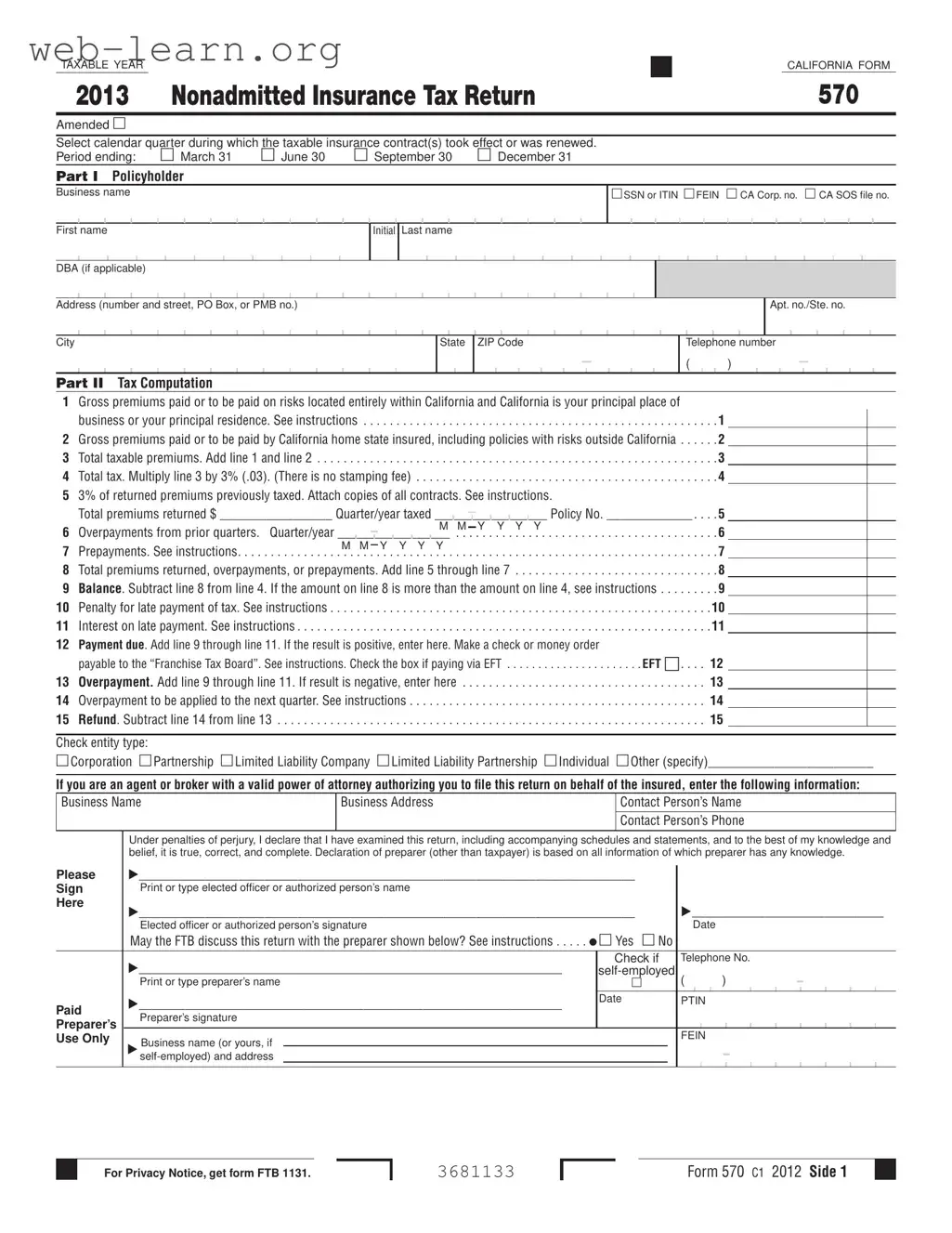

The California Form 570 is a crucial document for individuals and businesses involved in nonadmitted insurance transactions within the state. This form serves as the Nonadmitted Insurance Tax Return, enabling policyholders to report and calculate taxes on premiums associated with nonadmitted insurance contracts. The form requires users to specify the taxable year and select the relevant calendar quarter during which the insurance contracts took effect or were renewed. Key sections of the form include details about the policyholder, such as business name, address, and identification numbers. Additionally, it outlines the tax computation process, where gross premiums are reported and the applicable tax rate of three percent is applied. The form also provides space for reporting any returned premiums, overpayments, or prepayments, ensuring that policyholders can accurately manage their tax obligations. Completing Form 570 is essential for compliance, as it not only determines the tax due but also serves as a mechanism for claiming refunds or addressing amendments to previously filed returns.

| Fact Name | Description |

|---|---|

| Purpose of Form 570 | The California Form 570 is used to report and calculate the Nonadmitted Insurance Tax on premiums paid to nonadmitted insurers for contracts covering risks. |

| Tax Rate | The tax rate imposed on the gross premiums is three percent (3%). This rate applies to premiums paid for policies covering risks located within the United States. |

| Filing Frequency | Taxpayers may need to file up to four Form 570 returns in a single year, corresponding to each calendar quarter in which a nonadmitted insurance contract is purchased or renewed. |

| Governing Laws | The form is governed by the California Revenue and Taxation Code and the California Insurance Code, specifically Assembly Bill (AB) 315 and the Nonadmitted and Reinsurance Reform Act (NRRA). |

| Amended Returns | Taxpayers can file an amended Form 570 to correct errors or claim refunds. This must be done within four years of the original due date or one year from the date of overpayment. |

Filling out the California Form 570 is essential for reporting nonadmitted insurance tax. Once you have completed the form, ensure that you submit it by the deadline specified for the relevant calendar quarter. This will help you avoid penalties and ensure compliance with state tax regulations.

What is the California 570 Form?

The California 570 Form is used to report and pay taxes on nonadmitted insurance premiums. This form helps determine the tax owed on premiums paid or to be paid for insurance contracts covering risks. It is important for individuals and businesses that purchase nonadmitted insurance in California.

Who needs to file the California 570 Form?

Anyone who is a home state insured and purchases or renews a nonadmitted insurance contract must file this form. A home state insured is someone whose principal place of business or residence is in California.

When is the California 570 Form due?

The form is due on the first day of the third month following the end of each calendar quarter in which the insurance contract took effect or was renewed. For example, if a contract starts in January, February, or March, the form is due by June 1.

What is the tax rate for nonadmitted insurance premiums?

The tax rate is 3% of the gross premiums paid or to be paid. This rate applies to all taxable premiums, excluding any stamping fees.

What information do I need to provide on the form?

You will need to enter your business name, address, identification number, and the gross premiums paid. You must also report any returned premiums or overpayments from previous quarters.

Can I amend my California 570 Form?

Yes, you can file an amended return if you need to correct an error or claim a refund. Simply check the "Amended" box at the top of the form and attach a copy of the original return.

What happens if I miss the filing deadline?

If you file late, you may incur a penalty of 10% of the tax due. Additionally, interest will be charged on any unpaid amounts from the due date until paid.

How do I make a payment for the tax due?

You can make a payment by check or money order made out to the "Franchise Tax Board." If you prefer, you can also pay electronically using Electronic Funds Transfer (EFT).

What if I have questions about the form?

If you have any questions, you can contact the FTB Nonadmitted Insurance Desk at 916.845.7448. They can provide assistance regarding the form and the filing process.

Where do I send the completed California 570 Form?

Mail the completed form and payment to:

FRANCHISE TAX BOARD

PO BOX 942867

SACRAMENTO CA 94267-0651

Filling out the California Form 570 can be a straightforward process, but several common mistakes can lead to complications. One significant error is neglecting to select the correct calendar quarter for the taxable insurance contracts. Each quarter has specific deadlines and requirements, so choosing the wrong one can result in delays or penalties.

Another frequent mistake involves incorrect entries in the policyholder information section. Providing inaccurate names, addresses, or identification numbers can create issues with processing the return. It is crucial to ensure that all details are entered accurately, as discrepancies may lead to further inquiries from the Franchise Tax Board.

Many individuals fail to report all gross premiums accurately. Line 1 and Line 2 must reflect the total premiums paid or to be paid on risks located entirely within California and those from California home state insured policies, respectively. Omitting or miscalculating these amounts can lead to an incorrect tax computation.

Another common oversight is rounding amounts. The instructions specify that individuals should not round cents to the nearest dollar. Entering amounts with cents is essential for accurate calculations, yet many people overlook this detail, which can affect the total tax owed.

In addition, some filers mistakenly fail to attach required documentation, especially when claiming returned premiums or overpayments. Line 5 requires copies of all contracts related to returned premiums. Without this documentation, the return may be rejected or delayed.

Another mistake involves the calculation of penalties and interest for late payments. Individuals often underestimate these charges or fail to include them in their total payment due. Understanding how to calculate these amounts accurately is essential to avoid additional fees.

Some individuals also neglect to check the box indicating whether they wish to allow the Franchise Tax Board to discuss the return with their preparer. This can complicate communication if questions arise during processing. It is advisable to make this choice clear to facilitate any necessary follow-up.

Finally, failing to sign and date the form is a common but critical mistake. The declaration at the end of the form requires a signature to validate the information provided. Without a signature, the return may be considered incomplete, leading to potential penalties or processing delays.

The California 570 form, used for reporting nonadmitted insurance tax, is often accompanied by several other forms and documents that help provide a complete picture of the tax obligations. Below are four commonly used documents that can be relevant when filing the 570 form.

Understanding these accompanying forms and documents can simplify the filing process and ensure compliance with California tax regulations. Proper documentation not only supports accurate reporting but also helps in addressing any potential issues that may arise during the review of the tax return.

The California Form 570, Nonadmitted Insurance Tax Return, shares similarities with several other tax-related documents. Here is a list of eight documents that resemble the California 570 form:

When completing the California 570 form, there are several important guidelines to follow. Below is a list of things to do and avoid to ensure accurate and timely submission.

This form applies to any individual or entity that purchases nonadmitted insurance, regardless of size. Small businesses and individuals may also need to file.

Anyone classified as a California home state insured, which can include out-of-state residents with certain insurance policies, must file.

The tax rate is fixed at 3% of the gross premium paid or to be paid, with no additional fees.

The form must be filed by the first day of the third month following the close of each calendar quarter.

Returned premiums must be reported on the form, specifically in line 5, to adjust the taxable amount.

Filing an amended return is straightforward. Just check the "Amended" box and attach the original return.

It is essential to maintain records of all policies, as they must be reported on the form and may be required for verification.

Currently, the California 570 form must be mailed in; electronic submission is not available.

Late payments incur a penalty of 10% of the tax due, in addition to interest on the unpaid amount.

The form applies to all nonadmitted insurance contracts, covering various types of risks, as long as the insured is classified as a California home state insured.

The California Form 570 is used to report and calculate the Nonadmitted Insurance Tax on premiums paid to nonadmitted insurers. This tax applies to contracts covering risks located entirely within California.

It's essential to accurately complete all sections of the form, including the policyholder's information, tax computation, and details about insurance contracts. Clear and legible entries are crucial.

The tax rate for this form is 3% of the gross premiums paid or to be paid, excluding any stamping fees. Be sure to include only premiums related to risks within the U.S.

Form 570 must be filed by the first day of the third month following the close of any calendar quarter in which the insurance contract took effect or was renewed. Missing this deadline can result in penalties.

If an error is found on the original return, an amended return can be filed using Form 570. This must be done within four years of the original due date or one year from the date of overpayment.

When filling out the form, avoid rounding cents to the nearest dollar. Always report amounts in full, including cents, to ensure accurate tax calculations.