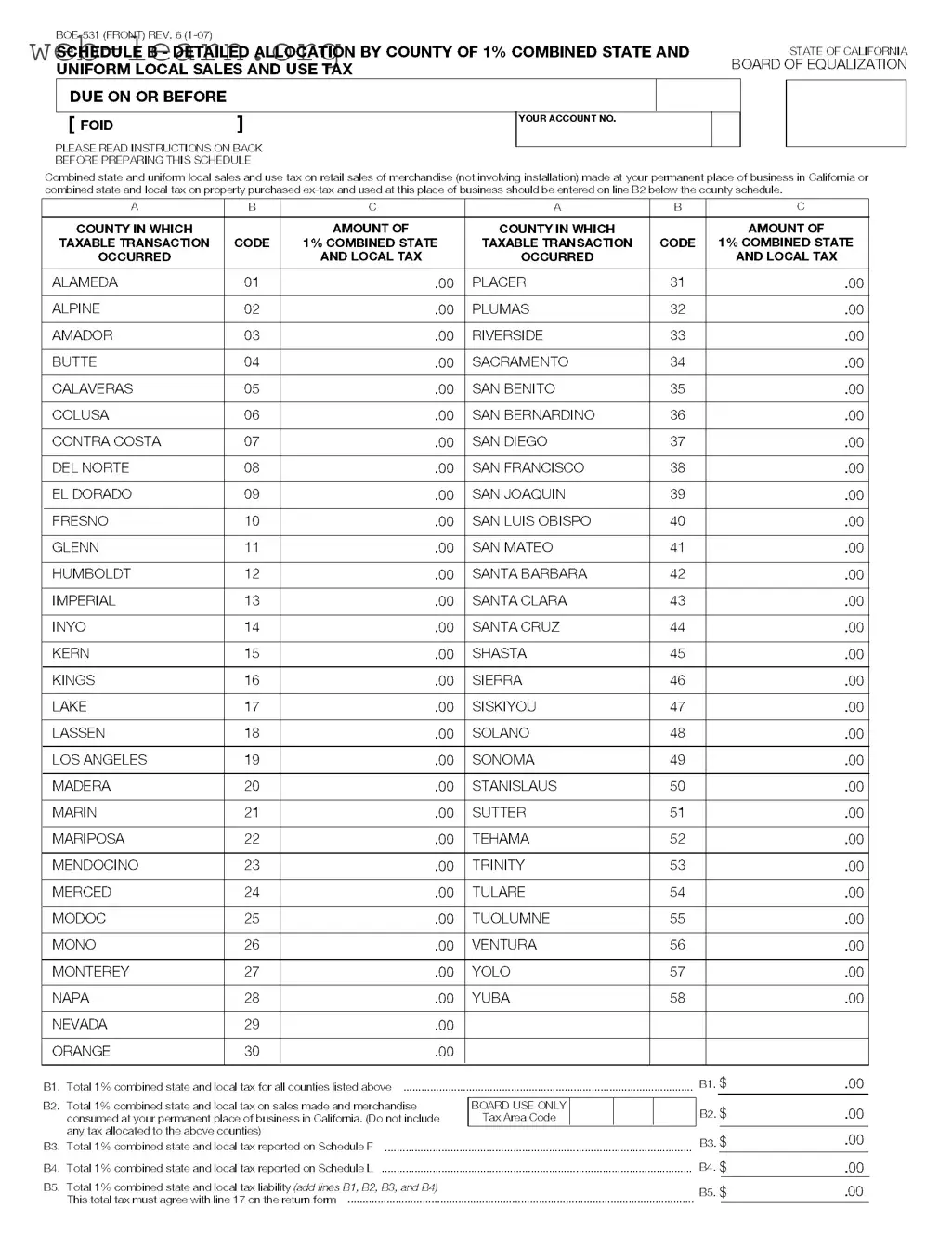

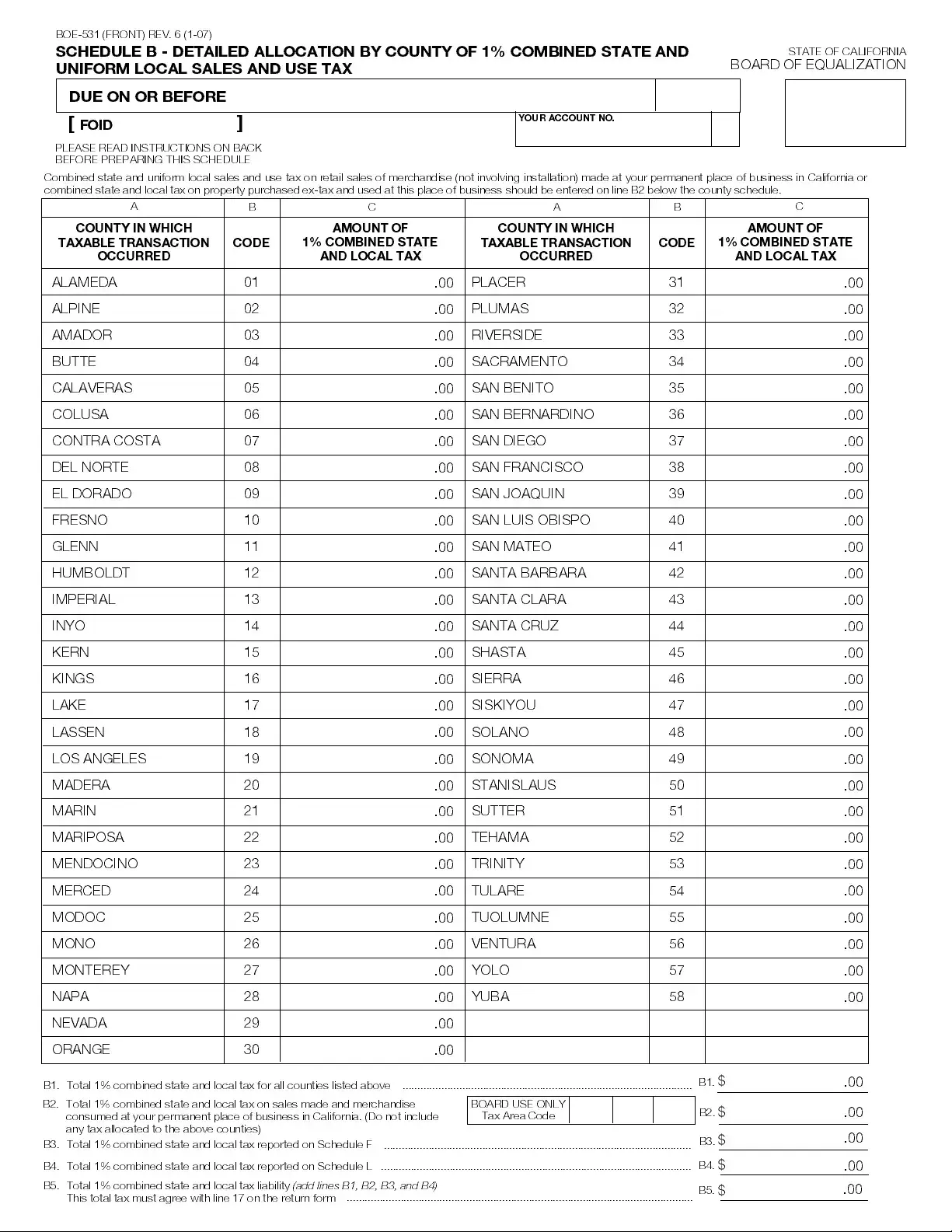

The California BOE-531 form is an essential document for businesses operating within the state, specifically designed to report the combined state and uniform local sales and use tax. This form is particularly important for those who engage in retail sales of merchandise and must accurately allocate tax liabilities across various counties. It provides a structured way to detail the amount of tax due based on where taxable transactions occur, ensuring compliance with state regulations. The form consists of several sections, including a county allocation schedule that lists all counties in California, allowing businesses to specify the tax amounts attributable to each location. Additionally, it includes instructions for different types of businesses, such as auctioneers and vending machine operators, clarifying how to report their specific tax obligations. By completing the BOE-531 form, businesses can ensure that they meet their tax responsibilities while contributing to local and state funding. Understanding the nuances of this form can simplify the tax reporting process and help avoid potential penalties for non-compliance.

| Fact Name | Details |

|---|---|

| Form Purpose | The California BOE 531 form is used to report the 1% combined state and local sales and use tax on retail sales made at a permanent business location in California. |

| Governing Law | This form is governed by California Revenue and Taxation Code Sections 6011 and 6012, which outline the requirements for sales and use tax reporting. |

| Filing Frequency | Businesses must file the BOE 531 form on a quarterly basis, aligning with the state’s sales tax reporting schedule. |

| County Allocation | The form allows businesses to allocate sales tax collected by county, ensuring that tax revenues are distributed appropriately among local jurisdictions. |

| Instructions | Specific instructions are provided on the back of the form, detailing how to accurately complete the schedule based on business activities. |

| Tax Liability Calculation | Total tax liability is calculated by summing the amounts reported on various lines, ensuring that the total matches the return form. |

| Special Cases | Special provisions apply for auctioneers, out-of-state retailers, and vending machine operators, which may affect how taxes are reported on the form. |

Completing the California BOE-531 form involves providing detailed information about sales and use tax allocated by county. After filling out this form, you will need to submit it along with your tax return to the California Board of Equalization by the specified deadline.

The BOE-531 form is a document used in California to report the combined state and local sales and use tax due on retail sales of merchandise. This form helps businesses allocate tax amounts based on where taxable transactions occurred.

Any business that makes retail sales of merchandise in California is required to file this form. This includes businesses with a permanent place of business in the state, as well as certain out-of-state retailers who are authorized to operate in California.

To complete the BOE-531, you will need to enter the amount of 1% combined state and local tax for each county where taxable transactions occurred. Make sure to read the instructions provided on the back of the form for guidance specific to your business activities.

The form requires the following information:

If your business operates in multiple counties, you will need to report the tax amounts for each county separately on the BOE-531. Be sure to include the correct county codes and tax amounts in the designated columns.

Yes, auctioneers have specific reporting requirements. If your auction sales reach $500,000 or more at temporary locations, you must report the tax on a different form, BOE-530-B. For smaller auctions, report the tax on the BOE-531 form for each county where sales occurred.

The BOE-531 must be filed by the due date of your sales and use tax return. Make sure to check the California Board of Equalization’s website for specific deadlines to avoid any penalties.

If you have questions, you can contact the California Board of Equalization directly or consult a tax professional. They can provide assistance tailored to your specific situation and ensure that you complete the form correctly.

Filling out the California BOE-531 form can be a straightforward process, but many people make common mistakes that can lead to delays or issues with their tax filings. One frequent error is not reading the instructions carefully. The form has specific guidelines on how to report sales and use tax, and skipping this step can result in incorrect entries.

Another common mistake is failing to enter the correct county codes. Each county has a designated code, and using the wrong one can complicate the allocation of taxes. It’s essential to double-check these codes against the list provided on the form.

Many individuals also forget to total their amounts correctly. After entering the tax amounts for each county, it’s crucial to ensure that the total on line B1 matches the sum of the individual entries. A simple math error can lead to discrepancies that may require additional follow-up.

Some people neglect to report sales made at their permanent place of business. This is a vital part of the form. If these sales are not included, the total tax liability will be understated, which can lead to penalties.

In addition, individuals often overlook the need to report sales from vending machines. If your business includes vending operations, make sure to include those sales in the appropriate section of the form. Failing to do so can result in an inaccurate tax calculation.

Another mistake is not including the correct amounts for sales made out of state. If your business involves transactions that cross state lines, it’s important to follow the specific reporting guidelines to avoid errors.

Some filers forget to check their figures against previous submissions. Consistency is key. If there are significant discrepancies from previous years, it may raise red flags with the Board of Equalization.

Lastly, a common oversight is not submitting the form on time. Missing the deadline can lead to penalties and interest charges. Ensure that you keep track of important dates and submit your form promptly to avoid these issues.

By being aware of these common mistakes, you can take steps to ensure that your California BOE-531 form is completed accurately and submitted on time.

The California BOE-531 form is a critical document for businesses reporting sales and use tax. However, several other forms and documents often accompany it to ensure compliance with state tax regulations. Below is a list of these related documents, each serving a specific purpose.

Understanding these forms and their purposes is essential for accurate tax reporting and compliance. Each document plays a vital role in the broader context of sales and use tax management in California.

Filling out the California BOE-531 form can seem daunting, but with the right approach, you can navigate it smoothly. Here are some helpful tips on what to do and what to avoid when completing this important document.

By following these dos and don’ts, you can streamline the process of filling out the BOE-531 form and ensure that you meet your tax obligations with confidence.

Misconceptions about the California BOE 531 form can lead to confusion and errors in tax reporting. Here are six common misunderstandings, along with clarifications to help ensure accurate compliance.

This form is required for any business that makes taxable sales in California, regardless of size. Small businesses must also report their sales and use tax accurately.

Even businesses operating from out of state must file if they make sales to California customers. This includes online retailers and vendors who ship products to California.

The BOE 531 form applies to various types of transactions, including those involving services and digital products, depending on the nature of the sale.

California has different local tax rates, and businesses must allocate their sales tax according to the specific counties where sales occurred. This can affect the total tax liability reported on the form.

Sales made at temporary locations, such as fairs or markets, must be reported separately. Businesses should use the appropriate sections of the BOE 531 to ensure compliance.

Businesses can amend the form if errors are discovered after submission. It is crucial to correct any inaccuracies promptly to avoid penalties.

When filling out the California BOE-531 form, there are several important points to keep in mind. Understanding these key takeaways can help ensure accurate reporting and compliance with state tax regulations.