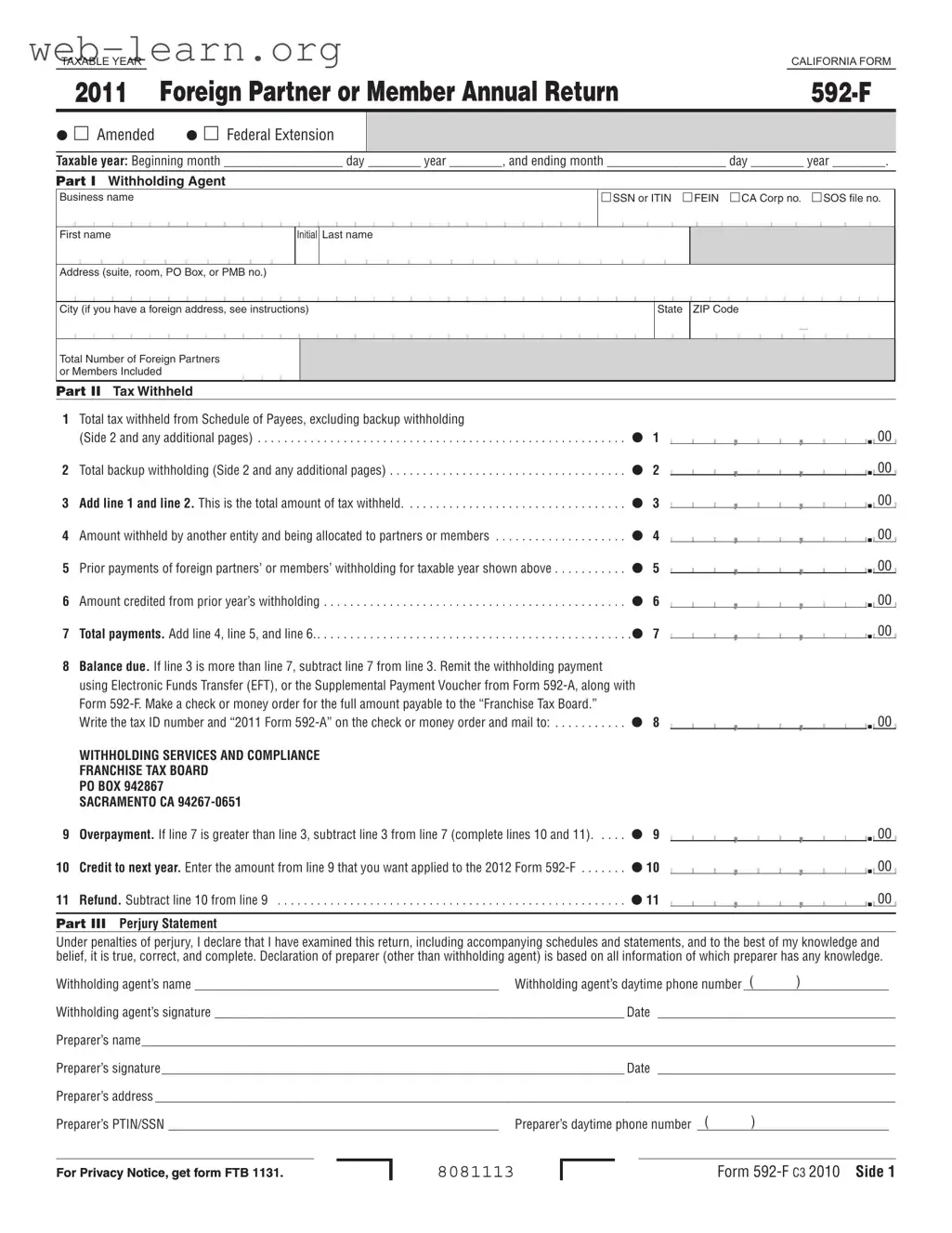

The California Form 592-F is a crucial document for partnerships and limited liability companies (LLCs) that have foreign partners or members. This form is used to report the total withholding tax for the taxable year and to allocate that income and related withholding amounts to those foreign partners or members. It is important to note that, as of 2011, the maximum personal income tax rate has been set at 9.3%. The form is structured into several parts, starting with the identification of the withholding agent, who must provide their business name and tax identification number. The form also requires detailed information about the total tax withheld, including any backup withholding amounts. Additionally, it allows for the reporting of prior payments and credits from previous years. To ensure compliance, the withholding agent must file this form by the 15th day of the 4th month following the close of the taxable year, or by the 15th day of the 6th month if all partners are foreign. The form must be submitted to the Franchise Tax Board along with any necessary payments. Understanding the requirements and deadlines associated with Form 592-F is essential for any entity engaging with foreign partners or members in California.

| Fact Name | Details |

|---|---|

| Purpose | Form 592-F is used to report the total withholding for the year on foreign partners or members under California Revenue and Taxation Code Section 18666. |

| Filing Deadline | The form must be filed by the 15th day of the 4th month following the end of the partnership's or LLC's taxable year. |

| Backup Withholding Rate | The California backup withholding rate is set at 7% of the payment for certain payees. |

| Amendments | Only the withholding agent can amend Form 592-F by completing a new form, checking the “Amended” box, and providing an explanation of the changes. |

| Electronic Filing Requirement | Form 592-F must be filed electronically if the number of payees is 250 or more, using FTB's Secure Web Internet File Transfer (SWIFT). |

Completing the California Form 592-F requires careful attention to detail. This form is essential for reporting withholding on foreign partners or members. Follow these steps to ensure accurate submission.

Once completed, ensure that the form is signed and dated. Submit it along with any necessary payment to the Franchise Tax Board at the specified address. Keep a copy for your records, as it may be required for future reference or audits.

What is the California 592 F form?

The California 592 F form is used by partnerships and limited liability companies (LLCs) to report withholding on income earned by foreign partners or members. It summarizes the total tax withheld for the year and allocates that withholding to the foreign partners or members. This form helps ensure compliance with California tax laws regarding non-resident income taxation.

Who needs to file the 592 F form?

Any partnership or LLC that has foreign partners or members must file the 592 F form. This includes entities that are not based in California but have partners or members who are foreign individuals or entities. If all partners or members are foreign, the form must be filed within specific deadlines.

When is the 592 F form due?

The 592 F form is due on or before the 15th day of the 4th month after the close of the partnership's or LLC's taxable year. If all partners or members are foreign, the deadline extends to the 15th day of the 6th month after the close of the taxable year.

What information is required on the form?

The form requires the following information:

How do I amend a previously filed 592 F form?

To amend a filed 592 F form, complete a new form with the correct information. Check the "Amended" box at the top of the form. Include a letter explaining the changes made and why. Send the amended form and letter to the address provided on the form.

What happens if I miss the filing deadline?

If you miss the filing deadline, you may incur penalties and interest on the unpaid tax. The penalties are assessed based on how late the form is filed. It's important to file as soon as possible to minimize any potential penalties.

Can I file the 592 F form electronically?

Yes, if you have 250 or more payees, you must file the 592 F form electronically using the Franchise Tax Board's Secure Web Internet File Transfer (SWIFT). However, you still need to provide paper copies of the Schedule of Payees to each payee.

What is backup withholding?

Backup withholding is a tax withholding requirement that applies to certain payments made to individuals or entities that do not provide a valid taxpayer identification number. For California, the backup withholding rate is 7%. If applicable, this amount must be reported on the 592 F form.

Where do I send the completed 592 F form?

Mail the completed 592 F form, along with any required payment and the Supplemental Payment Voucher from Form 592-A, to the Franchise Tax Board at the following address:

WITHHOLDING SERVICES AND COMPLIANCE

FRANCHISE TAX BOARD

PO BOX 942867

SACRAMENTO CA 94267-0651

How can I get help with the 592 F form?

If you need assistance, you can call the Withholding Services and Compliance automated telephone service at 888.792.4900 or 916.845.4900. Additionally, you can visit the Franchise Tax Board's website at ftb.ca.gov for more information and resources.

Completing the California Form 592-F can be challenging, and mistakes can lead to delays or penalties. One common error is failing to include the correct taxable year. Make sure to accurately enter the beginning and ending dates for the partnership’s or LLC’s taxable year. If these dates are incorrect, it could result in processing issues.

Another frequent mistake is not properly identifying the withholding agent. The business name, ID number, and address must be entered correctly. If you are a partnership or LLC, ensure that you provide your entity's information rather than that of the entity that originally withheld payments. This distinction is crucial for proper processing.

Many filers also overlook the importance of calculating the total tax withheld accurately. On Line 1, you must report the total withholding, excluding backup withholding. This figure should be carefully calculated to avoid discrepancies that could lead to penalties.

Additionally, some people forget to include the total backup withholding on Line 2. This amount must be reported separately, and failure to do so can result in an inaccurate total tax withheld on Line 3. Always double-check your calculations to ensure accuracy.

Another common error involves the Schedule of Payees. It is essential to complete this section thoroughly and accurately. If you have multiple payees, use the additional Schedule of Payees provided on Side 2 of Form 592-F. Do not create your own version, as only the official form will be accepted.

Some filers neglect to report the amount withheld by another entity on Line 4. This information is critical for accurately allocating credits to foreign partners or members. If this line is left blank, it could lead to confusion and potential penalties.

Moreover, failing to check the “Amended” box when submitting a corrected form is another mistake that can cause issues. If you need to amend your return, ensure you complete a new Form 592-F, check the appropriate box, and include a letter explaining the changes made.

Lastly, many people forget to sign and date the form. The perjury statement requires the withholding agent’s signature, as well as the preparer’s signature if applicable. Missing signatures can result in the form being rejected, causing delays in processing.

The California Form 592-F is an essential document for reporting withholding on foreign partners or members in a partnership or LLC. However, it is often accompanied by various other forms and documents that serve specific purposes in the tax reporting process. Below is a list of related forms that may be used in conjunction with Form 592-F, along with a brief description of each.

Understanding these forms can help ensure compliance with California tax regulations and facilitate accurate reporting of income and withholding for foreign partners or members. Each document plays a critical role in the overall process, making it essential to handle them with care and attention to detail.

When filling out the California 592 F form, it is important to follow specific guidelines to ensure accuracy and compliance. Here are five things you should and shouldn't do:

This form is specifically designed for foreign partners or members of partnerships and LLCs. It is crucial for reporting withholding for individuals or entities that are not U.S. residents.

While it is true that the withholding agent does not need to submit Form 592-B to the Franchise Tax Board (FTB) when filing Form 592-F, they are still required to provide copies of Form 592-B to the partners or members.

This form should not be used for real estate withholding. If you are involved in real estate transactions, you must use Form 593 instead.

The due date varies. If all partners or members are foreign, the form is due on the 15th day of the 6th month after the close of the taxable year. Otherwise, it is due on the 15th day of the 4th month following the close of the taxable year.

There are indeed penalties for late filing. The penalties can range from $15 to $50 per payee, depending on how late the form is submitted.

Payments must be properly allocated to the respective partners or members. It is essential to report the correct amounts on the Schedule of Payees to ensure proper credit.

If there are 250 or more payees, electronic filing is required. This helps streamline the process and ensures compliance with the FTB's regulations.

Backup withholding may apply, and it is essential to report any backup withholding amounts separately on the form. This ensures that all tax obligations are met.

Purpose of Form 592-F: Use this form to report the total withholding for foreign partners or members under California law. It helps pass-through entities allocate withholding credits.

Who Should File: Only partnerships and LLCs with foreign partners or members need to file this form. Do not use it for domestic nonresident partners or real estate transactions.

Filing Deadlines: Submit Form 592-F by the 15th day of the 4th month after the taxable year ends. If all partners are foreign, the deadline extends to the 15th day of the 6th month.

Amending the Form: If corrections are necessary, file a new Form 592-F, check the "Amended" box, and include a letter explaining the changes.

Payment Instructions: If tax is owed, remit payment using Electronic Funds Transfer (EFT) or the Supplemental Payment Voucher from Form 592-A. Include a check payable to the “Franchise Tax Board.”

Backup Withholding: If applicable, report backup withholding at a rate of 7%. Ensure to check the appropriate box for payees subject to this withholding.