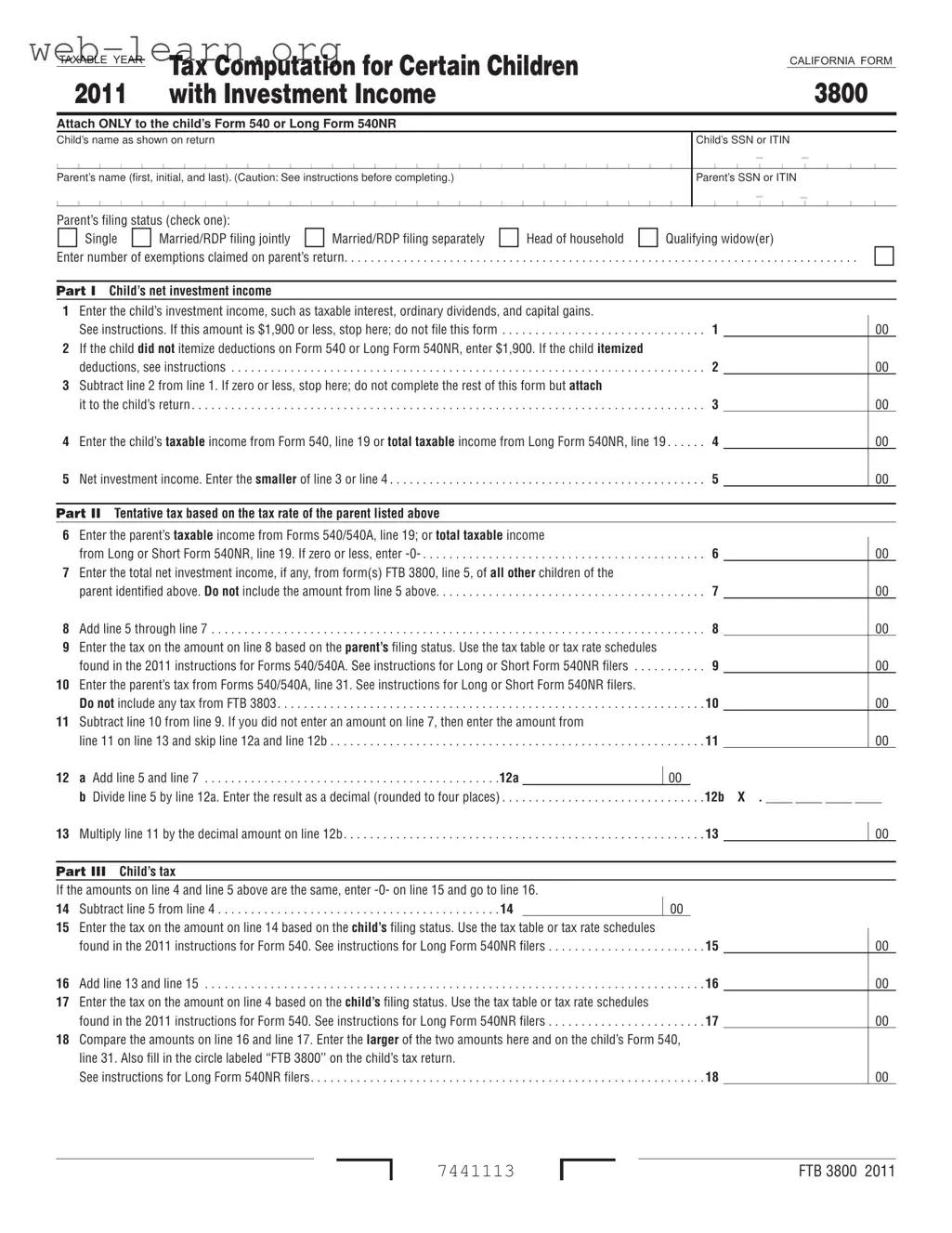

The California Form 3800 serves as a vital tool for parents navigating the complexities of tax obligations related to their children’s investment income. Specifically designed for children aged 18 and under, or students under the age of 24, this form is required when a child has investment income exceeding $1,900. By completing Form 3800, parents can ensure that any investment income is taxed at their own tax rate, which is often higher than the child’s rate. The form requires essential information, including the child’s name and Social Security Number (SSN), as well as the parent’s filing status and income details. It breaks down the calculation of the child’s net investment income and determines the tentative tax based on the parent’s tax rate. Furthermore, it guides parents through various scenarios, such as when to stop completing the form based on specific income thresholds. By understanding the purpose and requirements of Form 3800, families can effectively manage their tax responsibilities and potentially minimize their overall tax burden.

| Fact Name | Details |

|---|---|

| Form Purpose | This form calculates tax for certain children with investment income exceeding $1,900. |

| Eligibility Criteria | Children must be 18 or younger, or students under 24, with living parents at the end of the tax year. |

| Filing Requirement | The form must be attached to the child's Form 540 or Long Form 540NR. |

| Investment Income Threshold | If the child's investment income is $1,900 or less, this form does not need to be filed. |

| Governing Law | California Revenue and Taxation Code (R&TC) governs the use of this form. |

| Parent's Tax Rate | Tax on the child's investment income is calculated at the parent's tax rate if it is higher. |

| Form Version | This is the 2011 version of the FTB 3800 form. |

| Additional Forms | Form FTB 3803 may be required for parents electing to report their child's interest and dividends. |

Filling out the California Form 3800 is essential for determining the tax owed by certain children with investment income. This process requires careful attention to detail to ensure accuracy. After completing the form, it must be attached to the child's Form 540 or Long Form 540NR for submission.

Proceed to Part I to calculate the child's net investment income.

Move to Part II to calculate the tentative tax based on the parent's tax rate.

In Part III, calculate the child’s tax.

California Form 3800, also known as the Tax Computation for Certain Children with Investment Income, is designed to calculate the tax for children who have investment income exceeding $1,900. If a child qualifies, their investment income is taxed at the parent's tax rate, which may be higher than the child's rate. This form must be attached to the child's Form 540 or Long Form 540NR when filing.

Form 3800 is required for children who meet the following criteria:

When filling out Form 3800, parents should report the child's net investment income, which includes:

It is essential to only include income that is taxable under California law.

The tax calculation involves several steps:

Detailed instructions are provided on the form to guide you through each calculation step.

If the child's investment income is $1,900 or less, they do not need to file Form 3800. Instead, the tax can be calculated using the regular methods on the child's Forms 540/540A or Long or Short Form 540NR.

Yes, parents may elect to include their child's investment income on their own tax return if the child only has income from interest and dividends. This election allows the child to avoid filing a separate tax return or Form 3800. However, if estimated tax payments were made in the child's name, this option is not available.

When completing Form 3800, the parent’s name and Social Security Number (SSN) or Individual Taxpayer Identification Number (ITIN) must be provided. If the parents are married and filed jointly, the information of the parent listed first on the joint return should be used. In cases where parents are separated or unmarried, the information of the custodial parent is generally required.

Filling out the California 3800 form can be a bit tricky, and mistakes are common. One common error is not accurately reporting the child's net investment income. Line 1 asks for this income, which includes taxable interest, dividends, and capital gains. If you mistakenly leave this line blank or enter an incorrect amount, it can lead to significant issues. Always double-check to ensure the income reported matches what is taxable under California law.

Another frequent mistake is related to the parent’s information. When entering the parent’s name and Social Security Number (SSN) or Individual Taxpayer Identification Number (ITIN), it’s crucial to follow the guidelines carefully. For example, if the parents filed a joint return, the name and SSN of the first parent listed should be used. Failing to do this can cause confusion and delays in processing the form.

People also often overlook the importance of checking the child’s filing status. The form requires you to determine whether the child is filing as a dependent or has investment income exceeding $1,900. If you mistakenly indicate the wrong status, it can lead to incorrect tax calculations. Be sure to review the instructions to understand how to classify the child correctly.

Lastly, many individuals forget to attach the California 3800 form to the child’s Form 540 or Long Form 540NR. This is a crucial step. If the form isn’t attached, it may not be considered during the tax assessment, potentially leading to penalties or missed deductions. Always ensure that you follow the submission guidelines to avoid this mistake.

The California 3800 form is used to calculate the tax for certain children with investment income. When filling out this form, several other documents may be required to ensure accurate reporting and compliance with tax regulations. Below is a list of forms and documents that are often used alongside the California 3800 form, along with a brief description of each.

Having these forms and documents ready can streamline the tax filing process and ensure that all necessary information is accurately reported. It is always beneficial to consult with a tax professional if there are any uncertainties regarding the completion of these forms or the tax implications for children with investment income.

The California Form 3800 is used to calculate the tax for certain children with investment income. Several other tax forms share similarities with the California 3800 form, particularly in their purpose and structure. Below are seven documents that are similar to the California 3800 form, along with explanations of how they relate to it.

When filling out the California Form 3800, it is essential to approach the task with care and attention. Here’s a guide on what to do and what to avoid to ensure a smooth process.

By following these guidelines, you can navigate the completion of the California Form 3800 with confidence. Taking the time to ensure accuracy will help avoid unnecessary issues down the line.

Understanding the California 3800 form is essential for parents managing their children's investment income. However, several misconceptions can lead to confusion. Here are ten common misconceptions and clarifications:

This is incorrect. The form applies to children who are 18 and under or students under 24 at the end of the tax year.

Not true. The form is only necessary if the child's investment income exceeds $1,900.

This is misleading. Only specific types of investment income, such as interest and dividends, should be reported.

Actually, if parents elect to report the child's income on their return, the child does not need to file a separate return.

Each tax year may have different requirements and thresholds. Always check the specific instructions for the relevant year.

Both parents should ensure they understand their responsibilities, especially if they are filing separately.

This is not advisable. Supporting documentation is essential to substantiate the information reported on the form.

Only the child with qualifying investment income should be reported on this form.

The form calculates tax based on the parent's rate, which may not always be lower.

If the child's income exceeds the threshold, filing the form is necessary to comply with tax regulations.

Here are some key takeaways regarding the California 3800 form, which is used for computing taxes for certain children with investment income: