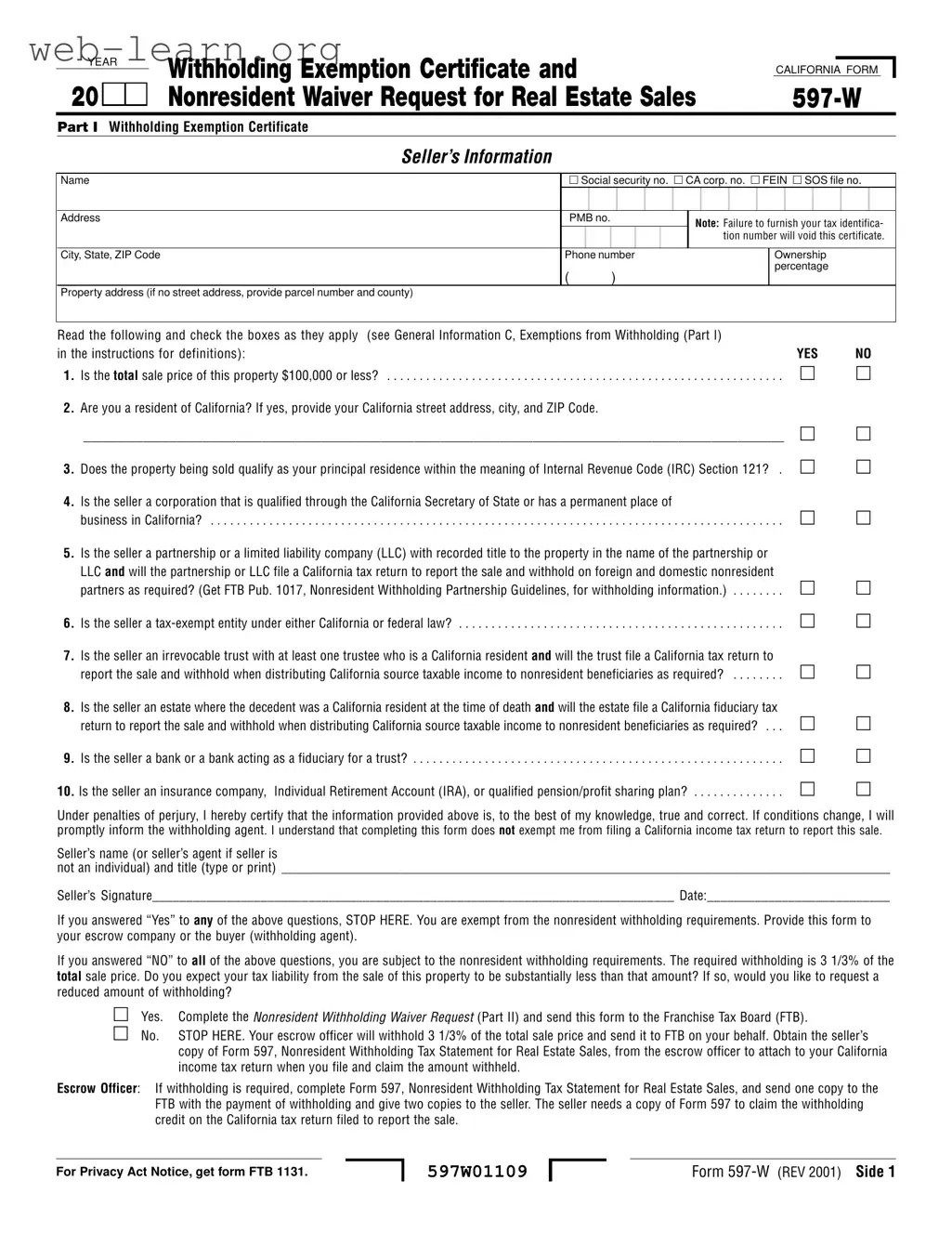

The California 597 W form is an essential document for anyone involved in the sale of real estate in California, particularly for nonresidents. This form serves two primary purposes: it acts as a Withholding Exemption Certificate and a Nonresident Waiver Request. Sellers must provide their personal information, including their name, social security number, and address, along with details about the property being sold. The form includes a series of questions that help determine whether the seller qualifies for an exemption from the state's nonresident withholding requirements. For instance, sellers need to indicate if the sale price is $100,000 or less, or if the property served as their principal residence. If sellers answer "yes" to any of these qualifying questions, they can stop there, as they would be exempt from withholding. However, if they answer "no" to all, they may be subject to a withholding rate of 3 1/3% of the total sale price. Additionally, there is an option to request a reduced withholding amount if the seller believes their tax liability will be significantly lower than the standard withholding. Completing the 597 W form accurately is crucial, as it not only affects the withholding process but also ensures compliance with California tax regulations.

| Fact Name | Details |

|---|---|

| Purpose | The California 597 W form serves as a Withholding Exemption Certificate and Nonresident Waiver Request for Real Estate Sales. |

| Governing Law | The form is governed by California Revenue and Taxation Code Section 18662. |

| Eligibility | It is used by sellers who may qualify for exemptions from nonresident withholding on real estate transactions. |

| Sale Price Threshold | If the total sale price of the property is $100,000 or less, sellers may be exempt from withholding. |

| Residency Requirement | Sellers who are residents of California may also qualify for withholding exemptions. |

| Corporate Sellers | Corporations qualified in California can complete the form to claim exemption from withholding. |

| Trusts and Estates | Irrevocable trusts and estates of California residents may also be exempt if they file appropriate tax returns. |

| Withholding Rate | If no exemptions apply, the withholding rate is 3 1/3% of the total sale price. |

Filling out the California 597 W form is a straightforward process, but it requires careful attention to detail. This form is essential for sellers of real estate in California, particularly for non-residents. Once completed, the form needs to be submitted to the appropriate parties involved in the transaction, such as the escrow company or the buyer.

What is the California 597 W form?

The California 597 W form serves two primary purposes: it acts as a Withholding Exemption Certificate and as a Nonresident Waiver Request for Real Estate Sales. This form is essential for sellers who may be exempt from nonresident withholding requirements when selling property in California.

Who needs to fill out the 597 W form?

Sellers who are nonresidents of California and are selling real estate in the state must complete this form. It is particularly important for those who believe they qualify for an exemption from withholding or wish to request a reduced amount of withholding.

What information is required on the form?

The form requires detailed information about the seller, including:

Additionally, sellers must answer specific questions regarding their residency status and the nature of the property being sold.

What are the exemptions from withholding?

Exemptions from withholding may apply if:

If any of these conditions are true, the seller may be exempt from withholding.

What happens if I answer "No" to all exemption questions?

If a seller answers "No" to all exemption questions, they are subject to nonresident withholding. This means that 3 1/3% of the total sale price will be withheld and sent to the Franchise Tax Board (FTB) on their behalf.

Can I request a reduced withholding amount?

Yes, if a seller expects their tax liability from the sale to be substantially less than the withholding amount, they can request a reduced amount. This requires completing the Nonresident Withholding Waiver Request section of the form and providing necessary documentation.

How do I submit the form?

The completed form should be provided to the escrow company or the buyer, who acts as the withholding agent. If requesting a waiver, the seller must also send the form to the FTB.

What documentation is needed to support a waiver request?

To support a waiver request, sellers must provide documentation that verifies their adjusted basis in the property, as well as any other information required by the FTB. This may include details about how the seller acquired the property and its use over time.

What should I do after submitting the form?

Once the form is submitted, sellers should obtain a copy of Form 597, the Nonresident Withholding Tax Statement for Real Estate Sales, from the escrow officer. This form is necessary for filing a California income tax return and claiming the amount withheld.

What are the penalties for providing false information?

Providing false information on the 597 W form can lead to penalties under perjury laws. It is crucial for sellers to ensure that all information provided is accurate and complete.

Filling out the California 597 W form can be a straightforward process, but many individuals make common mistakes that can lead to complications. One prevalent mistake is failing to provide a complete tax identification number. This number is crucial, and without it, the form becomes void. Sellers must ensure they enter their Social Security number, California corporation number, or Federal Employer Identification Number accurately to avoid delays.

Another frequent error occurs when sellers do not check the boxes correctly in Part I. Each question is designed to determine eligibility for withholding exemptions. If a seller answers “yes” to any question but does not check the corresponding box, it can create confusion and potentially lead to unnecessary withholding. It is essential to read each question carefully and respond accordingly.

Many people also overlook the importance of providing accurate ownership percentages. If the property is co-owned, each owner must indicate their respective percentage of ownership. Missing or incorrect percentages can complicate the withholding process and may lead to issues during tax filing.

Additionally, some sellers forget to sign and date the form. This step is vital because the signature certifies that the information provided is true and correct. Without a signature, the form may not be accepted by the escrow company or the Franchise Tax Board, resulting in delays or additional complications.

Another mistake involves not providing the correct property address. If a seller does not include a complete address or, in cases without a street address, fails to provide the parcel number and county, it can lead to significant issues. Accurate property information is essential for proper processing.

Some individuals also fail to provide adequate documentation to support their claims for exemptions or reduced withholding. The form requires additional information to verify the adjusted basis and other claims. Without this documentation, the Franchise Tax Board may not process the request, leading to potential withholding.

It is also common for sellers to misinterpret the requirements for a withholding waiver. Many do not realize that if they expect their tax liability to be substantially less than the withholding amount, they must complete the Nonresident Withholding Waiver Request (Part II) properly. Failing to do so can result in unnecessary withholding from the sale proceeds.

Lastly, sellers sometimes neglect to obtain a copy of Form 597 from their escrow officer. This form is essential for claiming any withholding credit on their California income tax return. Keeping track of all necessary documents is crucial to ensure a smooth tax filing process after the sale.

The California 597 W form is an essential document in real estate transactions involving nonresident sellers. It helps determine whether withholding is required on the sale of property. Along with this form, several other documents are often used to ensure compliance with tax regulations and to facilitate the sale process. Below is a list of related forms and documents that may be necessary.

Understanding the role of these documents is crucial for both sellers and buyers in California's real estate market. Each form serves a specific purpose in ensuring compliance with tax laws and protecting the interests of all parties involved in the transaction.

The California Form 597 W, which serves as a Withholding Exemption Certificate and Nonresident Waiver Request for Real Estate Sales, shares similarities with several other documents used in real estate transactions and tax reporting. Below are four such documents, each accompanied by a brief explanation of its relationship to Form 597 W.

When filling out the California 597 W form, it is important to follow specific guidelines to ensure accuracy and compliance. Below is a list of things to do and avoid during this process.

Understanding the California 597 W form is essential for anyone involved in real estate transactions in the state. However, several misconceptions persist regarding its purpose and implications. Here are four common misconceptions:

Many believe that only California residents need to complete the 597 W form. In reality, this form applies to both residents and non-residents involved in real estate sales in California. Non-residents must also comply with withholding requirements unless they qualify for an exemption.

Some individuals think that simply filling out the 597 W form automatically exempts them from withholding. However, exemption is only granted if the seller answers "Yes" to specific questions related to their circumstances. If all answers are "No," withholding is mandatory.

It is a common belief that the withholding rate is always 3 1/3% of the total sale price. While this is the standard rate, sellers can request a reduced amount if they anticipate their tax liability will be significantly lower than the withholding amount. This requires additional documentation and approval.

Some sellers mistakenly think that if they sell their property at a loss, they do not need to complete the 597 W form. Regardless of the sale price or profit/loss situation, the form must still be completed to determine withholding obligations.

Filling out and using the California 597 W form is crucial for sellers involved in real estate transactions. Here are four key takeaways to consider: