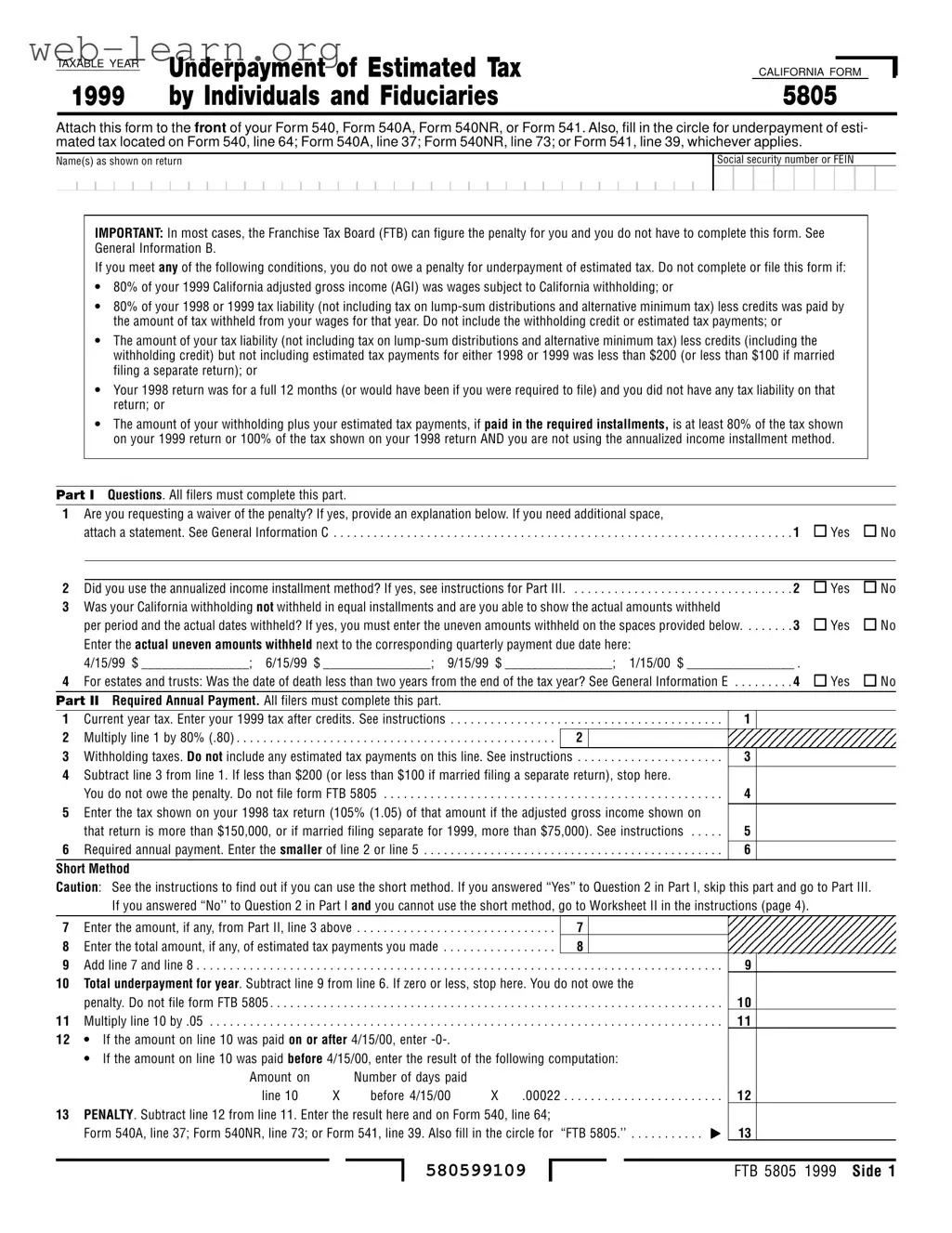

The California Form 5805 is an essential document for individuals and fiduciaries who may face penalties for underpaying their estimated taxes. This form is specifically designed to help taxpayers determine whether they owe a penalty and, if so, to calculate the amount due. When filing your California income tax return, you must attach Form 5805 to the front of your Form 540, Form 540A, Form 540NR, or Form 541. It is important to note that in many cases, the Franchise Tax Board (FTB) will automatically calculate any penalties, so completing this form may not be necessary for everyone. However, there are specific conditions under which you must fill it out, such as if your withholding was not done in equal installments or if you are requesting a waiver of the penalty. The form includes sections that require you to provide your personal information, answer key questions about your tax situation, and calculate your required annual payment based on your tax liability. By understanding the major components of Form 5805, taxpayers can navigate their obligations more effectively and ensure compliance with California tax regulations.

| Fact Name | Description |

|---|---|

| Purpose | The California Form 5805 is used to determine if an individual or fiduciary owes a penalty for underpaying estimated taxes for the tax year 1999. |

| Filing Requirement | This form must be attached to the front of Form 540, Form 540A, Form 540NR, or Form 541 if the filer meets certain conditions that may result in a penalty. |

| Conditions for No Penalty | No penalty is owed if specific criteria are met, such as having 80% of income from wages subject to withholding or if the tax liability is below $200. |

| Waiver of Penalty | Filers can request a waiver of the penalty for reasons such as retirement after age 62 or underpayment due to a disaster. This request must be documented on the form. |

| Governing Law | The form is governed by California Revenue and Taxation Code Section 19132, which outlines penalties for underpayment of estimated tax. |

Completing the California Form 5805 requires careful attention to detail. This form is essential for determining any penalties related to underpayment of estimated taxes. Follow the steps outlined below to ensure accuracy in filling out the form.

After completing these steps, ensure that you file your tax return by the due date to avoid additional penalties. Keep a copy of the completed form for your records.

The California Form 5805 is used to determine if you owe a penalty for underpaying your estimated tax. If you do owe a penalty, this form helps calculate the amount. It is important to attach this form to the front of your tax return, such as Form 540, Form 540A, Form 540NR, or Form 541.

Most taxpayers do not need to complete this form, as the Franchise Tax Board (FTB) can calculate any penalties for you. However, if you meet specific conditions, such as having uneven withholding or being an estate or trust, you must complete and file this form.

You may not owe a penalty if:

If you believe you qualify for a waiver, check "Yes" on Part I of Form 5805 and provide an explanation. You may attach a statement if you need more space. Complete the form through Part II, and indicate the amount you wish to waive.

If your California withholding was not withheld in equal installments, you must indicate the actual amounts withheld and their corresponding dates on Part I, Question 3 of the form. This information is crucial for accurately calculating your penalty.

This method is beneficial if your income varied throughout the year. It allows you to calculate your required estimated tax payments based on your actual income as it was earned. If you choose this method, you must complete Part III of Form 5805.

If you are a calendar year taxpayer, the due dates for 1999 estimated tax installments were:

The penalty is calculated based on the amount of underpayment and the number of days it remained unpaid. Different rates apply depending on the time period during which the underpayment occurred. The FTB provides the applicable rates for each period.

If you file an amended return, you must use the amounts from your original return to calculate the penalty if the amended return is filed after the original due date. If filed on or before the due date, you can use the amended amounts.

Completing the California Form 5805 can be a daunting task, and many individuals make common mistakes that can lead to penalties or complications. One frequent error is failing to determine whether the form is actually necessary. In many cases, the Franchise Tax Board (FTB) can calculate the penalty for underpayment on behalf of the taxpayer. If certain conditions are met, individuals may not owe a penalty and should not complete the form. Always check the criteria outlined in the instructions to see if you qualify for exemption.

Another common mistake involves incorrect calculations on the form itself. Taxpayers often miscalculate their required annual payment by not accurately entering their tax liability or withholding amounts. For example, if you do not properly account for all tax credits or fail to include the correct amounts from your previous year’s return, your figures will be off. Double-check all calculations to ensure accuracy, as even small errors can lead to significant penalties.

Many individuals also neglect to complete all necessary parts of the form. Part I requires specific questions to be answered, and skipping any of these can result in an incomplete submission. For instance, if you answer "Yes" to requesting a waiver of the penalty, you must provide an explanation. Failing to do so may lead the FTB to reject your request, resulting in an automatic penalty.

Additionally, taxpayers often forget to attach the completed Form 5805 to the front of their tax return. This is a crucial step that should not be overlooked. Without the proper attachment, the FTB may not consider your submission valid, and you could face penalties for underpayment. Always ensure that your form is securely attached to your main return before filing.

Finally, many individuals overlook the importance of timely filing. If you file your return late, even if you have completed the form correctly, you may still incur penalties. It is essential to be aware of filing deadlines and to submit your tax return, along with Form 5805 if applicable, on time to avoid unnecessary charges. By being diligent and thorough in your preparation, you can navigate this process more smoothly and reduce the risk of penalties.

The California Form 5805 is an important document used to determine if individuals and fiduciaries owe a penalty for underpaying estimated taxes. Alongside this form, several other documents are often required to ensure accurate tax reporting and compliance. Below is a list of related forms and documents that may be used in conjunction with the California 5805.

Using these forms correctly is crucial for compliance with California tax laws. Ensure that all necessary documents are completed accurately and submitted on time to avoid penalties and interest charges. Staying informed and organized will help streamline the tax filing process.

When filling out the California 5805 form, follow these guidelines to ensure accuracy and compliance.

Misconceptions about the California 5805 form can lead to confusion regarding tax obligations. Below are nine common misconceptions along with clarifications.

Understanding these misconceptions can help taxpayers navigate their responsibilities more effectively and avoid unnecessary penalties.

The California Form 5805 is used to determine if you owe a penalty for underpaying estimated taxes.

Attach this form to the front of your tax return, such as Form 540, 540A, 540NR, or 541.

Before filling out the form, check if the Franchise Tax Board (FTB) can calculate the penalty for you. In many cases, they will do so automatically.

You do not need to file the form if certain conditions are met, such as having 80% of your income from wages subject to California withholding.

All filers must complete Part I of the form, which includes questions about your tax situation.

If you request a waiver for the penalty, provide a clear explanation on the form.

Part II requires you to calculate your required annual payment based on your current year tax and withholding.

If your income fluctuated throughout the year, consider using the annualized income installment method detailed in Part III.

Make sure to fill in the appropriate circles on your main tax form to indicate you are submitting Form 5805.