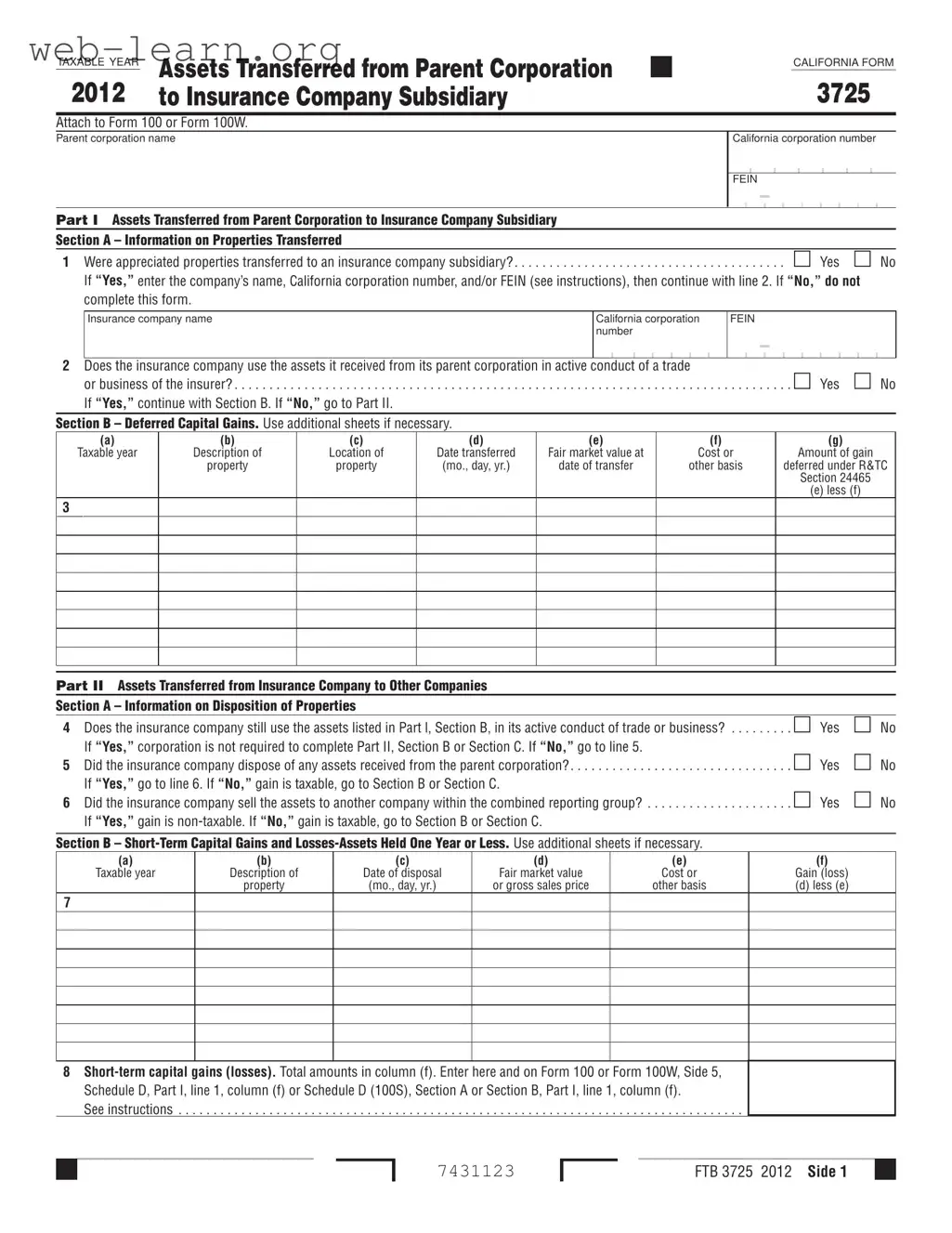

The California 3725 form is an essential document for corporations involved in transactions between a parent corporation and its insurance company subsidiary. This form is used to report the transfer of assets, particularly appreciated properties, and to calculate any deferred capital gains or losses associated with those transfers. It includes sections that require detailed information about the properties transferred, such as their fair market value at the time of transfer, and whether the insurance company actively uses these assets in its business operations. The form also addresses the tax implications of these transactions, specifying when gains must be recognized as income. For example, if the transferred property is no longer owned by the insurance company or is not used in its active trade, the gain must be reported. The California Revenue and Taxation Code Section 24465 governs these transactions, providing clarity on how to handle capital gains from appreciated properties. Understanding the nuances of this form is crucial for compliance and for optimizing tax outcomes.

| Fact Name | Fact Description |

|---|---|

| Purpose | The California 3725 form is used to track assets transferred from a parent corporation to an insurance company subsidiary. |

| Governing Law | This form is governed by California Revenue and Taxation Code (R&TC) Section 24465. |

| Deferred Gain | Gains from transferred appreciated property are deferred if the assets are used in the active conduct of the insurer's trade or business. |

| Appreciated Property | Appreciated property refers to assets whose fair market value exceeds their adjusted basis at the time of transfer. |

| Commonly Controlled Group | A commonly controlled group exists when a parent corporation or family members own more than 50% of voting power in multiple corporations. |

| Transfer Date | The form must be used for transactions involving asset transfers that occur on or after June 23, 2004. |

| Sections | The form includes sections for both assets transferred to an insurance company subsidiary and assets disposed of by the insurance company. |

| Tax Implications | If transferred property is no longer owned or used by the insurer, the gain must be recognized as income. |

Filling out the California 3725 form is an important step in reporting the transfer of assets from a parent corporation to an insurance company subsidiary. Once you have completed the form, it should be attached to either Form 100 or Form 100W as part of your tax return. Here are the steps to guide you through the process of filling out the form:

Once you’ve completed these steps, ensure all information is accurate. Attach the California 3725 form to your tax return, and you’re ready to submit. It's always a good idea to keep a copy for your records.

The California 3725 form is used to track assets transferred from a parent corporation to an insurance company subsidiary. It helps in calculating capital gains or losses resulting from these transfers. This form is particularly important for transactions that occur on or after June 23, 2004, as specified by California Revenue and Taxation Code (R&TC) Section 24465.

You should complete this form if your parent corporation has transferred appreciated properties to an insurance company subsidiary. If no appreciated properties were transferred, there is no need to fill out the form. Additionally, if the insurance company does not actively use the assets received from the parent corporation, you may need to complete specific sections regarding capital gains.

Part I requires details about the assets transferred from the parent corporation. You must indicate whether appreciated properties were transferred, provide the name and identification numbers of the insurance company, and confirm if the assets are used in the active conduct of the insurer's trade or business. If the assets are actively used, you will continue to Section B for deferred capital gains.

Capital gains or losses are reported in Part II of the form. You will need to specify whether the assets are short-term or long-term based on how long they were held. Enter the fair market value or sales price, cost or other basis, and calculate the gain or loss accordingly. The totals should then be transferred to the appropriate lines on Form 100 or Form 100W.

If the insurance company no longer uses the assets in its active trade or business, you must report any gains as taxable. You will need to determine if the assets were sold to another company within the combined reporting group, as this may affect the taxability of the gain.

Yes, two key definitions are crucial. First, "appreciated property" refers to property whose fair market value exceeds its adjusted basis at the time of transfer. Second, a "commonly controlled group" is a group of corporations with a common parent that owns more than 50% of the voting power. Understanding these terms will help ensure accurate reporting on the form.

Filling out the California Form 3725 can be a straightforward process, but there are common pitfalls that can lead to mistakes. Understanding these mistakes can help ensure that your form is completed accurately and efficiently.

One common mistake is failing to provide the correct identifying information for both the parent corporation and the insurance company subsidiary. This includes the California corporation number and the Federal Employer Identification Number (FEIN). Omitting or incorrectly entering this information can delay processing or lead to complications down the line.

Another frequent error occurs when individuals do not properly assess whether the assets transferred were indeed appreciated properties. If you answer "Yes" to the question about appreciated properties but fail to provide the necessary details, it can result in confusion and potential penalties. Always ensure you understand the definitions provided in the form instructions.

In Section B, where deferred capital gains are reported, many people mistakenly enter inaccurate values for the fair market value and the cost or other basis of the assets. It's essential to accurately calculate these values based on the guidelines provided. If the fair market value is not correctly determined, it can lead to incorrect tax calculations.

Another mistake is skipping the follow-up questions in Section A regarding the active use of assets. If the insurance company does not actively use the transferred assets, it is crucial to answer these questions correctly. Misunderstanding this section can lead to misreporting gains or losses.

Some individuals also overlook the importance of record-keeping. Failing to maintain adequate documentation of the assets transferred can complicate matters if the form is audited. Keeping detailed records ensures that you can substantiate the information provided on the form if needed.

Additionally, people often neglect to review the instructions for reporting short-term and long-term capital gains accurately. Entering these amounts incorrectly can impact your overall tax liability. Always double-check the specific lines where these totals should be reported to avoid mistakes.

Lastly, failing to attach the completed Form 3725 to the appropriate tax return can lead to significant issues. Ensure that you follow the instructions regarding attachments carefully. Not doing so can result in your form being overlooked, which may lead to penalties or additional scrutiny from tax authorities.

By being aware of these common mistakes, you can approach the completion of California Form 3725 with greater confidence and accuracy, ultimately ensuring compliance and reducing the risk of complications.

The California 3725 form is essential for tracking assets transferred from a parent corporation to an insurance company subsidiary. However, it is often used in conjunction with other forms and documents that provide additional context and information. Below are four important documents that frequently accompany the California 3725 form.

Each of these documents plays a crucial role in ensuring accurate reporting and compliance with California tax regulations. Using them in conjunction with the California 3725 form helps to provide a complete picture of asset transfers and their tax implications.

When filling out the California 3725 form, it's essential to approach the process carefully to ensure accuracy and compliance. Here’s a list of things to do and avoid:

There are several misconceptions regarding the California 3725 form that can lead to confusion. Here are seven common misunderstandings:

When dealing with the California Form 3725, there are several important points to keep in mind to ensure proper compliance and accurate reporting. Here are four key takeaways: