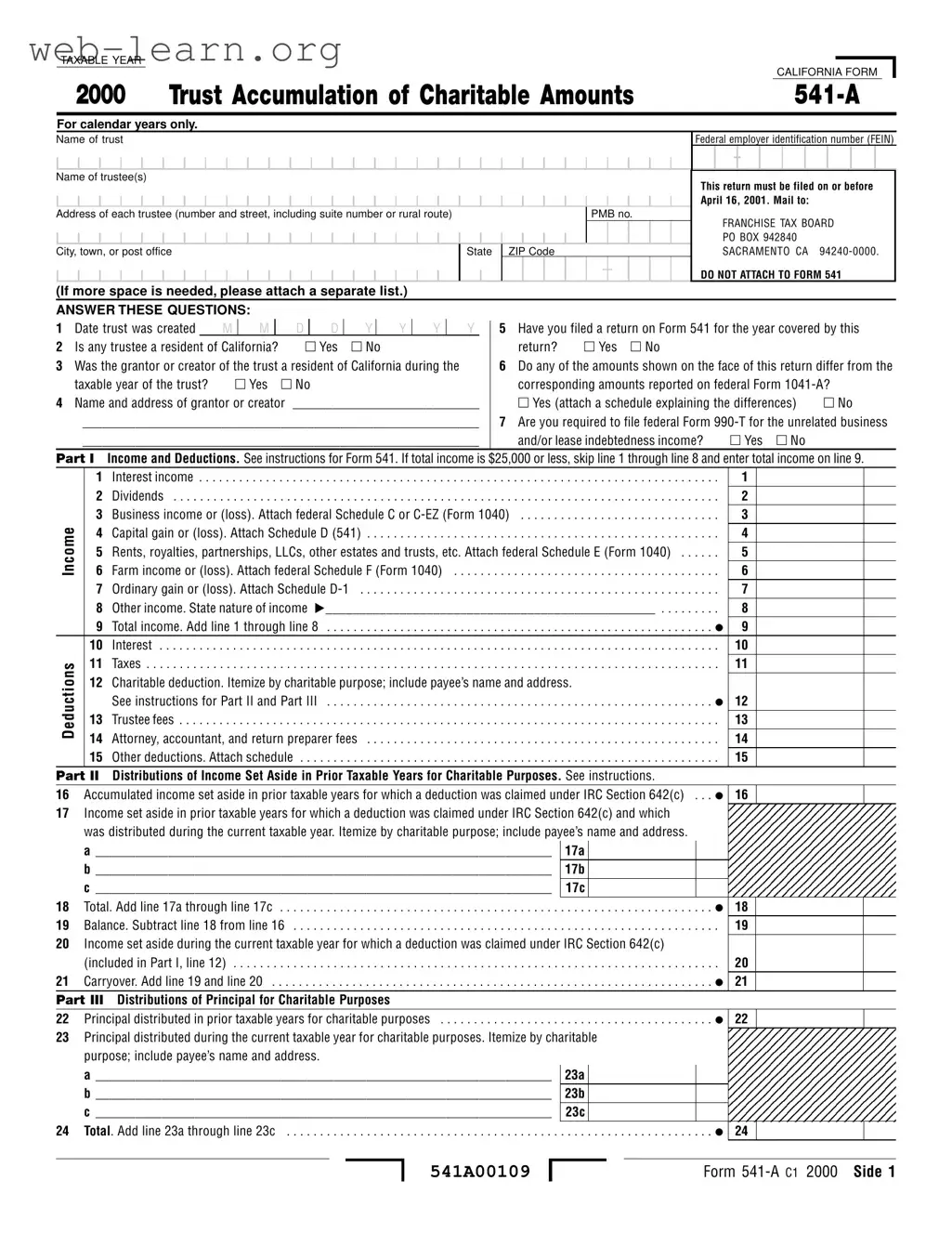

The California 541 A form is a tax document used by trustees to report charitable amounts accumulated in a trust. This form is specifically designed for trusts that claim deductions for charitable contributions under federal tax law. It requires the name of the trust, the federal employer identification number, and details about the trustee or trustees. The form includes sections for reporting income and deductions, as well as distributions made for charitable purposes. It also asks important questions about the trust's creation date, residency of trustees, and whether any discrepancies exist between the amounts reported on this form and federal forms. The 541 A form must be filed by April 16 of the following year, and it is essential for trustees to provide accurate information to comply with California tax regulations. Additional instructions guide trustees on how to detail distributions and reconcile any differences in financial records.

| Fact Name | Details |

|---|---|

| Form Purpose | The California Form 541-A is used to report the accumulation of charitable amounts by a trust for a calendar year. |

| Governing Law | This form is governed by the California Revenue and Taxation Code, specifically Section 18635. |

| Filing Deadline | Form 541-A must be filed on or before April 16, 2001. Extensions are available without a request form. |

| Who Must File | Trustees of charitable or split-interest trusts that claim deductions under IRC Section 642(c) must file this form. |

| Residency Requirement | If any trustee is a resident of California, they must complete the form, indicating the residency status. |

| Income Threshold | If total income is $25,000 or less, the trustee can skip several lines and directly report total income on line 9. |

| Mailing Address | Completed forms should be mailed to the Franchise Tax Board at PO Box 942840, Sacramento, CA 94240-0000. |

Filling out the California 541 A form can seem daunting, but with a clear understanding of the steps involved, it becomes manageable. This form is specifically designed for trusts that accumulate charitable amounts, and it requires precise information to ensure compliance with California tax regulations. Below are the steps to guide you through the process of completing this form.

Once completed, mail the form to the Franchise Tax Board at the address provided. Make sure to keep a copy for your records. If you need more time, remember that California grants an automatic six-month extension without needing to file a request form. This can provide peace of mind as you finalize your submission.

What is the purpose of California Form 541-A?

California Form 541-A is used to report the charitable information required by the Revenue and Taxation Code Section 18635. This form is specifically for trusts that claim a charitable deduction under IRC Section 642(c) or for charitable and split-interest trusts. The form helps ensure compliance with California tax law regarding charitable distributions.

Who is required to file Form 541-A?

A trustee must file Form 541-A for a trust that claims a charitable deduction under IRC Section 642(c) or for a charitable or split-interest trust. However, if the governing instrument requires the trustee to distribute all income for the taxable year, then filing is not necessary. This applies to charitable trusts that are not exempt from taxation under R&TC Section 23701d.

When is Form 541-A due?

Form 541-A must be filed on or before April 16, 2001. If more time is needed, California allows for an automatic six-month extension without the need for a request form. It’s important to ensure timely filing to avoid potential penalties.

Where should I mail Form 541-A?

Mail Form 541-A to the Franchise Tax Board at the following address:

FRANCHISE TAX BOARD

PO BOX 942840

SACRAMENTO CA 94240-0000

What information is required about the trust on Form 541-A?

The form requires several key pieces of information, including:

What if my trust has a taxable year different from the calendar year?

If the trust’s taxable year differs from the calendar year, you must indicate this on the form. Any discrepancies between the amounts reported on Form 541-A and the corresponding federal Form 1041-A must be explained in an attached schedule.

How do I report income and deductions on Form 541-A?

Income and deductions are reported in Part I of the form. If the total income is $25,000 or less, you can skip lines 1 through 8 and simply enter the total income on line 9. Various types of income, such as interest, dividends, and business income, need to be itemized accordingly.

What kind of charitable distributions need to be reported?

In Parts II and III, you must report distributions of income set aside in prior taxable years for charitable purposes, as well as distributions of principal for charitable purposes. It’s essential to provide detailed descriptions of these distributions, including the purpose and the recipient’s information.

What should I do if my balance sheet does not agree with my books of account?

If there are discrepancies between the balance sheet and the books of account, you must reconcile these differences in an attached statement. This ensures transparency and accuracy in your reporting.

What penalties might I face for failing to file Form 541-A on time?

Failure to file Form 541-A by the due date may result in penalties. These can include late filing fees and interest on any taxes owed. To avoid such consequences, it’s crucial to adhere to the filing deadlines and requirements outlined by the Franchise Tax Board.

Filling out the California Form 541-A can be a complex task, and many individuals make common mistakes that can lead to confusion or delays. One frequent error is failing to provide complete and accurate trustee information. The form requires the name, address, and federal employer identification number (FEIN) of each trustee. Incomplete information can result in processing delays or even rejection of the form.

Another mistake involves misunderstanding the filing requirements. Some trustees may overlook the necessity of filing if the trust is required to distribute all income for the year. If this requirement is not met, the trustee must file Form 541-A. Ignoring this crucial detail can lead to penalties or issues with the Franchise Tax Board.

Many individuals also neglect to check the residency status of the trustee and grantor. The form asks whether any trustee is a resident of California and whether the grantor was a resident during the taxable year. Incorrectly answering these questions can lead to misclassification of the trust, impacting tax obligations.

Moreover, mistakes often occur in reporting income and deductions. Some trustees may skip lines or miscalculate totals, particularly when the total income is $25,000 or less. This oversight can lead to inaccurate reporting, which may trigger audits or additional scrutiny from tax authorities.

Another common error is failing to reconcile discrepancies between California and federal tax law. California has not conformed to many changes made to the Internal Revenue Code, and trustees must be aware of these differences. Not addressing these discrepancies can lead to incorrect filings and potential penalties.

Trustees sometimes overlook the importance of itemizing charitable deductions. The form requires detailed information about charitable contributions, including the payee’s name and address. Failing to provide this information can result in disallowance of the deduction, affecting the trust's overall tax liability.

Lastly, many trustees forget to sign and date the form. The declaration of perjury at the bottom of the form emphasizes the importance of accuracy and honesty in reporting. A missing signature can lead to the form being considered incomplete, resulting in further delays and complications.

The California Form 541-A is used for reporting the accumulation of charitable amounts by a trust. When filing this form, there are several other documents that may be required or helpful to include. Below is a list of these forms and documents, along with brief descriptions of each.

These forms and documents collectively help ensure compliance with both California and federal tax laws. They provide necessary details about the trust's income, deductions, and charitable activities. Properly preparing and submitting these documents can help facilitate a smoother filing process and avoid potential issues with tax authorities.

The California Form 541-A is primarily used for reporting the accumulation of charitable amounts by trusts. It has similarities with several other tax-related documents, each serving specific purposes. Below is a list of documents that share characteristics with Form 541-A:

When filling out the California 541 A form, it’s important to follow certain guidelines to ensure accuracy and compliance. Here’s a list of things you should and shouldn’t do:

Misconception 1: The California 541 A form is only for large trusts.

This form is required for any trust claiming a charitable deduction, regardless of its size. Even smaller trusts must file if they meet certain criteria.

Misconception 2: You can file the 541 A form at any time during the year.

The form must be filed by April 16 of the following year. Timely filing is crucial to avoid penalties.

Misconception 3: You don't need to file if the trust is exempt from taxes.

Even if a trust is exempt, it may still need to file if it claims deductions under IRC Section 642(c).

Misconception 4: The 541 A form is the same as the federal Form 1041-A.

While they share similarities, there are significant differences due to California's tax laws. It's important to understand both forms separately.

Misconception 5: All trustees must be California residents to file the 541 A form.

Only if any trustee is a California resident does it affect the filing requirements. Non-resident trustees can still file the form.

Misconception 6: You can skip filing if the trust has no income.

If the trust is claiming charitable deductions, it still needs to file, even if it reports no income.

Misconception 7: Filing the 541 A form is optional if the trust distributes all income.

Trusts that distribute all income might not need to file, but they must confirm this based on the governing instrument and local laws.

Misconception 8: The 541 A form is only for charitable trusts.

While primarily for charitable trusts, split-interest trusts also need to file this form if they claim deductions.