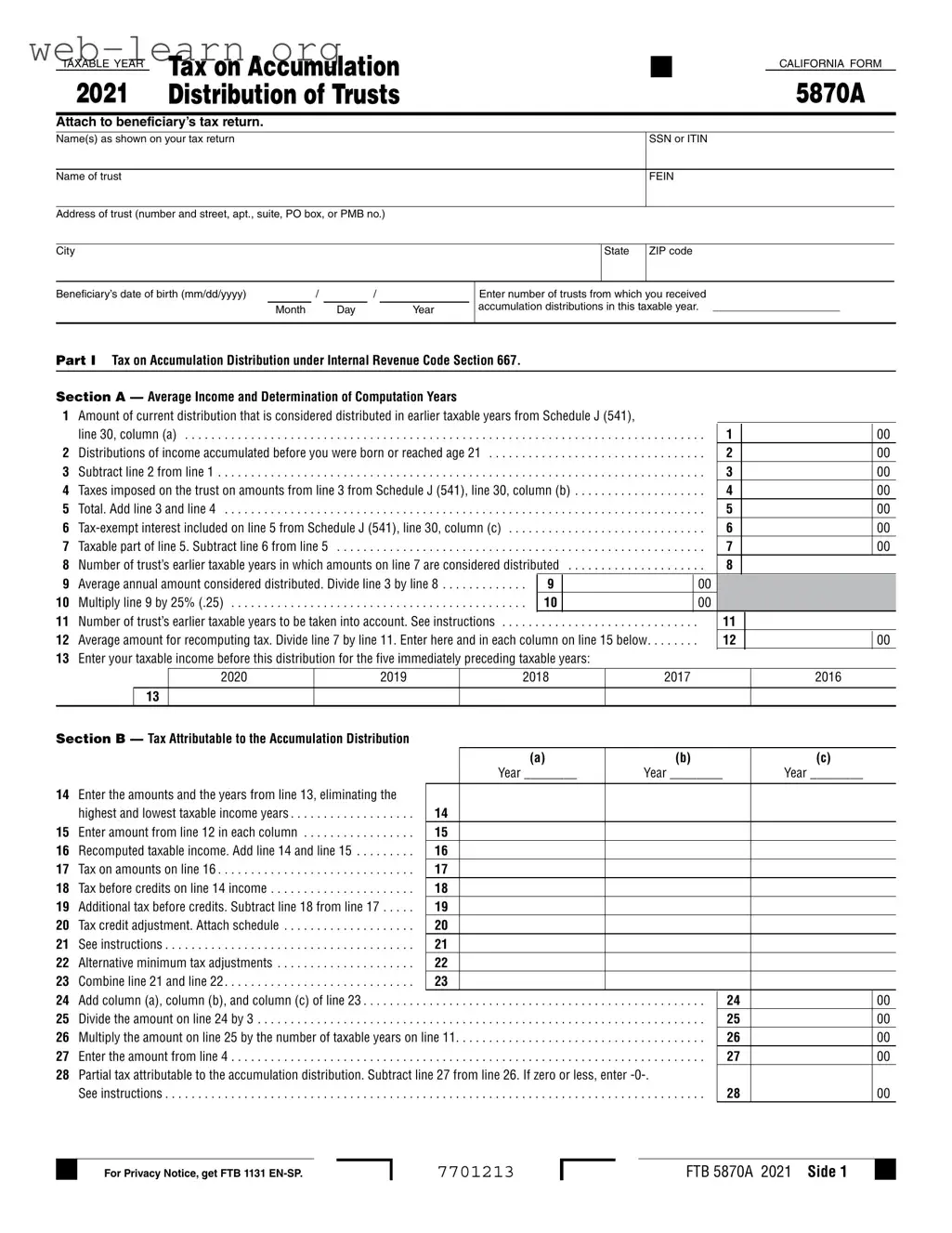

The California 5870A form plays a crucial role in the tax reporting process for beneficiaries of trusts. Designed for the 2020 tax year, this form is primarily used to report the tax on accumulation distributions from trusts, ensuring that beneficiaries accurately account for their received distributions. It requires specific information, including the name of the trust, its federal employer identification number (FEIN), and the beneficiary’s details, such as their Social Security Number (SSN) or Individual Taxpayer Identification Number (ITIN). The form is divided into several sections, each focusing on different aspects of the trust distributions. Part I addresses the tax on accumulation distributions under Internal Revenue Code Section 667, guiding beneficiaries through calculations related to prior taxable years and average annual amounts. Part II focuses on distributions of previously untaxed trust income, while Part III pertains to the Mental Health Services Tax. Beneficiaries must attach this form to their tax returns, making it essential for accurate tax reporting and compliance.

| Fact Name | Description |

|---|---|

| Purpose | The California Form 5870A is used to report taxes on accumulation distributions from trusts to beneficiaries. |

| Tax Year | This form is specifically for the taxable year 2020, as indicated at the top of the form. |

| Governing Law | The form operates under the Internal Revenue Code Section 667 and the California Revenue and Taxation Code Section 17745. |

| Filing Requirement | Beneficiaries must attach Form 5870A to their individual tax returns when reporting accumulation distributions received from trusts. |

Filling out the California 5870A form is an important step in reporting trust distributions. This form must be attached to the beneficiary's tax return and requires specific information about the trust and the distributions received. Following these steps will help ensure that the form is completed accurately.

Next, complete Part I by calculating the average income and determining the computation years. Start with the current distribution amount from Schedule J, then follow through with the calculations outlined in the form. Move on to Section B to calculate the tax attributable to the accumulation distribution. Make sure to fill out the necessary income details for the previous five taxable years.

After filling out all sections, review the form for accuracy. Make sure to attach it to the beneficiary's tax return before submission. This will ensure compliance with California tax regulations.

What is the California 5870A form?

The California 5870A form is used to report tax on accumulation distributions from trusts. If you are a beneficiary who has received distributions from a trust, you will need to attach this form to your tax return. It helps determine the tax liability on amounts that have been accumulated in the trust and distributed to you.

Who needs to file the 5870A form?

If you are a beneficiary of a trust and received accumulation distributions during the taxable year, you must file the 5870A form. This applies regardless of whether the distributions were made before or after you were born or reached the age of 21.

What information do I need to complete the form?

You will need several pieces of information to fill out the California 5870A form:

How do I calculate the tax on accumulation distributions?

The tax calculation involves several steps. You will need to determine the average income from previous taxable years, subtract any tax-exempt interest, and then apply the appropriate tax rates. Each section of the form guides you through the calculations, ensuring you account for all relevant factors.

Are there any penalties for not filing the 5870A form?

Failing to file the 5870A form when required can lead to penalties and interest on any unpaid taxes. It's essential to file accurately and on time to avoid complications with the California Franchise Tax Board.

Where can I get help with the California 5870A form?

If you have questions or need assistance, you can refer to the instructions provided with the form. Additionally, consulting a tax professional can help clarify any uncertainties and ensure that you complete the form correctly.

Filling out the California 5870A form can be challenging. Many individuals make common mistakes that can lead to issues with their tax returns. One frequent error is not providing the correct Social Security Number (SSN) or Individual Taxpayer Identification Number (ITIN). This information is crucial for identifying the beneficiary and ensuring accurate processing. Missing or incorrect SSNs or ITINs can delay the tax return and create complications.

Another mistake is failing to include the trust's Federal Employer Identification Number (FEIN). This number is essential for tax purposes and helps the state track the trust's income and distributions. Omitting the FEIN can lead to confusion and potential penalties.

Some individuals also overlook the importance of accurately reporting the beneficiary's date of birth. This date can affect tax calculations, especially in relation to distributions received before the beneficiary turned 21. Providing an incorrect date can lead to miscalculations in the tax owed.

Additionally, many people forget to enter the number of trusts from which they received accumulation distributions. This number is necessary for determining the tax liability accurately. Without this information, the form may be deemed incomplete, leading to further inquiries from tax authorities.

In Section A, errors often occur when calculating the average income and determining the computation years. For instance, miscalculating the amounts from Schedule J can result in incorrect tax calculations. It's vital to ensure that each line is filled out correctly, as even small errors can compound into larger issues.

Another common oversight is failing to eliminate the highest and lowest taxable income years when reporting income from previous years. This step is crucial for an accurate tax computation. Neglecting this requirement can lead to an inflated tax amount.

People sometimes also forget to attach required schedules, such as the tax credit adjustment schedule. Missing attachments can result in delays or rejections of the tax return, causing unnecessary stress for the taxpayer.

Lastly, individuals often misinterpret the instructions regarding the alternative minimum tax adjustments. This can lead to incorrect calculations and potential penalties. Understanding these adjustments is essential for compliance and accurate reporting.

By being aware of these common mistakes, individuals can approach the California 5870A form with greater confidence and accuracy. Careful attention to detail can help ensure a smoother tax filing process.

The California 5870A form is a critical document for beneficiaries of trusts, particularly when dealing with accumulation distributions. However, several other forms and documents often accompany it, providing essential information for tax purposes. Below is a list of these related forms, each serving a specific role in the overall process.

Understanding these forms and their interconnections can greatly simplify the process of filing taxes related to trust distributions. Each document plays a vital role in ensuring compliance and accuracy, ultimately benefiting the beneficiaries involved.

When filling out the California 5870A form, it’s essential to be thorough and accurate. Here’s a helpful list of dos and don’ts to guide you through the process.

This form applies to all trusts that have accumulated income, regardless of where they were established. If the trust has beneficiaries in California, the form must be completed and submitted as part of their tax returns.

While tax professionals can provide valuable assistance, individuals can also complete the form. Clear instructions accompany the form, making it accessible for those willing to invest time in understanding the requirements.

Even if no distributions have been made, the form may still be necessary. It addresses accumulated income, which can impact tax obligations. Beneficiaries should be aware of any accumulation, as it may affect their tax situation.

Filing this form does not guarantee a refund. It is designed to calculate tax liabilities on accumulated income. The actual tax outcome will depend on various factors, including the overall income and deductions of the beneficiaries.

The California 5870A form is used to report accumulation distributions from trusts. It must be attached to the beneficiary's tax return.

When filling out the form, ensure that you provide accurate information regarding the trust, including its name, address, and federal employer identification number (FEIN).

It is important to note the taxable year for which you are filing, as well as the beneficiary's date of birth, which may impact tax calculations.

Sections A and B of the form require different calculations based on the accumulation period of the income. Be sure to follow the instructions closely to determine which section applies to your situation.

Finally, review the completed form for accuracy before submission. Mistakes can lead to delays or issues with tax processing.