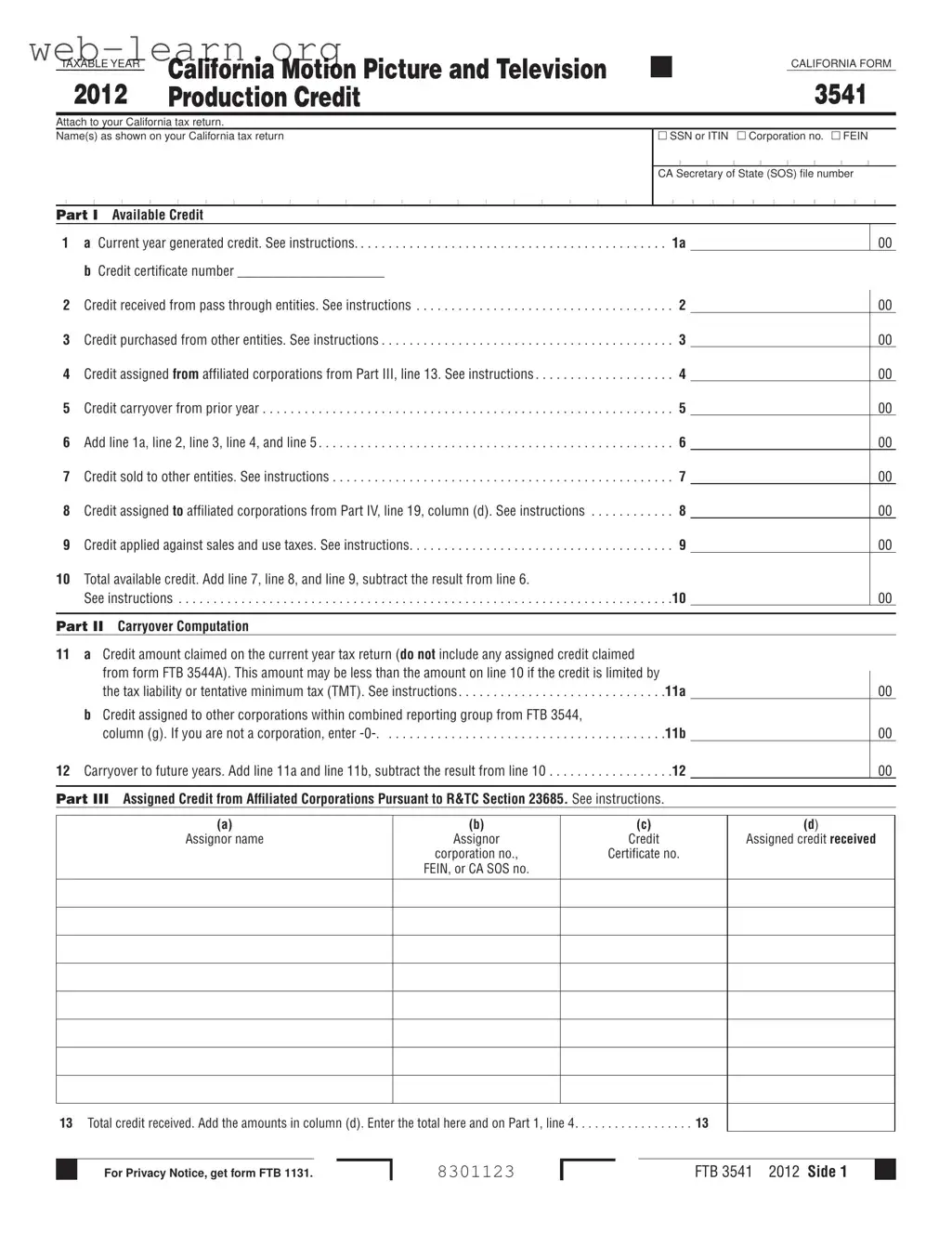

The California Form 3541 is a crucial document for taxpayers engaged in the motion picture and television production industry, particularly those seeking to benefit from the California Motion Picture and Television Production Credit. This form is essential for reporting various types of credits available to qualified taxpayers, including credits generated during the current year, credits received from pass-through entities, and those purchased from other entities. Additionally, the form facilitates the assignment of credits to affiliated corporations, enabling taxpayers to manage their tax liabilities effectively. It includes sections for calculating total available credits, carryover computations, and specific details regarding credits assigned from or to affiliated corporations. Taxpayers must attach Form 3541 to their California tax returns and follow the guidelines provided to ensure compliance with the Revenue and Taxation Code. The form not only serves to document the credits claimed but also plays a significant role in the strategic financial planning of production companies operating within California, which has established itself as a prominent hub for the film and television industry.

| Fact Name | Fact Description |

|---|---|

| Purpose | The California Form 3541 is used to report the California Motion Picture and Television Production Credit. |

| Governing Law | This form is governed by Revenue and Taxation Code (R&TC) Sections 17053.85 and 23685. |

| Eligibility | Qualified taxpayers must have incurred qualified expenditures and received a credit certificate from the California Film Commission (CFC). |

| Credit Amount | The credit is 20% of expenditures for a qualified motion picture and 25% for independent films or television series relocating to California. |

| Usage of Credit | Taxpayers can use the credit to offset income tax liability, sell to unrelated parties (for independent films), assign to affiliated corporations, or apply against qualified sales and use taxes. |

| Credit Assignment | Taxpayers can assign credits to affiliated corporations, but the election to assign is irrevocable and cannot be reassigned once made. |

| Carryover | If the available credit exceeds current year tax liability, it can be carried over for up to six years or until exhausted. |

| Attachment Requirement | Form 3541 must be attached to the appropriate California tax return, such as Form 100, 540, or 540NR. |

Completing the California 3541 form is an important step in ensuring that you accurately report your motion picture and television production credits. Following the steps below will help you navigate the process smoothly. After filling out the form, be sure to attach it to your California tax return as required.

What is the California 3541 form?

The California 3541 form is used to claim the California Motion Picture and Television Production Credit. This credit is available to qualified taxpayers who incur eligible production expenditures for motion pictures or television series produced in California. It is essential to attach this form to your California tax return to claim the credit.

Who qualifies as a "qualified taxpayer"?

A "qualified taxpayer" is defined as an individual or entity that has paid or incurred qualified expenditures and has received a credit certificate from the California Film Commission (CFC). This includes corporations, limited liability companies (LLCs) taxed as corporations, partnerships, and individuals who meet the necessary requirements.

What types of productions are eligible for the credit?

Eligible productions include qualified motion pictures produced for public distribution, independent films with budgets between $1 million and $10 million, and television series that relocate to California after filming prior seasons elsewhere. The credit is designed to incentivize productions to take place within the state.

How is the credit amount calculated?

The credit is calculated based on the production expenditures. For qualified motion pictures, the credit is typically 20% of the expenditures. Independent films and television series that relocate to California may qualify for a higher credit rate of 25%. The specific amounts must be reported on the form based on the details provided by the CFC.

Can the credit be assigned or sold?

Yes, the credit can be assigned to affiliated corporations or sold to unrelated parties, specifically for independent films. However, it's important to note that the assignment election is irrevocable. Once assigned, the credit cannot be reassigned, and both the assignor and assignee must maintain records to substantiate the transaction.

What happens if the credit exceeds my tax liability?

If the available credit exceeds your current year tax liability, you may carry over the unused credit to future years. This carryover can last for up to six years or until the credit is fully utilized. However, it is crucial to apply the credit to the earliest taxable year possible.

Are there limitations on how the credit can be used?

Indeed, there are limitations. The credit cannot reduce certain taxes, such as the minimum franchise tax or the alternative minimum tax. Additionally, it cannot lower the tax liability below the tentative minimum tax. Understanding these limitations is vital for effective tax planning.

What documentation is required when filing the 3541 form?

When filing the California 3541 form, it is essential to include your credit certificate number, details of any credits received from pass-through entities, and any other relevant documentation that supports your claim. Maintaining thorough records is critical, as the Franchise Tax Board may request access to these records to verify your claims.

Filling out the California Form 3541 can be a complex process, and mistakes can lead to complications with tax credits. One common error occurs when individuals fail to accurately report the current year generated credit on Line 1a. This line requires the total amount of credit allocated by the California Film Commission (CFC) as shown on Form M. If multiple Form Ms were received, the credits must be summed up. Neglecting to do this can result in an incorrect total, which may affect the overall credit calculation.

Another frequent mistake involves misreporting the credit certificate number on Line 1b. Taxpayers should ensure that they enter the correct number corresponding to the credit amount reported on Line 1a. If multiple credits are reported, all relevant certificate numbers must be listed. Omitting this information or entering an incorrect number can lead to delays or rejections of the credit claim.

Many individuals also overlook the requirement to provide documentation for credits received from pass-through entities on Line 2. It is essential to attach a schedule that details the taxpayer names, identification numbers, and ownership percentages associated with these entities. Failing to include this supporting documentation can result in the disallowance of the claimed credit.

In addition, errors can occur when entering the credit amount assigned from affiliated corporations on Line 4. Taxpayers must complete Part III of the form to determine the correct amount to report. Not doing so can lead to incorrect figures being submitted, which can complicate future credit assignments and tax liabilities.

Another common oversight happens when individuals miscalculate the excess credit available for assigning to affiliated corporations on Line 16. This line requires the subtraction of the tax liability from the total available credit. If this calculation is incorrect, it can lead to assigning a credit that exceeds what is allowable, resulting in potential penalties.

Finally, many taxpayers forget to write “CFC Credit” in red ink at the top margin of their tax return. This simple step alerts the tax authorities to the specific nature of the credit being claimed. Neglecting this instruction can lead to confusion and may delay the processing of the tax return.

The California Form 3541 is used to report the California Motion Picture and Television Production Credit. This form is often accompanied by several other documents that support the credit claims and provide necessary information for tax purposes. Below is a list of five forms and documents commonly used alongside the California 3541 form.

These forms and documents work together to facilitate the proper reporting and utilization of the California Motion Picture and Television Production Credit. Ensuring that all required documentation is completed accurately is crucial for compliance and maximizing potential tax benefits.

When filling out the California 3541 form, attention to detail is crucial. Here are four important dos and don'ts to keep in mind:

This form is available to any qualified taxpayer involved in motion picture and television production, regardless of company size. Independent filmmakers can also benefit from this credit.

In fact, qualified taxpayers can assign credits to affiliated corporations or sell them, particularly in the case of independent films. This flexibility can enhance financial opportunities.

The California Motion Picture and Television Production Credit is not refundable. Taxpayers can only use it to offset tax liabilities or apply it against sales and use taxes.

This credit cannot be carried back. Taxpayers can only carry it forward for up to six years or until the credit is exhausted.

Only expenditures that meet specific criteria set by the California Film Commission qualify for the credit. Taxpayers should carefully review these criteria.

Credits are not allowed at the pass-through entity level. Instead, they pass through to shareholders or partners who must claim them on their individual returns.

Taxpayers must receive a credit certificate from the California Film Commission before claiming the credit. This certificate confirms eligibility.

The credit does not reduce the minimum franchise tax for corporations or S corporations. It is essential to understand this limitation when planning finances.

Taxpayers must retain all records documenting the credit and any carryover used in prior years. The Franchise Tax Board may require access to these records for verification.

Filling out the California Form 3541 is an important step for taxpayers involved in the motion picture and television industry. Here are some key takeaways to consider: