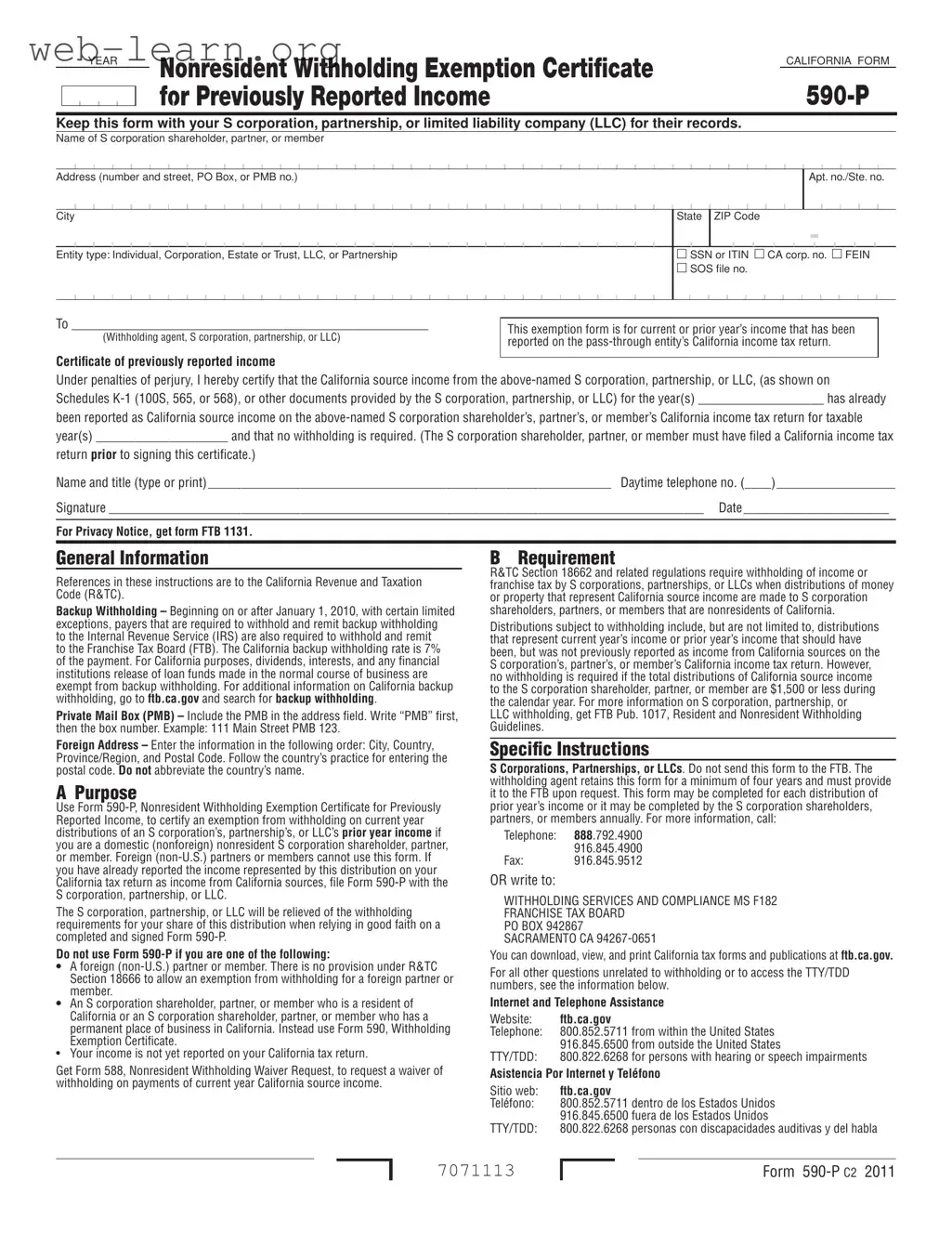

The California Form 590 P, known as the Nonresident Withholding Exemption Certificate for Previously Reported Income, plays a crucial role for nonresident shareholders, partners, or members of S corporations, partnerships, and limited liability companies (LLCs). This form certifies that certain income has already been reported on a California tax return, thus exempting the individual from additional withholding on current distributions of that income. To utilize this form, one must ensure they are a domestic nonresident and that the income in question has been duly reported in prior tax filings. It's important to note that foreign partners or members are not eligible to use this form. The 590 P form must be kept on file by the entity for at least four years, providing a safeguard against unnecessary withholding. By accurately completing and submitting this form, nonresidents can avoid the burden of withholding taxes on distributions that represent income already accounted for in their tax returns. Understanding the nuances of this form is essential for compliance and financial planning, making it imperative for affected individuals to stay informed and act promptly.

| Fact Name | Details |

|---|---|

| Purpose | Form 590-P certifies an exemption from withholding on current year distributions of prior year income for nonresident S corporation shareholders, partners, or members. |

| Eligibility | This form is only for domestic nonresident individuals. Foreign partners or members cannot use Form 590-P. |

| Governing Law | The form is governed by California Revenue and Taxation Code Section 18662. |

| Withholding Requirements | No withholding is required if total distributions are $1,500 or less during the calendar year. |

| Retention Period | The withholding agent must retain Form 590-P for a minimum of four years and provide it to the Franchise Tax Board upon request. |

Completing the California 590 P form is essential for nonresident S corporation shareholders, partners, or members who wish to certify an exemption from withholding on distributions of previously reported income. Follow the steps below to ensure that the form is filled out correctly.

Once completed, keep the form with your S corporation, partnership, or LLC for their records. This document will help ensure that the withholding requirements are met appropriately.

What is the purpose of California Form 590-P?

California Form 590-P, also known as the Nonresident Withholding Exemption Certificate for Previously Reported Income, is used to certify that certain income has already been reported on a California tax return. This form is specifically for nonresident shareholders, partners, or members of S corporations, partnerships, or LLCs. When this form is completed and submitted, it allows these entities to avoid withholding taxes on distributions that represent income already reported in prior years.

Who should use Form 590-P?

This form is intended for domestic (nonforeign) nonresident individuals who are shareholders, partners, or members of an S corporation, partnership, or LLC. If you have reported income from these entities on your California tax return, you can use Form 590-P to claim an exemption from withholding on current year distributions of that previously reported income. However, foreign partners or members cannot use this form.

What are the requirements for using Form 590-P?

To use Form 590-P, the following conditions must be met:

If you are a California resident or have a permanent place of business in California, you should use Form 590 instead.

What happens if my total distributions are $1,500 or less?

If your total distributions of California source income from the S corporation, partnership, or LLC are $1,500 or less during the calendar year, no withholding is required. This means that you do not need to submit Form 590-P for those distributions, as they fall below the threshold that triggers withholding requirements.

How long should the withholding agent keep Form 590-P?

The withholding agent, which can be the S corporation, partnership, or LLC, must retain Form 590-P for a minimum of four years. This form may need to be provided to the Franchise Tax Board (FTB) upon request. It’s important for the withholding agent to keep accurate records, as this helps ensure compliance with tax regulations.

Where can I find more information about withholding requirements?

For additional information regarding withholding requirements for S corporations, partnerships, or LLCs, you can refer to FTB Publication 1017, which outlines guidelines for both resident and nonresident withholding. For further assistance, you can visit the FTB website at ftb.ca.gov or contact them directly at their provided phone numbers.

Filling out the California 590 P form can be straightforward, but many people make common mistakes that can lead to complications. One frequent error is failing to provide accurate personal information. Ensure that your name, address, and taxpayer identification number (SSN or ITIN) are correct. A simple typo can cause delays or issues with processing your form.

Another mistake is not including the correct entity type. The form asks for your entity type—whether you are an individual, corporation, LLC, or partnership. Omitting this detail can lead to confusion and may result in your form being rejected.

Many individuals forget to indicate the correct withholding agent. This is the S corporation, partnership, or LLC that you are associated with. Make sure to fill in this section completely. If you leave it blank, it may be unclear who the form pertains to, leading to potential problems.

People often overlook the requirement to report previously reported income. The form is designed for income that has already been declared on your California tax return. If you haven’t reported the income yet, you should not use this form. Instead, consider filing Form 588 for a waiver.

Another common oversight is not signing the form. Your signature is crucial as it certifies that the information you provided is true. Without it, the form is incomplete and cannot be processed.

Additionally, some individuals neglect to include a daytime telephone number. This can be a barrier if the withholding agent needs to reach you for clarification or additional information. Including a contact number can expedite the process.

People also sometimes forget to keep a copy of the completed form for their records. It’s important to maintain a personal copy in case any questions arise later regarding your withholding exemption.

Another mistake involves misunderstanding the income threshold. If your total distributions of California source income are $1,500 or less during the calendar year, you may not need to fill out this form. Be sure to check your totals to see if this applies to you.

Lastly, many individuals fail to read the instructions thoroughly. The California 590 P form has specific guidelines that need to be followed. Taking the time to read the instructions can help prevent these common mistakes and ensure that your form is filled out correctly.

When dealing with the California 590 P form, several other documents may come into play. Each serves a specific purpose in the process of managing nonresident withholding exemptions. Understanding these documents can help ensure compliance and smooth transactions.

Having these forms and documents ready can make the process much easier. They help clarify your tax situation and ensure that you meet all necessary requirements. Always keep them organized and accessible to avoid any last-minute issues.

When filling out the California 590 P form, there are important guidelines to follow. Here’s a list of things you should and shouldn’t do:

Here are ten common misconceptions about the California 590 P form, along with explanations to clarify each point:

When filling out and using the California 590 P form, it is essential to understand its purpose and requirements. Here are key takeaways to guide you through the process:

Understanding these key points will help ensure that you fill out the California 590 P form accurately and comply with the necessary tax regulations. Take your time to review the requirements and seek assistance if needed.