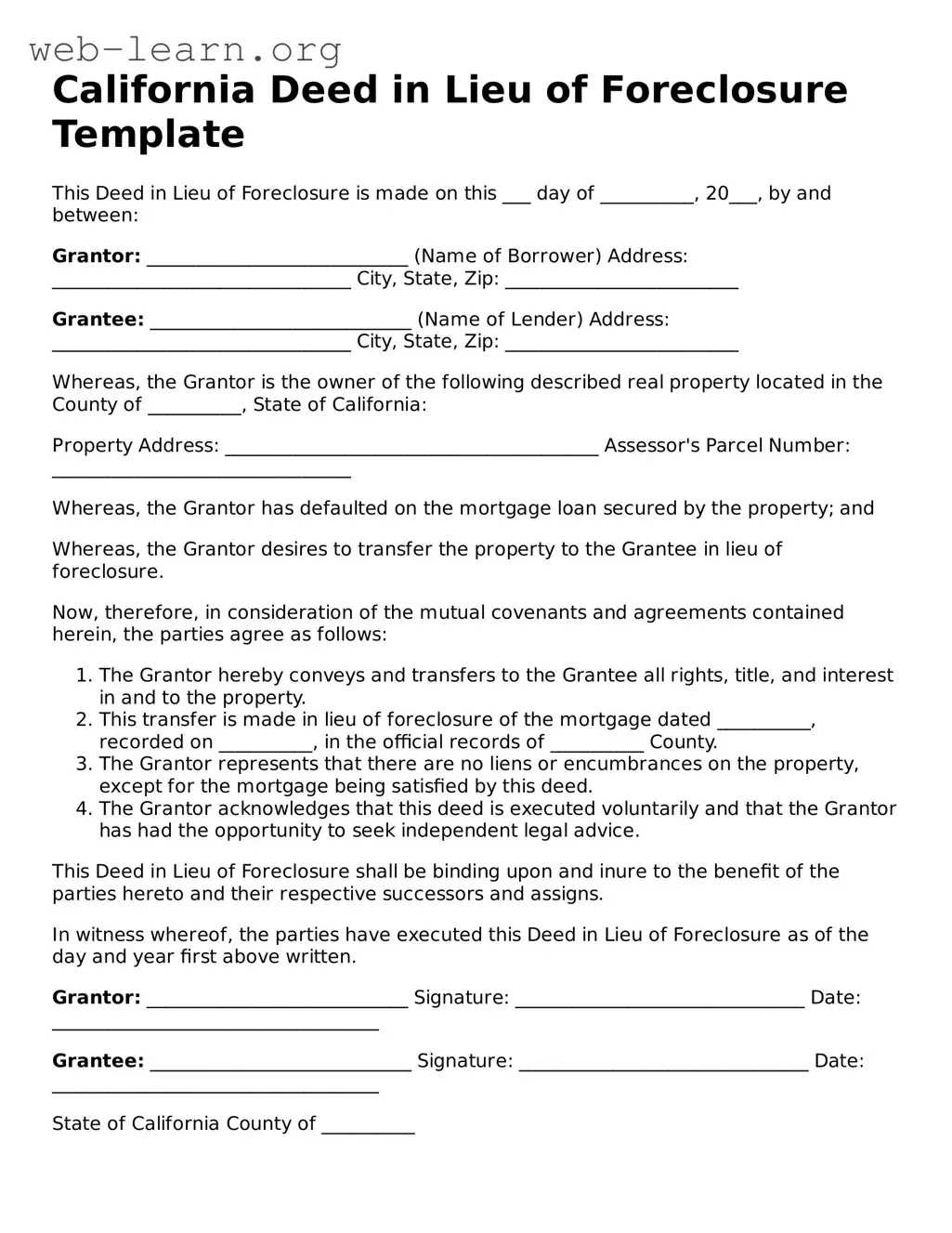

This Deed in Lieu of Foreclosure is made on this ___ day of __________, 20___, by and between:

Grantor: ____________________________ (Name of Borrower) Address: ________________________________ City, State, Zip: _________________________

Grantee: ____________________________ (Name of Lender) Address: ________________________________ City, State, Zip: _________________________

Whereas, the Grantor is the owner of the following described real property located in the County of __________, State of California:

Property Address: ________________________________________ Assessor's Parcel Number: ________________________________

Whereas, the Grantor has defaulted on the mortgage loan secured by the property; and

Whereas, the Grantor desires to transfer the property to the Grantee in lieu of foreclosure.

Now, therefore, in consideration of the mutual covenants and agreements contained herein, the parties agree as follows:

This Deed in Lieu of Foreclosure shall be binding upon and inure to the benefit of the parties hereto and their respective successors and assigns.

In witness whereof, the parties have executed this Deed in Lieu of Foreclosure as of the day and year first above written.

Grantor: ____________________________ Signature: _______________________________ Date: ___________________________________

Grantee: ____________________________ Signature: _______________________________ Date: ___________________________________

State of California County of __________

On this ___ day of __________, 20___, before me, a Notary Public, personally appeared ____________________________ (Grantor's Name), who proved to me on the basis of satisfactory evidence to be the person whose name is subscribed to this instrument and acknowledged that he/she executed it.

Notary Public Signature: _______________________ My Commission Expires: _______________________

| Fact Name | Description |

|---|---|

| Definition | A deed in lieu of foreclosure is a legal document where a borrower voluntarily transfers the title of their property to the lender to avoid foreclosure. |

| Governing Law | The process is governed by California Civil Code Section 1475 et seq., which outlines the requirements and implications of such deeds. |

| Benefits | This option can help borrowers avoid the lengthy foreclosure process, preserve their credit score, and eliminate the burden of an underwater mortgage. |

| Eligibility | Typically, borrowers must demonstrate financial hardship and be unable to keep up with mortgage payments to qualify for this option. |

| Impact on Credit | While a deed in lieu of foreclosure is less damaging than a foreclosure, it may still negatively affect the borrower's credit score. |

After completing the California Deed in Lieu of Foreclosure form, you’ll be ready to move forward with the next steps in your process. This may involve submitting the form to your lender and ensuring that all necessary parties are informed. It's essential to keep copies of everything for your records.

What is a Deed in Lieu of Foreclosure?

A Deed in Lieu of Foreclosure is a legal agreement where a homeowner voluntarily transfers the ownership of their property to the lender to avoid foreclosure. This process allows the homeowner to walk away from the mortgage without the damaging consequences of foreclosure on their credit report. It can be a beneficial option for those who are struggling to keep up with mortgage payments.

How does the process work?

The process typically begins when a homeowner contacts their lender to discuss their financial difficulties. If both parties agree to pursue a Deed in Lieu of Foreclosure, the homeowner will need to provide documentation of their financial situation. This may include income statements, tax returns, and information about other debts. Once the lender reviews the information and approves the request, the homeowner signs the deed, transferring ownership of the property to the lender.

What are the benefits of a Deed in Lieu of Foreclosure?

There are several advantages to consider:

These benefits make it an appealing option for many facing financial hardship.

Are there any drawbacks?

While a Deed in Lieu of Foreclosure has its benefits, it is important to consider potential drawbacks:

Can I still buy another home after a Deed in Lieu of Foreclosure?

Yes, it is possible to buy another home after a Deed in Lieu of Foreclosure, but it may take time. Most lenders require a waiting period before considering a new mortgage application. This period can vary, but it often ranges from two to four years. During this time, rebuilding your credit and improving your financial situation will be crucial for future home-buying opportunities.

Filling out the California Deed in Lieu of Foreclosure form can be a complex process, and many individuals make critical mistakes that can jeopardize their intentions. One common error is failing to provide accurate property information. When the address or legal description of the property is incorrect, it can lead to delays or even rejection of the deed. Always double-check these details to ensure they match official records.

Another frequent mistake is neglecting to include all necessary signatures. The form requires signatures from all parties involved, including co-owners or spouses. Omitting a signature can invalidate the deed, causing complications down the line. It is essential to ensure that everyone with an interest in the property has signed the document.

Many people also overlook the importance of understanding the implications of signing the deed. A deed in lieu of foreclosure can have significant consequences on one's credit and future borrowing ability. Failing to grasp these implications can lead to regret after the fact. It is advisable to consult with a legal or financial expert before proceeding.

Additionally, individuals often forget to attach supporting documents. The form may require additional paperwork, such as a statement of the mortgage balance or proof of hardship. Not including these documents can slow the process and create unnecessary hurdles. Always check the requirements carefully before submission.

Another common pitfall is not properly notifying the lender. While the deed in lieu is a voluntary action, lenders typically need formal notice. Some people assume that submitting the deed is enough, but failing to communicate with the lender can lead to misunderstandings and potential legal issues.

People sometimes also underestimate the need for a notary. The deed must be notarized to be legally binding. Skipping this step can render the document ineffective. Ensure that you have a notary available when finalizing the deed to avoid this mistake.

Finally, individuals may not fully understand the tax implications of a deed in lieu of foreclosure. The cancellation of debt can result in tax liability, which can come as an unpleasant surprise. Consulting with a tax professional can provide clarity on potential tax consequences and help in planning accordingly.

A Deed in Lieu of Foreclosure can be a helpful tool for homeowners facing financial difficulties. It allows a homeowner to voluntarily transfer their property to the lender, thereby avoiding the lengthy foreclosure process. When completing this transaction, several other forms and documents may also be required. Below is a list of these important documents.

Understanding these documents can ease the process for homeowners and lenders alike. Being prepared with the necessary paperwork can help ensure a smoother transition and provide clarity during a challenging time.

When filling out the California Deed in Lieu of Foreclosure form, it is essential to approach the process with care. Here are some key dos and don'ts to keep in mind:

Taking these steps can help protect your interests and ensure a smoother transition during a challenging time.

Many homeowners facing financial difficulties may consider a Deed in Lieu of Foreclosure as an option. However, several misconceptions surround this process. Here are four common misunderstandings:

While a Deed in Lieu of Foreclosure can help homeowners avoid foreclosure, it does not necessarily erase all debts associated with the property. Homeowners may still be responsible for any remaining mortgage balance or other liens on the property.

The process can be lengthy and complicated. Lenders often require extensive documentation and may take time to approve the deed. Homeowners should be prepared for a potentially drawn-out process.

A Deed in Lieu of Foreclosure can negatively affect a homeowner's credit score. Although it may be less damaging than a foreclosure, it still represents a significant negative mark on a credit report.

Not all lenders are willing to accept a Deed in Lieu of Foreclosure. Some may prefer to proceed with foreclosure instead. Homeowners should check with their lender to understand their specific policies.

Filling out and using the California Deed in Lieu of Foreclosure form is a significant step for homeowners facing foreclosure. Here are key takeaways to consider:

Taking these steps seriously can help streamline the process and minimize complications. Act promptly to protect your interests.

What Does an Arizona Homeowner Lose When Choosing to Use Deed in Lieu of Foreclosure? - The lender will review the homeowner's financial status before accepting the deed.

Foreclosure Georgia - The process can lead to a quicker resolution of housing issues.

A Deed in Lieu of Foreclosure - This form can serve as a practical solution for those facing unavoidable financial challenges.

Sample Deed in Lieu of Foreclosure - It may be necessary to negotiate a release from liability for any remaining mortgage debt.