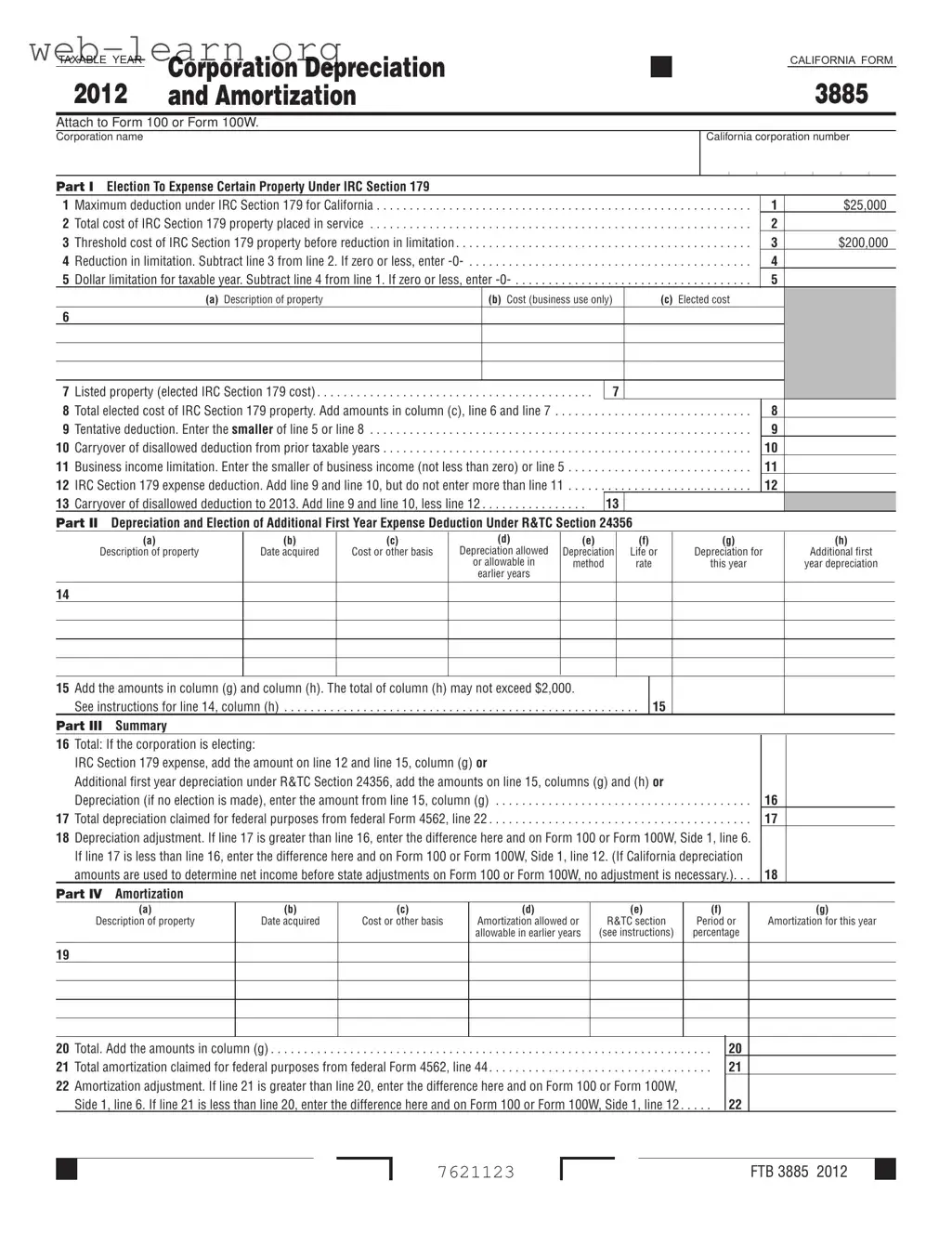

The California Form 3885 is a crucial document for corporations, partnerships, and limited liability companies (LLCs) classified as corporations, as it facilitates the calculation of depreciation and amortization deductions. This form is essential for reporting on the election to expense certain property under IRC Section 179, which allows a corporation to deduct a portion of the cost of qualifying property in the year it is placed in service. The maximum deduction under this section for California is set at $25,000, with specific thresholds and limitations based on the total cost of the property. Additionally, Form 3885 includes sections for detailing depreciation methods, such as straight-line and declining balance, and allows for the election of additional first-year expense deductions. It also addresses amortization for intangible assets over a fixed period, typically 15 years, aligning with California’s Revenue and Taxation Code. Understanding the nuances of this form is vital for accurate tax reporting and compliance, particularly given the differences between California and federal tax laws.

| Fact Name | Fact Description |

|---|---|

| Form Purpose | The California Form 3885 is used to calculate depreciation and amortization deductions for corporations. |

| Governing Laws | This form is governed by the California Revenue and Taxation Code (R&TC) and the Internal Revenue Code (IRC). |

| Section 179 Deduction | The maximum deduction allowed under IRC Section 179 for California is $25,000. |

| Threshold Cost | The threshold cost of IRC Section 179 property before reduction is $200,000. |

| Listed Property | Listed property includes passenger automobiles and other assets used for transportation that can also be used personally. |

| Depreciation Methods | California allows various depreciation methods, including straight-line and declining balance methods. |

| Amortization Period | Intangible assets under R&TC Section 197 are amortized on a straight-line basis over 15 years. |

| Federal/State Differences | California law has specific differences from federal law regarding depreciation and amortization calculations. |

Filling out the California 3885 form involves several steps to accurately report depreciation and amortization for your corporation. After completing the form, you will attach it to Form 100 or Form 100W as part of your tax filing. Ensure that all information is accurate to avoid any issues with your submission.

What is California Form 3885?

California Form 3885 is used by corporations to calculate depreciation and amortization deductions. This includes partnerships and limited liability companies (LLCs) classified as corporations. S corporations, however, must use Schedule B (100S) for these calculations. The form helps businesses recover costs associated with their property over time, providing significant tax benefits.

Who needs to file Form 3885?

Any corporation, including partnerships and LLCs treated as corporations, that has depreciable or amortizable property must file Form 3885. If you are an S corporation, you will need to complete Schedule B instead. It's essential to file this form if your business has purchased property that qualifies for depreciation or amortization deductions.

What types of property can be included on Form 3885?

Form 3885 covers both tangible and intangible assets. Tangible assets include office furniture, machinery, and vehicles, while intangible assets may include organizational expenditures and certain types of intellectual property. The form allows businesses to recover costs for property with a determinable useful life of more than one year.

What is the maximum deduction allowed under IRC Section 179 for California?

The maximum deduction allowed under IRC Section 179 for California is $25,000. However, this amount is subject to reduction if the total cost of IRC Section 179 property placed in service during the taxable year exceeds $200,000. Therefore, businesses must carefully track their property costs to determine their eligibility for this deduction.

What is the difference between depreciation and amortization?

Depreciation applies to tangible assets, allowing businesses to recover the cost of property like machinery and vehicles over time. Amortization, on the other hand, pertains to intangible assets, such as patents or trademarks, and spreads the cost over a fixed period. Understanding these distinctions is crucial for accurately completing Form 3885.

How do I determine the depreciation method to use?

Corporations can choose from several depreciation methods, including straight-line, declining balance, and sum-of-the-years-digits. The choice depends on the type of property, its useful life, and whether it is new or used. It's vital to consider these factors to maximize deductions and comply with tax regulations.

Can I elect to expense certain property under IRC Section 179?

Yes, corporations can elect to expense certain property under IRC Section 179, provided the property is placed in service during the taxable year. However, the total deduction cannot exceed the corporation’s business income. This election must be made on a timely filed tax return and cannot be revoked without consent from the Franchise Tax Board.

What happens if I do not file Form 3885?

If you fail to file Form 3885 when required, you may miss out on valuable tax deductions. This could lead to a higher tax liability than necessary. Additionally, not filing could result in penalties or interest charges from the California Franchise Tax Board. Therefore, it is critical to file accurately and on time.

Where can I find more information about Form 3885?

For more detailed information, you can visit the California Franchise Tax Board's website. There, you will find resources, instructions, and guidelines related to Form 3885. It’s essential to stay informed about any updates or changes to tax laws that could affect your filings.

Filling out the California Form 3885 can be a complex task, and mistakes can lead to delays or inaccuracies in tax filings. One common mistake is failing to provide the correct corporation name and number at the top of the form. This information is essential for identifying the business and ensuring that the form is processed correctly. Omitting or misspelling this information can cause significant issues.

Another frequent error occurs in Part I, where taxpayers often miscalculate the maximum deduction under IRC Section 179. It is crucial to remember that the maximum deduction allowed for California is $25,000. If a corporation places more than $200,000 of Section 179 property in service, the deduction may be reduced, and some individuals overlook this threshold, leading to incorrect entries.

Inaccuracies in reporting the total cost of IRC Section 179 property placed in service can also create problems. Taxpayers sometimes forget to include all qualifying assets, which can result in a lower deduction than entitled. Each asset must be accounted for to ensure compliance with tax regulations.

Another mistake involves the elected cost of listed property. Taxpayers may include listed property in the wrong section or fail to apply the correct limits. Listed property, such as passenger vehicles under 6,000 pounds, has specific rules that must be followed. Ignoring these rules can lead to disallowed deductions.

Many individuals also fail to properly calculate the business income limitation. This figure determines the maximum deduction a corporation can claim under Section 179. If the business income is less than the allowable deduction, the corporation cannot claim the full amount, which can be overlooked during the filling process.

In Part II, errors often arise in reporting the depreciation method. Taxpayers sometimes select the wrong method for their assets, such as using the straight-line method when a declining balance method would be more appropriate. Understanding the asset's classification and useful life is essential for accurate reporting.

Another common mistake is failing to include the additional first-year depreciation for qualifying property. This deduction can significantly reduce taxable income, but it must be calculated correctly. Taxpayers may neglect to apply this deduction or miscalculate the amount, leading to missed savings.

In Part IV, taxpayers often misidentify the correct R&TC section for amortization. Each type of amortization has specific regulations, and entering the wrong section can result in incorrect calculations and potential penalties. It is vital to refer to the instructions carefully to ensure compliance.

Finally, many individuals overlook the importance of keeping accurate records of all property placed in service. Documentation is crucial for substantiating claims made on the form. Failing to maintain proper records can lead to challenges during audits or reviews by tax authorities.

In summary, careful attention to detail is required when completing the California Form 3885. By avoiding these common mistakes, taxpayers can ensure a smoother filing process and potentially maximize their deductions.

The California Form 3885 is essential for corporations to calculate their depreciation and amortization deductions. However, several other forms and documents are often used alongside it to ensure compliance with state tax regulations. Here’s a list of these related documents, each serving a unique purpose in the tax preparation process.

Using these forms in conjunction with the California Form 3885 helps corporations navigate the complexities of tax regulations while maximizing their deductions. Understanding the purpose of each document ensures accurate reporting and compliance with state tax laws.

When filling out the California 3885 form, it is essential to follow specific guidelines to ensure accuracy and compliance. Here are eight things to consider:

This form is applicable to all corporations, including small businesses and limited liability companies (LLCs) that are classified as corporations.

Corporations must complete this form if they want to claim depreciation and amortization deductions on their California tax returns.

In California, the maximum deduction is limited to $25,000, which differs from federal limits.

Not all property qualifies; off-the-shelf computer software and certain vehicles do not meet the criteria.

In addition to depreciation, the form is also used to calculate amortization for intangible assets.

Corporations must choose one or the other for the same taxable year; they cannot elect both.

There are significant differences between California and federal laws that affect how depreciation is calculated.

Different methods apply based on the type of property, such as straight-line or declining balance methods.

The election can be revoked, but only with consent from the Franchise Tax Board.

Filling out the form accurately requires attention to detail, including specific descriptions and costs for each asset.

The California 3885 form is used by corporations to calculate depreciation and amortization deductions.

Corporations, partnerships, and LLCs classified as corporations can utilize this form, while S corporations must use Schedule B (100S).

IRC Section 179 allows corporations to expense certain property, with a maximum deduction of $25,000 for California.

The total cost of IRC Section 179 property placed in service must be reported, as it affects the deduction limit.

California has specific differences from federal law regarding depreciation and amortization, which must be understood to ensure compliance.

Corporations must make their election for IRC Section 179 on a timely filed tax return, and this election cannot be revoked without consent from the Franchise Tax Board.

Listed property, such as passenger automobiles and certain entertainment equipment, has specific rules under IRC Section 179.

For depreciation, corporations can choose from various methods, including straight-line and declining balance, depending on the asset type and useful life.

Amortization for intangible assets typically follows a straight-line basis over 15 years, but there are exceptions based on asset type.

It is crucial for corporations to maintain accurate records of property costs and depreciation calculations to support their deductions on tax returns.