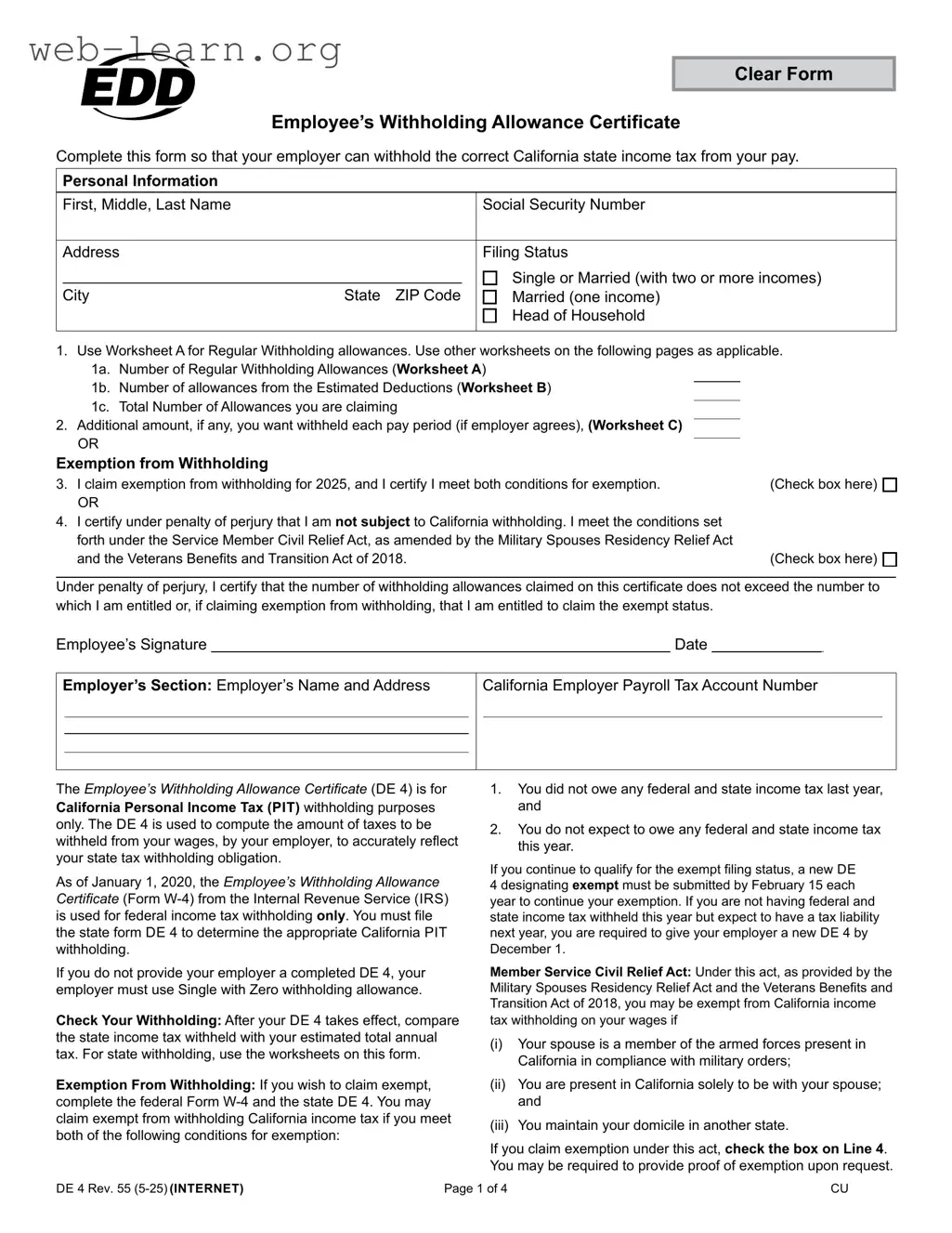

The California DE 4 form, officially known as the Employee’s Withholding Allowance Certificate, plays a crucial role in determining how much state income tax is withheld from an employee's paycheck. This form is essential for ensuring that the correct amount of California Personal Income Tax (PIT) is deducted based on individual circumstances. When filling out the DE 4, employees provide personal information such as their name, address, and Social Security number, and they must select their filing status—options include single, married, or head of household. The form also includes worksheets that guide users in calculating their withholding allowances, which can vary based on factors like dependents, itemized deductions, and multiple income sources. Additionally, individuals have the option to claim exemption from withholding if they meet specific criteria, such as not owing any federal or state income tax in the previous year and not expecting to owe taxes in the current year. Furthermore, the DE 4 outlines the importance of reviewing withholding amounts regularly to ensure they align with estimated tax liabilities. By accurately completing this form, employees can avoid under-withholding, which could lead to penalties and unexpected tax bills at the end of the year.

| Fact Name | Description |

|---|---|

| Purpose of DE 4 | The DE 4 form is used to determine the correct amount of California state income tax that should be withheld from an employee's paycheck. |

| Filing Requirements | Employees must submit the DE 4 to their employer to ensure proper withholding. If not submitted, the employer will withhold taxes as if the employee is single with zero allowances. |

| Exemption Conditions | To claim exemption from withholding, employees must meet two conditions: they did not owe any federal or state income tax last year and do not expect to owe any this year. |

| Legal Authority | The DE 4 is governed by the California Revenue and Taxation Code, specifically sections 18624 and 19176, as well as Title 22 of the California Code of Regulations. |

| Penalties for Incorrect Filing | Filing a DE 4 with no reasonable basis that results in less tax being withheld may lead to a fine of $500. Criminal penalties may also apply for providing false information. |

Filling out the California DE 4 form is an important step to ensure the correct amount of state income tax is withheld from your paycheck. Follow these steps carefully to complete the form accurately.

What is the purpose of the California DE 4 form?

The California DE 4 form, also known as the Employee’s Withholding Allowance Certificate, is used to determine the correct amount of state income tax to withhold from your paycheck. By completing this form, you help your employer calculate how much tax to withhold based on your personal circumstances.

Who needs to fill out the DE 4 form?

Any employee in California who wants their employer to withhold the correct amount of state income tax should complete the DE 4 form. This includes individuals who are starting a new job, experiencing a change in their financial situation, or simply want to adjust their withholding allowances.

How do I determine the number of withholding allowances to claim?

You can determine the number of allowances by using Worksheet A included with the DE 4 form. Consider factors such as whether you have dependents, if you are blind, or if you plan to itemize deductions. The total number of allowances claimed should reflect your unique financial situation.

What if I want to claim exemption from withholding?

If you believe you qualify for exemption from withholding, you must meet two conditions: you did not owe any federal or state income tax last year, and you do not expect to owe any this year. To claim this status, check the appropriate box on the DE 4 form. Remember, this exemption is valid for one year and must be renewed annually.

What should I do if I have multiple jobs?

If you work multiple jobs, it is advisable to claim all your allowances on the DE 4 form for your highest-paying job. This approach minimizes the risk of under-withholding. Do not claim the same allowances with more than one employer, as it can lead to tax complications later.

What happens if I do not submit a DE 4 form?

If you do not provide your employer with a DE 4 form, they will automatically withhold taxes as if you are single with zero allowances. This may result in more tax being withheld than necessary, which could affect your take-home pay.

Can I change my withholding allowances later?

Yes, you can update your withholding allowances at any time by submitting a new DE 4 form to your employer. This is particularly useful if your personal or financial situation changes, such as getting married, having a child, or experiencing a significant change in income.

What penalties could I face for incorrect information on the DE 4?

Providing false information on the DE 4 can lead to penalties. You may be fined $500 if you file a DE 4 that results in less tax being withheld than is properly allowable. Additionally, criminal penalties may apply for willfully supplying false information. It is essential to ensure that all information provided is accurate and truthful.

Filling out the California DE 4 form correctly is essential for ensuring accurate state income tax withholding. However, many individuals make common mistakes that can lead to complications. One frequent error is failing to provide complete personal information. This includes not entering the full name, Social Security number, or address. Incomplete information can delay processing and lead to incorrect withholding.

Another mistake involves misunderstanding filing status. Selecting the wrong filing status can significantly impact the number of allowances claimed. For example, individuals may mistakenly choose "Single" when they are actually "Married" or "Head of Household." It is crucial to review the definitions of each status before making a selection.

Many individuals also overlook the use of the worksheets provided with the DE 4 form. These worksheets are designed to help determine the correct number of allowances. Failing to utilize Worksheet A or B can result in under- or over-withholding, which may lead to unexpected tax liabilities at the end of the year.

Claiming allowances incorrectly is another common issue. Some people claim allowances for dependents or other factors that do not apply to their situation. This can lead to inaccurate withholding amounts. It is important to ensure that only valid allowances are claimed based on individual circumstances.

Additionally, individuals sometimes forget to sign and date the form. A missing signature can render the form invalid, causing the employer to withhold taxes at the highest rate. Always double-check that the form is signed and dated before submission.

Another mistake is not updating the DE 4 form when personal circumstances change. Events such as marriage, divorce, or the birth of a child can affect withholding allowances. It is important to submit a new DE 4 form whenever significant life changes occur to ensure that withholding remains accurate.

Lastly, some individuals mistakenly believe they are exempt from withholding without meeting the necessary criteria. To claim exemption, one must not have owed any federal or state income tax in the previous year and not expect to owe in the current year. Failing to meet these conditions can lead to penalties and unexpected tax bills.

The California DE 4 form is essential for employees to determine the correct amount of state income tax withheld from their paychecks. However, several other forms and documents are often used in conjunction with the DE 4 to ensure accurate tax reporting and withholding. Below is a list of commonly associated documents.

These documents work together to facilitate accurate tax withholding and reporting for employees and employers alike. Understanding each form's purpose can lead to better financial planning and compliance with state tax laws.

When filling out the California DE 4 form, it’s important to approach the process with care. Here are some key do's and don'ts to keep in mind:

This form is not optional. Employees must complete it to ensure the correct amount of state income tax is withheld from their paychecks.

In reality, the DE 4 is designed for all filing statuses, including married individuals and heads of household.

Filing the DE 4 does not guarantee a refund. It only helps in determining the correct withholding amount to avoid underpayment or overpayment of taxes.

There are limits to the number of allowances an employee can claim based on their personal situation and tax obligations.

While both forms serve a similar purpose, they are distinct. The DE 4 is specifically for California state income tax withholding.

Employers are not required to withhold the additional amount requested unless they agree to do so.

Employees should update their DE 4 whenever their financial situation changes, such as marriage, divorce, or a change in income.

There are deadlines for submitting the DE 4 to ensure correct withholding for the tax year, particularly for those claiming exemption from withholding.

Claiming exemption only applies if the employee meets specific criteria. If their situation changes, they may owe taxes.

The DE 4 impacts every paycheck throughout the year, making it crucial to complete it accurately at any time.

Filling out the California DE 4 form is essential for ensuring the correct amount of state income tax is withheld from your paycheck. Here are some key takeaways to help you navigate the process: