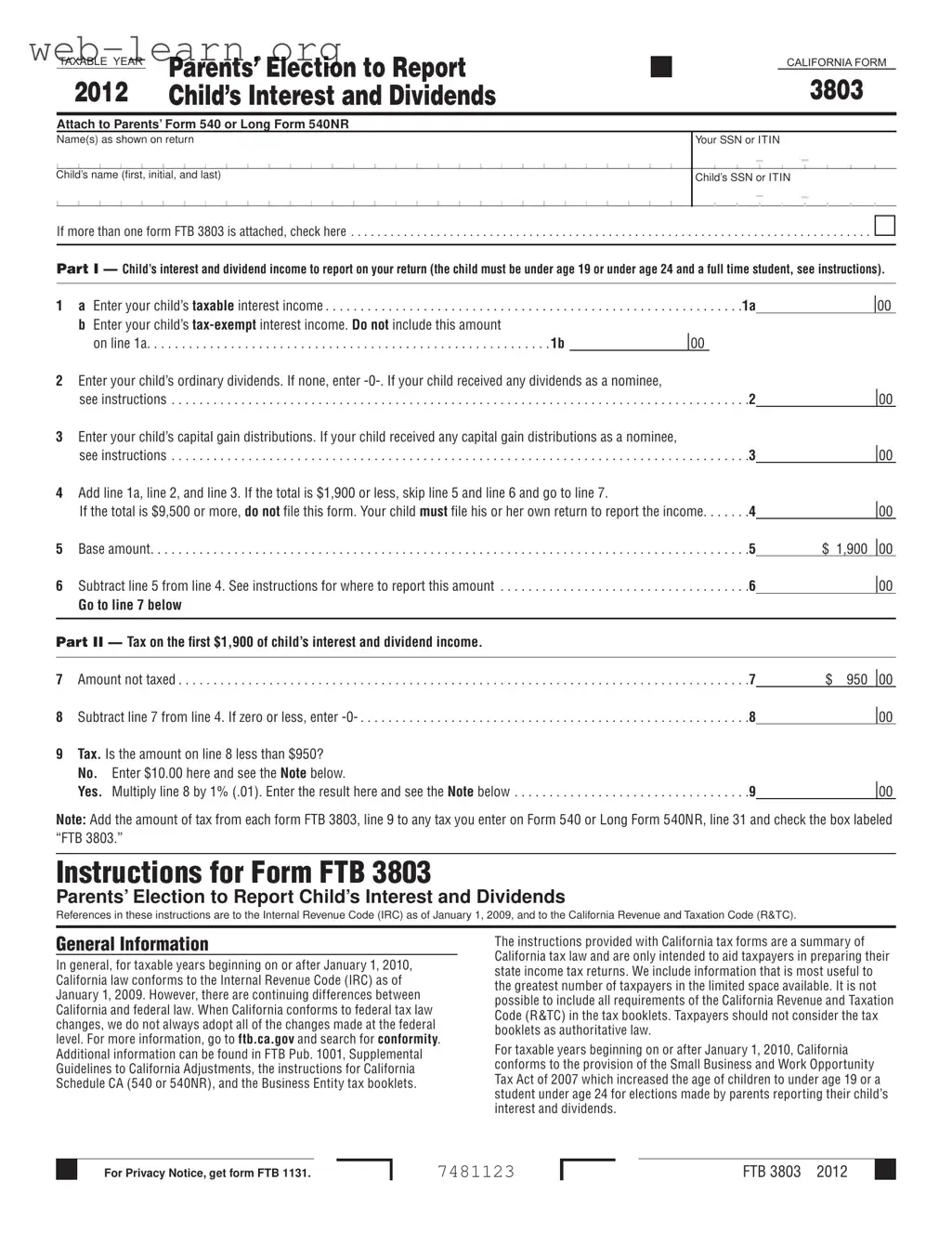

The California Form 3803, also known as the Parents’ Election to Report Child’s Interest and Dividends, plays a crucial role for families managing their children's income tax responsibilities. This form allows parents to report their child's interest and dividend income on their own tax returns, simplifying the filing process for children under 19 or under 24 if they are full-time students. By completing this form, parents can elect to include their child's income, which must not exceed $9,500, thereby relieving the child from the obligation to file a separate return. The form requires parents to provide essential details, including the child's name and Social Security Number (SSN) or Individual Taxpayer Identification Number (ITIN), as well as the total amount of the child's taxable interest and dividends. Notably, if the child's total income is $1,900 or less, no tax is owed on that amount, making this form particularly beneficial for families with modest income. The tax implications are straightforward, as the form guides parents through calculating any additional tax owed based on the child's income. Understanding the nuances of this form can help families make informed decisions about their tax filings and optimize their financial responsibilities.

| Fact Name | Details |

|---|---|

| Purpose of Form | The California Form 3803 allows parents to report their child's interest and dividend income on their own tax returns, preventing the child from needing to file separately. |

| Eligibility Criteria | To use this form, the child must be under age 19 or under age 24 if a full-time student, and their income must come solely from interest and dividends with a total gross income below $9,500. |

| Governing Laws | This form is governed by the California Revenue and Taxation Code (R&TC) and conforms to the Internal Revenue Code (IRC) as of January 1, 2009. |

| Filing Requirements | Form 3803 must be attached to either Form 540 or Long Form 540NR when filed, and a separate form is required for each child whose income is being reported. |

Filling out the California 3803 form involves several steps to ensure accurate reporting of your child's interest and dividends on your tax return. Follow these instructions carefully to complete the form correctly.

What is California Form 3803?

California Form 3803, also known as the Parents' Election to Report Child's Interest and Dividends, allows parents to report their child's interest and dividend income on their own tax return. This form is useful for parents who wish to avoid having their child file a separate tax return if the child's income falls below certain thresholds.

Who qualifies to use Form 3803?

To use Form 3803, the child must be under age 19, or under age 24 if a full-time student. The child must also have income solely from interest and dividends, with gross income below $9,500. Additionally, the parents must meet specific criteria regarding their filing status and income level.

How do I complete Form 3803?

To complete Form 3803, you need to provide your name, your child's name, and their Social Security Number (SSN) or Individual Taxpayer Identification Number (ITIN). You will enter the child's taxable interest income, tax-exempt interest income, ordinary dividends, and capital gain distributions. The form will guide you through calculating the total income and any tax owed.

What happens if my child's total income is $1,900 or less?

If the total income reported on Form 3803 is $1,900 or less, you can skip certain lines related to additional tax calculations. This simplifies the process, as you will not owe any tax on that income. However, if the total is $9,500 or more, the child must file their own tax return.

Can I use Form 3803 if I filed a federal return differently?

Yes, you can elect to report your child's income on your California return even if you did not do so on your federal return. California allows this election as long as you meet the qualifications outlined in the form's instructions.

What if I have more than one child?

If you have more than one child whose income you wish to report, you must complete a separate Form 3803 for each child. Attach each form to your Form 540 or Long Form 540NR when you file your tax return.

How do I file Form 3803?

To file Form 3803, complete the form and attach it to your Form 540 or Long Form 540NR. Ensure that you file your return by the due date, including any extensions. Be sure to check the box labeled “FTB 3803” on your tax return to indicate that you are reporting your child's income.

When filling out the California 3803 form, many individuals make common mistakes that can lead to complications in their tax filings. One frequent error is failing to accurately report the child’s Social Security Number (SSN) or Individual Taxpayer Identification Number (ITIN). The form requires this information to be correct and consistent with the child’s tax records. Omitting or misentering this number can delay processing and cause issues with the IRS.

Another mistake is not understanding the eligibility criteria for reporting the child’s income. Parents must ensure that the child is under age 19 or a full-time student under age 24. If the child does not meet these criteria, the election to report the child's income cannot be made. This oversight can result in the need for the child to file their own tax return, which may incur additional taxes or penalties.

Many people also overlook the requirement to separate taxable and tax-exempt income. Line 1a of the form specifically asks for taxable interest income, while line 1b is for tax-exempt interest. Confusing these lines can lead to incorrect calculations and potential issues with tax liability. It is crucial to read the instructions carefully to ensure that each type of income is reported accurately.

In addition, some filers fail to check the box indicating that more than one form FTB 3803 is attached if applicable. This can create confusion for tax authorities and may lead to delays in processing the tax return. Properly indicating the number of forms attached helps ensure that all relevant information is considered during processing.

Lastly, individuals often neglect to follow the specific instructions for calculating the tax on the child’s income. The form includes distinct lines for different calculations, and miscalculating these figures can result in incorrect tax amounts being reported. It is essential to carefully follow the steps outlined in the instructions to avoid errors that could affect the overall tax return.

The California Form 3803 is essential for parents electing to report their child's interest and dividends on their tax returns. Several other forms and documents are often used in conjunction with this form. Below is a list of these documents, each serving a specific purpose in the tax filing process.

Utilizing these forms and publications can streamline the tax filing process and ensure compliance with California tax laws. It is essential to gather all necessary documents before filing to avoid delays and potential issues with the tax authorities.

The California Form 3803, which allows parents to report their child's interest and dividends on their tax returns, shares similarities with several other tax documents. Here’s a breakdown of eight forms that are akin to the California 3803 form, along with a brief explanation of how they are similar:

When filling out the California 3803 form, it is essential to be thorough and accurate. Here are some guidelines to follow, as well as common pitfalls to avoid.

By adhering to these guidelines, parents can ensure that they accurately report their child's interest and dividend income, simplifying the tax filing process for both themselves and their child.

Understanding the California Form 3803 can be challenging, and there are several misconceptions that can lead to confusion. Here are five common misunderstandings about this form:

In fact, parents can report their child's income if the child is under age 19 or under age 24 and a full-time student. This flexibility allows more families to take advantage of the form.

Some believe that the form is limited to interest income. However, it applies to both interest and dividends, including capital gain distributions. Parents can report a variety of income types using this form.

While it is true that if the child's total income exceeds $9,500, they must file their own return, parents can still use Form 3803 if the income is $1,900 or less. This threshold is crucial for determining eligibility.

Parents may choose to report their child's income on their California state tax return without having to do the same on their federal return. This option provides flexibility based on individual tax situations.

It is a common belief that parents can reduce the reported income by claiming deductions. However, any deductions that the child would have claimed on their own return cannot be used when filing Form 3803.

The California 3803 form allows parents to report their child's interest and dividend income on their tax return.

This election is available for children under age 19 or under age 24 if they are full-time students.

To qualify, the child must have income solely from interest and dividends, and their gross income must be less than $9,500.

Parents must file either Form 540 or Long Form 540NR to use this election.

Each child requires a separate California 3803 form if parents choose to report multiple children’s income.

Part I of the form is used to calculate the child’s total interest and dividend income.

Part II determines any additional tax owed on the first $1,900 of the child’s income.

It is important to file the form by the due date of the tax return, including any extensions.