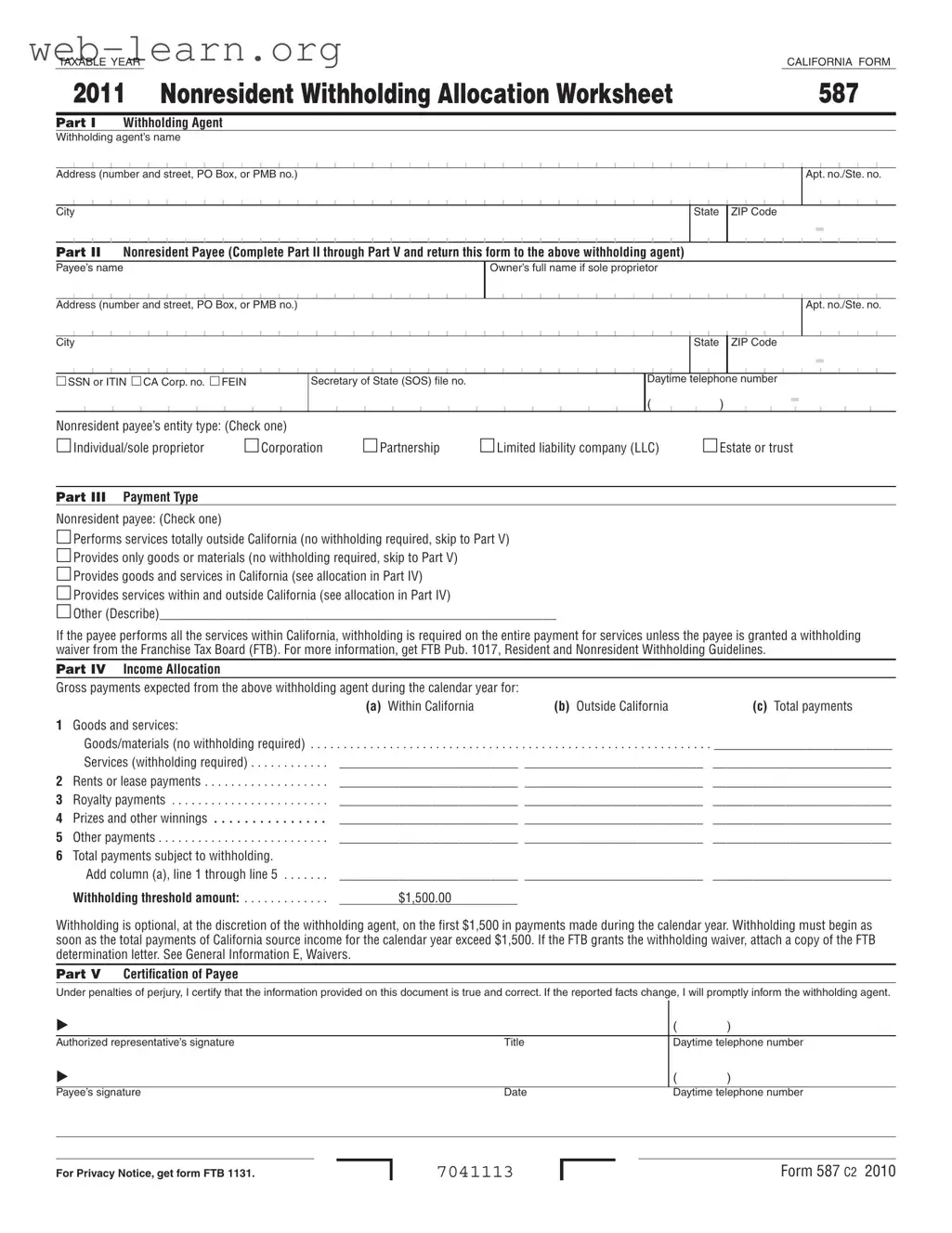

Understanding the California Form 587, also known as the Nonresident Withholding Allocation Worksheet, is essential for anyone involved in payments to nonresidents for services performed within the state. This form plays a crucial role in determining how much tax needs to be withheld from such payments. When a nonresident payee, whether an individual or a business entity, earns income from California sources, the withholding agent must use this form to assess the appropriate withholding amount. The form is divided into several parts, beginning with the details of the withholding agent and the nonresident payee, including their names and addresses. It also categorizes the type of payment being made, whether for services, goods, or other income types. Importantly, the form outlines specific guidelines regarding when withholding is required, with a threshold of $1,500 before mandatory withholding kicks in. Moreover, it includes sections for income allocation, allowing payees to specify the amounts earned both within and outside California. By completing and returning this form, nonresidents can ensure compliance with California tax laws while withholding agents can fulfill their obligations effectively. Keeping accurate records of this form is vital, as it must be retained for a minimum of four years and provided to the Franchise Tax Board upon request.

| Fact Name | Details |

|---|---|

| Purpose | Form 587 is used to determine the withholding amount required on payments made to nonresidents for services performed in California. |

| Governing Law | The form is governed by the California Revenue and Taxation Code (R&TC) Section 18662. |

| Withholding Rate | The standard withholding rate is 7% on payments made to nonresidents for California source income. |

| Threshold for Withholding | No withholding is required if total payments to the nonresident are $1,500 or less during the calendar year. |

| Filing Requirement | The withholding agent must request Form 587 to be completed and returned before payment is made to the nonresident payee. |

| Certification | The payee must certify that the information provided on Form 587 is true and correct, signing under penalties of perjury. |

| Waivers | A nonresident payee can request a waiver for withholding using Form 588, and must attach the waiver letter if granted. |

| Retention Period | The withholding agent must retain Form 587 for a minimum of four years and provide it to the Franchise Tax Board upon request. |

Completing the California Form 587 is a straightforward process. This form is essential for nonresidents to report their withholding allocations correctly. After filling it out, return it to the withholding agent, who will use the information to determine the appropriate withholding amounts.

California Form 587, known as the Nonresident Withholding Allocation Worksheet, is designed to determine the amount of withholding required on payments made to nonresidents. It is crucial for ensuring compliance with California tax regulations regarding income earned by nonresidents for services performed or other income sourced within the state.

The form must be completed by the nonresident payee receiving payments from a withholding agent. This includes individuals, corporations, partnerships, limited liability companies (LLCs), estates, and trusts that are not residents of California. The withholding agent must also fill out Part I of the form before providing it to the payee.

Form 587 should be completed and submitted by the payee to the withholding agent at the time a contract is established or before any payment is made. The withholding agent is required to retain this form for a minimum of four years and must provide it to the Franchise Tax Board (FTB) upon request.

Payments made to nonresidents for services performed in California, rents for property located in California, royalties, and certain other payments are subject to withholding. However, if the total payments to the nonresident during the calendar year do not exceed $1,500, withholding is not required.

A nonresident payee can request a waiver from withholding by submitting Form 588, the Nonresident Withholding Waiver Request. If granted, a copy of the FTB's determination letter must be attached to Form 587 when submitted to the withholding agent.

Should there be any changes in the information provided on Form 587, the payee is obligated to promptly notify the withholding agent. This ensures that the withholding agent has the most accurate and up-to-date information for tax compliance.

If a payee fails to provide a valid TIN, they may be denied the backup withholding credit. It is essential for the payee to contact the FTB to provide a valid TIN before filing a tax return to avoid complications.

Filling out the California Form 587 can be straightforward, but several common mistakes can lead to delays or complications. One frequent error is failing to provide all required information in Part II. This section requires detailed information about the nonresident payee, including their full name and taxpayer identification number. Omitting any of this information can result in processing delays.

Another common mistake is not checking the correct box in Part III regarding the type of payment. The payee must accurately indicate whether they perform services entirely outside California or provide goods and services within the state. Misclassification can lead to incorrect withholding calculations.

In Part IV, some individuals forget to allocate income properly. It is essential to distinguish between payments made for services rendered within California and those made for services outside the state. This allocation affects the withholding amount. Failure to provide accurate figures can lead to over- or under-withholding.

Additionally, many payees overlook the withholding threshold amount of $1,500. If total payments exceed this amount, withholding is mandatory. Not being aware of this requirement can lead to unexpected tax liabilities.

Another mistake occurs when individuals neglect to sign the certification in Part V. Both the payee and any authorized representative must sign and date the form. Without signatures, the form is incomplete and cannot be processed.

Some people also fail to update the withholding agent if their circumstances change after submitting the form. If there are any changes in the facts reported, the payee is obligated to inform the withholding agent promptly. Ignoring this responsibility can create issues down the line.

Lastly, many individuals do not keep a copy of the completed Form 587 for their records. It is important to retain this document for at least four years, as it may be needed for future reference or in case of an audit.

By being aware of these common mistakes, payees can fill out the California Form 587 more accurately and avoid potential complications. Attention to detail is key in ensuring compliance with state tax requirements.

The California Form 587, known as the Nonresident Withholding Allocation Worksheet, is essential for determining withholding requirements on payments made to nonresidents. In conjunction with this form, several other documents are commonly utilized to ensure compliance with California tax regulations. Below is a list of documents that often accompany Form 587, each serving a specific purpose in the withholding process.

Each of these forms and documents plays a vital role in the withholding process for nonresidents in California. Understanding their purposes can help ensure compliance with state tax laws and avoid potential penalties. Proper documentation is crucial for both withholding agents and payees to navigate the complexities of California's tax regulations effectively.

When filling out the California 587 form, there are several key do's and don'ts to keep in mind. Here’s a helpful list:

Understanding the California Form 587 can be challenging due to various misconceptions. Here are eight common misunderstandings about this form, along with clarifications:

In reality, Form 587 is required for various entity types, including corporations, partnerships, and limited liability companies (LLCs), not just individuals.

Withholding is only required when total payments exceed $1,500 during the calendar year. Payments below this threshold do not require withholding.

This is incorrect. Payments for goods or services performed entirely outside California do not require withholding.

The withholding agent must complete Part I of the form and ensure that it is filled out correctly before returning it to the payee.

Payees must inform the withholding agent of any changes to the information provided on Form 587 promptly.

Form 587 is specifically designed for nonresidents receiving payments for services performed in California.

To request a waiver, payees must complete Form 588 and submit it to the Franchise Tax Board (FTB). A formal process is necessary.

Even if withholding is waived or the payee is exempt, they are still required to file a California tax return and pay any taxes owed.

When dealing with the California Form 587, Nonresident Withholding Allocation Worksheet, it's essential to understand its purpose and requirements. Here are five key takeaways:

Understanding these key points can help ensure compliance and avoid potential issues related to nonresident withholding in California.