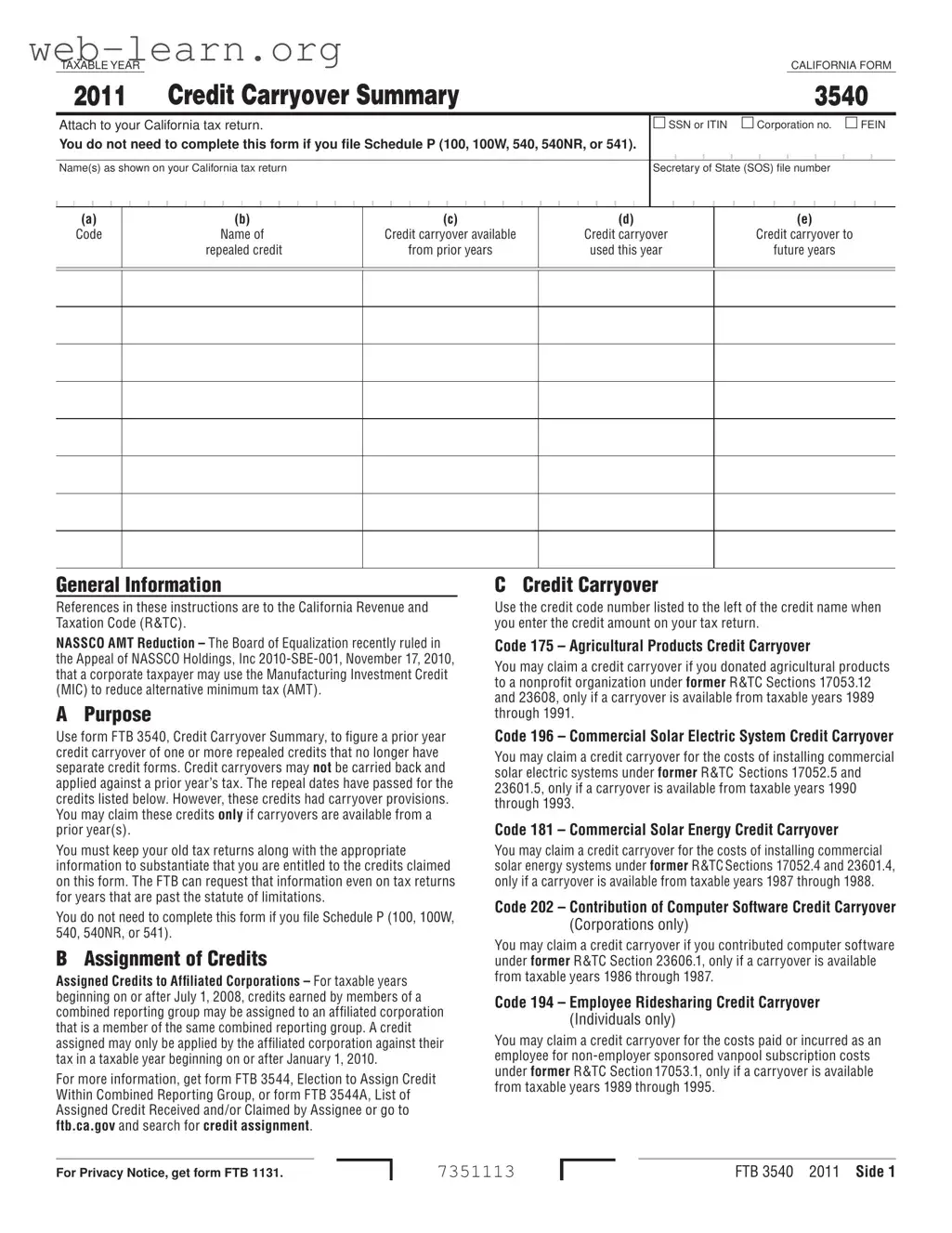

The California Form 3540, known as the Credit Carryover Summary, plays an important role for taxpayers who have credits from previous years that can still be utilized. This form is necessary for those who want to calculate and report any carryover of repealed tax credits that no longer have separate forms. Taxpayers must attach this form to their California tax return if they have available credit carryovers from prior years. The form requires specific information, including the taxpayer's identification number, the name of the credit, and the amounts available for carryover, used, and to be carried over to future years. Notably, the form is not required if taxpayers file certain schedules, such as Schedule P. Various types of credits are listed, including those related to energy conservation, ridesharing programs, and agricultural donations, each with its own set of limitations and eligibility criteria. Understanding how to properly complete this form is crucial for maximizing potential tax benefits while ensuring compliance with California tax regulations.

| Fact Name | Fact Details |

|---|---|

| Form Purpose | The California Form 3540 is used to summarize credit carryovers from prior years for certain repealed tax credits. |

| Governing Law | This form is governed by the California Revenue and Taxation Code (R&TC). |

| Eligibility | Taxpayers must have carryovers available from prior years to claim credits on this form. |

| Filing Requirement | Taxpayers do not need to complete this form if they file Schedule P (100, 100W, 540, 540NR, or 541). |

| Credit Assignment | Credits earned by members of a combined reporting group may be assigned to affiliated corporations starting from taxable years after July 1, 2008. |

| Credit Limitations | Generally, credit carryovers cannot reduce the minimum franchise tax or alternative minimum tax, with specific exceptions for certain credits. |

Completing the California 3540 form is an important step for those looking to summarize their credit carryovers. This form must be attached to your California tax return. Ensure you have all necessary information at hand before you begin filling it out. The following steps will guide you through the process.

The California Form 3540, also known as the Credit Carryover Summary, is used to report and calculate the carryover of certain tax credits that have been repealed. These credits may no longer have separate forms, but taxpayers can still utilize any remaining credits from prior years. The form helps ensure that eligible taxpayers can claim these credits on their current tax returns, provided they have carryovers available from previous years.

Not every taxpayer needs to fill out Form 3540. If you file Schedule P (100, 100W, 540, 540NR, or 541), you do not need to complete this form. However, if you have carryover credits from prior years that are eligible for use, and you are not filing the aforementioned schedules, then you should complete Form 3540 to claim those credits.

Form 3540 allows taxpayers to report various types of repealed credits, including but not limited to:

Each credit has specific eligibility requirements and carryover periods, so it is essential to refer to the instructions for the exact details related to each credit.

Yes, there are limitations regarding how credits can be applied. Generally, a credit carryover cannot reduce certain taxes, such as the minimum franchise tax or alternative minimum tax (AMT). Additionally, if the available credit carryover exceeds your current tax liability, any unused amount can be carried over to future years, but only until the carryover period expires. It is crucial to apply the carryover to the earliest taxable years possible to maximize its benefits.

Filling out the California Form 3540 can be a daunting task, and many individuals make critical mistakes that can lead to complications. One common error is failing to provide the correct identification numbers. It is essential to include your Social Security Number (SSN) or Individual Taxpayer Identification Number (ITIN), along with any relevant corporation numbers. Missing this information can delay the processing of your tax return.

Another mistake is neglecting to check the eligibility requirements for the credits being claimed. Each credit has specific rules regarding carryover from prior years. Individuals often assume they qualify without verifying the necessary conditions. This oversight can result in denied credits and potential penalties.

Many filers also struggle with accurately calculating the credit carryover amounts. Column (c) requires the carryover available from prior years, while column (d) is for the amount claimed this year. Miscalculating these figures can lead to incorrect reporting, which may attract scrutiny from tax authorities.

Additionally, failing to maintain proper documentation is a significant pitfall. The Franchise Tax Board (FTB) may request substantiating information even for past tax returns. Without the necessary records, taxpayers may find it challenging to defend their claims.

Some individuals mistakenly believe that they can carry back credits to offset previous years' taxes. This is not allowed. Understanding that credits can only be carried forward is crucial to avoid confusion and ensure compliance.

Using the wrong credit code is another frequent error. Each credit has a specific code that must be entered correctly in column (a). Incorrect coding can lead to delays in processing or even denial of the credit.

Another common issue arises when taxpayers do not apply credits to the earliest taxable years possible. This can limit the benefits of the credit and may result in lost opportunities for tax savings.

Moreover, some filers overlook the limitations imposed on certain credits. For example, credits cannot reduce the minimum franchise tax or alternative minimum tax for corporations. Ignoring these limitations can lead to unexpected tax liabilities.

Finally, failing to review the instructions thoroughly can lead to misunderstandings about the form's requirements. Each section of the form has specific instructions that must be followed closely. Skipping this step can result in incomplete or incorrect submissions.

In summary, taking the time to carefully fill out the California Form 3540 is essential. Avoiding these common mistakes can save taxpayers from complications and ensure they receive the credits they are entitled to.

The California Form 3540 is an essential document for taxpayers looking to report credit carryovers from prior years. Along with this form, several other documents may be required or beneficial for a complete and accurate tax filing. Below is a list of forms and documents that are often used in conjunction with the California 3540 form, along with brief descriptions of each.

It is crucial to gather all relevant forms and documents before filing your taxes. This preparation ensures that you can accurately report any credit carryovers and comply with California tax regulations. If you have any questions or need assistance, consider reaching out to a tax professional for guidance.

When filling out the California 3540 form, consider the following guidelines:

Additionally, avoid the following mistakes:

Understanding the California Form 3540 is crucial for taxpayers who want to maximize their tax credits. However, several misconceptions can lead to confusion. Here are seven common misconceptions about the California 3540 form:

Being aware of these misconceptions can help taxpayers navigate the complexities of the California Form 3540 more effectively. Accurate understanding is essential for optimizing tax benefits.

Here are some important points to remember when filling out and using the California 3540 form: