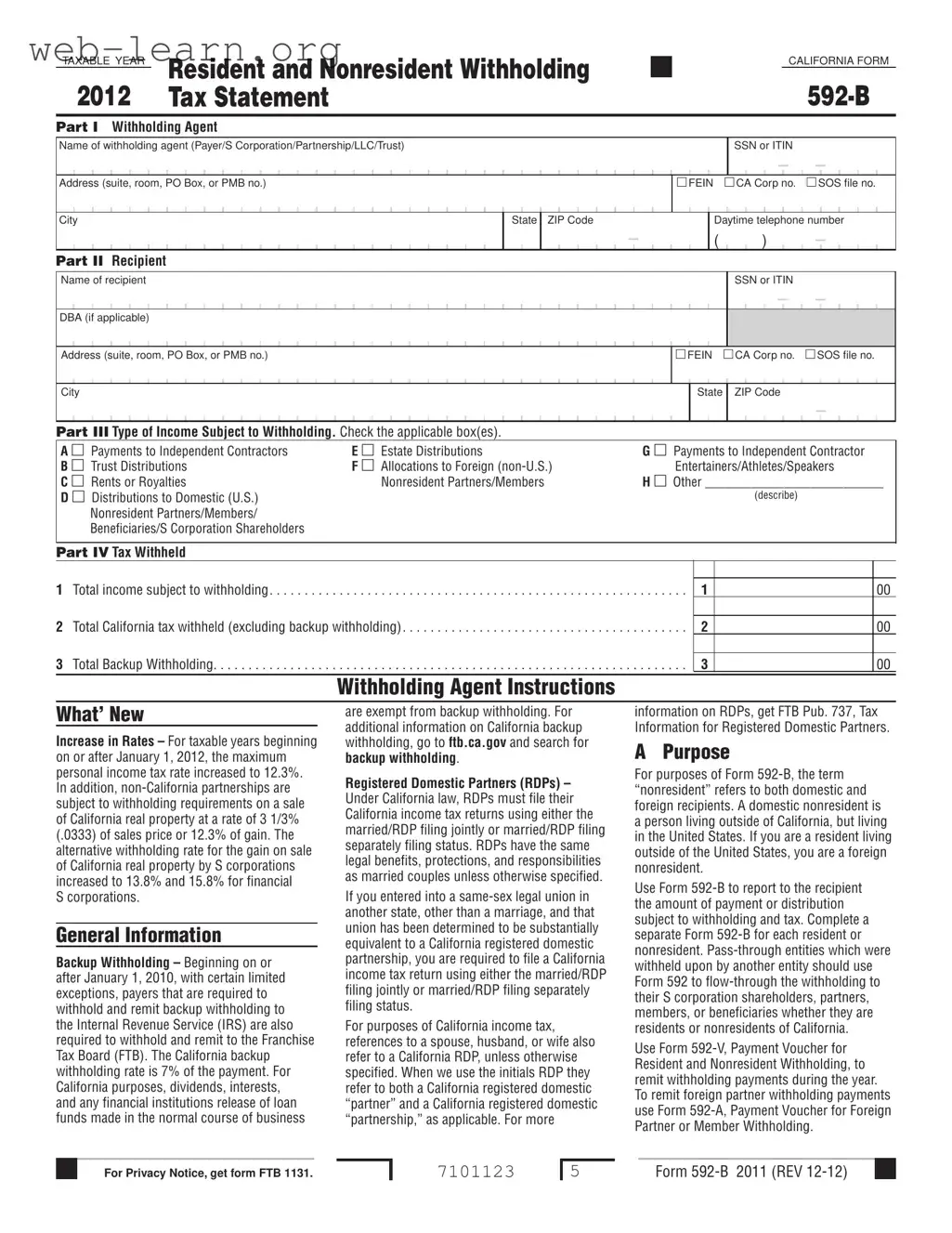

The California 592 B form plays a crucial role in the state’s tax withholding process, particularly for payments made to both residents and nonresidents. This form is used by withholding agents—such as businesses, partnerships, and trusts—to report the amounts withheld from various types of income. It includes essential details like the withholding agent's name and identification number, as well as the recipient's information. The form also categorizes the type of income subject to withholding, which can range from payments to independent contractors to estate distributions and royalties. Additionally, it outlines the total income subject to withholding and the corresponding California tax withheld. Withholding agents must provide this form to recipients by January 31 of the following year, ensuring that all parties are informed about their tax obligations. The 592 B form not only helps maintain compliance with California tax laws but also assists recipients in accurately reporting their income when filing their tax returns. Understanding this form is vital for anyone involved in transactions that require tax withholding in California.

| Fact Name | Details |

|---|---|

| Purpose | Form 592-B is used to report amounts withheld from payments made to residents and nonresidents in California. |

| Governing Law | The form is governed by California Revenue and Taxation Code Sections 18662 and 18666. |

| Tax Year | The form must reflect the calendar year in which the withholding took place. |

| Deadline for Submission | Withholding agents must provide Form 592-B to recipients by January 31 of the following year. |

| Backup Withholding Rate | The backup withholding rate in California is set at 7% of the payment amount. |

| Types of Income | Income types subject to withholding include rents, royalties, and payments to independent contractors. |

| Penalties for Noncompliance | Failure to provide the form timely can result in penalties of $50 per payee statement. |

| Record Keeping Requirement | Withholding agents must retain proof of withholding for a minimum of four years. |

Completing the California 592-B form is essential for reporting withholding taxes related to payments made to residents and nonresidents. The following steps outline the process to accurately fill out this form.

After completing the form, it is important to retain a copy for your records. Timely submission will help avoid potential penalties associated with late or incorrect filings.

What is the California Form 592-B?

The California Form 592-B is a tax statement used to report the amount of income subject to withholding for both residents and nonresidents of California. This form is primarily utilized by withholding agents, such as S corporations, partnerships, LLCs, and trusts, to inform recipients about the tax withheld from their payments. It is crucial for ensuring compliance with California tax laws.

Who needs to complete Form 592-B?

Any individual or entity that has withheld taxes on payments to residents or nonresidents must complete Form 592-B. This includes those who have withheld backup withholding. If you are a pass-through entity that has been withheld upon, you also need to flow-through the withholding credit to your shareholders, partners, members, or beneficiaries. It is important to complete this form accurately to avoid penalties.

When is Form 592-B due?

Form 592-B must be provided to each recipient by January 31 following the close of the calendar year. However, if you are a broker, the deadline is February 15. For foreign partners in a partnership or members of an LLC, the form must be issued on or before the 15th day of the fourth month following the close of the taxable year. Timely submission is key to avoiding penalties.

What are the penalties for not providing Form 592-B on time?

Failure to furnish complete and correct copies of Form 592-B to recipients by the due date can lead to penalties. Specifically, there is a $50 penalty for each payee statement not provided on time. If the failure is due to intentional disregard of the requirement, the penalty increases to either $100 or 10% of the amount required to be reported, whichever is greater. It is essential to comply with these deadlines to avoid unnecessary costs.

How do I report the withholding on my tax return?

To claim the withholding reported on Form 592-B, you must include the amount from Part IV, line 2 on your California tax return. Attach a copy of Form 592-B to your return. If you received a composite statement from a broker, you only need to include the relevant information from Form 592-B. Keeping accurate records will help ensure that you report your income correctly and claim any withholding credits.

Where can I find more information about Form 592-B?

For additional information, you can visit the California Franchise Tax Board's website at ftb.ca.gov. You can also contact their automated telephone service at 888.792.4900 or 916.845.4900 for assistance. If you prefer to write, you can reach out to the Withholding Services and Compliance department at the address provided on their website. They can provide guidance and answer any specific questions you may have.

Filling out the California 592-B form can be straightforward, but many people make common mistakes that can lead to delays or penalties. One frequent error is not providing complete taxpayer identification numbers (TINs) for all payees. This information is crucial for the Franchise Tax Board (FTB) to track payments and ensure proper withholding. Without accurate TINs, the form may be rejected or returned, causing unnecessary complications.

Another common mistake is failing to complete all fields on the form. Every section is important, and incomplete forms can lead to processing delays. Ensure that both the withholding agent and recipient information are fully filled out, including names, addresses, and identification numbers. Omitting even a small detail can result in significant issues down the line.

Timeliness is also key. Many people do not submit the form by the required deadlines. For instance, Form 592-B must be provided to each recipient by January 31 of the following year. Missing this deadline can lead to penalties, which can add up quickly. Keeping track of due dates is essential for avoiding these unnecessary costs.

Some individuals mistakenly use the wrong taxable year on the form. The year in the upper left corner must match the calendar year in which the withholding took place. If this is incorrect, it can create confusion and lead to problems with tax reporting. Always double-check that the year reflects when the income was earned.

Another frequent oversight involves the address format. When providing a Private Mail Box (PMB) address, it is important to include "PMB" first, followed by the box number. Failing to format the address correctly can result in misdelivery or delays in processing.

Additionally, some filers neglect to check the appropriate boxes for the type of income subject to withholding. This is a crucial step, as it determines the withholding rate and the amount that must be reported. Checking the wrong box can lead to incorrect calculations and potential penalties.

Many people also overlook the requirement to keep proof of withholding for at least four years. This documentation is vital if the FTB requests it later. Not retaining this information can complicate matters if there are questions or audits in the future.

Lastly, failing to provide accurate and timely copies of Form 592-B to recipients can result in penalties. Each payee must receive a complete and correct form by the due date. If not, the withholding agent may face fines for each form that is not provided on time. It is essential to ensure that all recipients receive their forms promptly to avoid these consequences.

The California 592 B form is essential for reporting withholding on payments made to residents and nonresidents. When dealing with this form, there are several other documents that often accompany it. Each of these documents serves a specific purpose in the withholding and reporting process. Understanding them can help ensure compliance and streamline your tax reporting obligations.

Being familiar with these forms can simplify the tax reporting process and help you avoid potential pitfalls. Each document plays a vital role in ensuring that withholding is properly reported and that tax obligations are met accurately and on time.

When filling out the California 592 B form, it is important to follow specific guidelines to ensure accuracy and compliance. Here are some do's and don'ts to keep in mind:

This form applies to both residents and nonresidents. It is used to report withholding on payments made to individuals living outside California, including those within the United States.

Any person or entity that withholds payments to residents or nonresidents, regardless of size, is required to complete this form.

This form covers various types of income, including payments to independent contractors, rents, royalties, and distributions from trusts or estates.

Even if no taxes were withheld, Form 592 B must be completed to report the payments made to recipients.

Timely filing is crucial. The form must be provided to recipients by January 31 of the following year, or penalties may apply.

Recipients must attach Form 592 B to their California tax return to claim the withholding credit. Ignoring this can lead to issues with tax liability.

The details on this form are essential for accurate tax reporting and compliance. Both payers and recipients rely on this information for their tax obligations.

Failure to provide accurate and complete information can result in significant penalties. It’s crucial to ensure all details are correct before submission.

Understanding the California Form 592-B is essential for both withholding agents and recipients. Here are key takeaways regarding its completion and use: