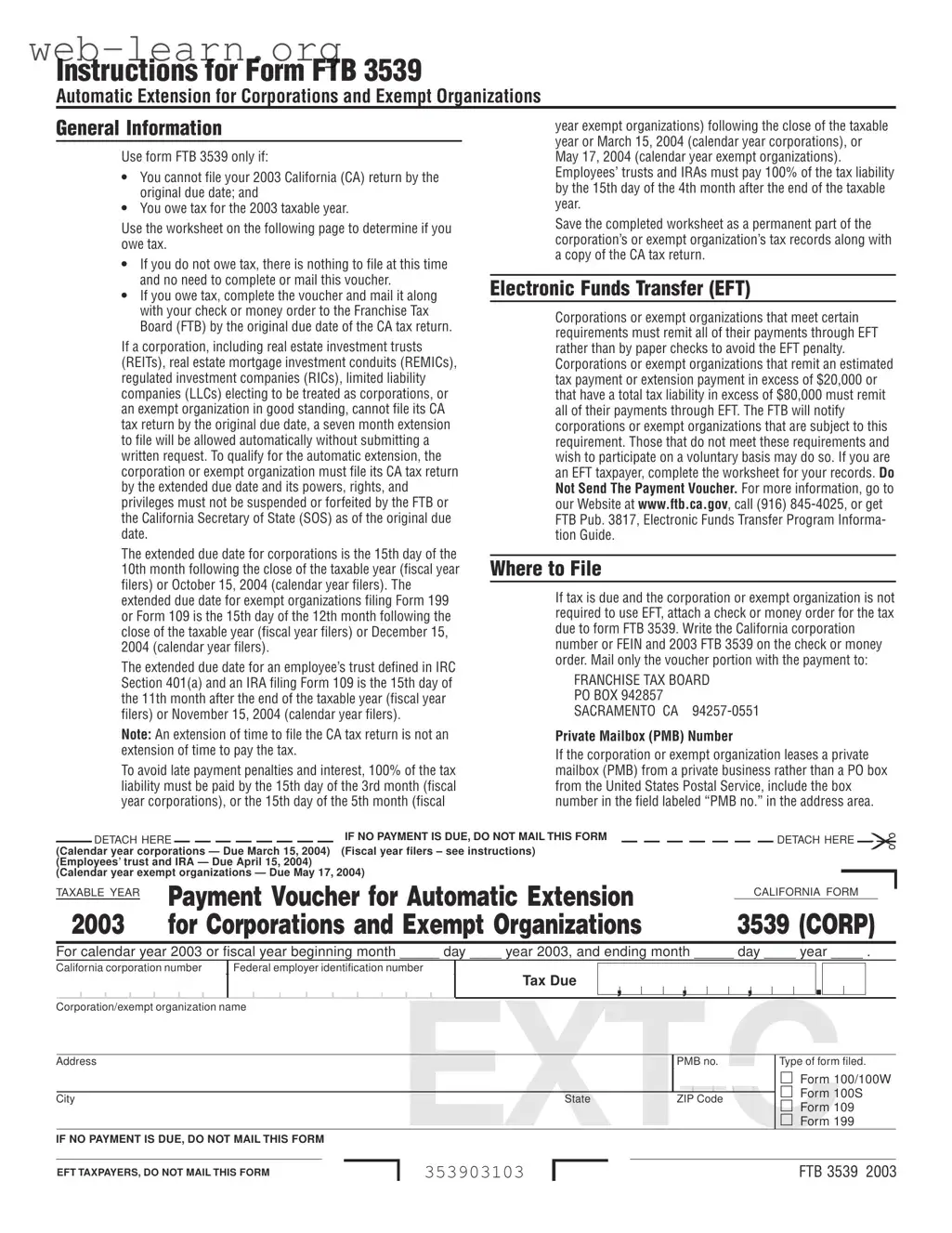

The California Form 3539 serves as a vital tool for corporations and exempt organizations seeking an automatic extension for filing their state tax returns. This form is specifically designed for those who are unable to meet the original filing deadline due to various circumstances. By submitting Form 3539, eligible entities can secure a seven-month extension to file their California tax return, provided they adhere to certain requirements. Notably, this extension does not apply to tax payments, which must still be made by the original due date to avoid penalties and interest. For organizations that owe tax, completing the payment voucher and remitting it along with the appropriate payment is essential. The form also outlines specific guidelines for different types of filers, including corporations, real estate investment trusts, and exempt organizations, each with their own deadlines and tax obligations. Furthermore, the form highlights the necessity for electronic funds transfer for certain entities, ensuring compliance with California’s tax regulations. Understanding these components is crucial for maintaining good standing with the Franchise Tax Board and avoiding potential penalties.

| Fact Name | Description |

|---|---|

| Purpose | The California Form FTB 3539 is used to request an automatic extension for filing tax returns for corporations and exempt organizations. |

| Eligibility | Only corporations and exempt organizations that cannot file their tax return by the original due date and owe tax can use this form. |

| Due Dates | For calendar year corporations, the due date is March 15. Exempt organizations have a due date of May 17. |

| Payment Requirement | Tax liabilities must be paid by the original due date to avoid penalties. If no tax is owed, there is no need to file the form. |

| EFT Requirement | Corporations with a tax liability over $80,000 must pay via Electronic Funds Transfer (EFT) to avoid penalties. |

| Governing Law | The use of Form FTB 3539 is governed by California Revenue and Taxation Code sections relevant to corporate tax filings. |

Filling out the California 3539 form is a straightforward process that requires careful attention to detail. Once you have completed the form, it will need to be submitted along with your payment if applicable. Be sure to check your entries for accuracy to avoid any potential penalties or issues with your tax return.

What is the purpose of the California 3539 form?

The California 3539 form is used to request an automatic extension for corporations and exempt organizations that cannot file their California tax return by the original due date. This form allows eligible entities to extend their filing deadline without needing to submit a written request.

Who should use the California 3539 form?

This form should be used by corporations and exempt organizations that owe taxes for the taxable year and cannot file their tax return by the original due date. If an organization does not owe tax, there is no need to file this form.

When is the California 3539 form due?

The due date for filing the California 3539 form varies based on the type of entity and its fiscal year. For calendar year corporations, the form is due on March 15, while exempt organizations have a due date of May 17. For fiscal year filers, the extended due date is the 15th day of the 10th month following the close of the taxable year.

What happens if I fail to pay my taxes by the original due date?

If a corporation or exempt organization fails to pay its total tax by the original due date, a late payment penalty plus interest will be added to the tax due. It's crucial to pay 100% of the tax liability by the specified deadlines to avoid these penalties.

Are there any penalties for not filing the California 3539 form?

Yes, if the corporation or exempt organization does not file its tax return by the extended due date, or if its powers, rights, and privileges have been suspended or forfeited, a delinquency penalty plus interest will be assessed from the original due date. Additionally, a 10% non-compliance penalty may apply if required payments are not made through Electronic Funds Transfer (EFT).

How do I determine if I owe taxes?

To determine if you owe taxes, complete the Tax Payment Worksheet included with the California 3539 form. This worksheet will guide you through calculating your total tentative tax and any estimated tax payments you may have made. If your tentative tax exceeds your payments, you have tax due.

What should I include with the California 3539 form if I owe taxes?

If you owe taxes, complete the form and include a check or money order for the tax due. Ensure that you write your California corporation number or Federal Employer Identification Number (FEIN) on the payment. Only the voucher portion of the form should be mailed with your payment to the Franchise Tax Board (FTB).

What if I am part of a combined unitary group?

In a combined unitary group, only the designated key corporation should submit the California 3539 form if filing a combined return. This key corporation must include payment for the minimum franchise tax for each corporation in the group that is subject to this tax. If members intend to file separately, each member must submit its own form if there is tax due.

Where can I find more information about the California 3539 form?

For more information, you can visit the Franchise Tax Board's website at www.ftb.ca.gov or call their customer service at (916) 845-4025. Additionally, you may refer to FTB Pub. 3817, which provides guidance on the Electronic Funds Transfer Program.

Filling out the California Form FTB 3539 can be a straightforward process, but many individuals make common mistakes that can lead to complications. One frequent error is not filing the form on time. The deadline for submitting the form depends on whether the organization operates on a calendar or fiscal year. Missing this deadline can result in penalties and interest, which can be avoided by being diligent about the due date.

Another mistake is failing to pay the full tax liability by the original due date. Even if an extension is granted for filing the return, it does not extend the time to pay taxes owed. Organizations must ensure that they pay 100% of their tax liability by the required date to avoid late payment penalties. This is a critical point that many overlook, thinking that an extension gives them more time to pay.

Some individuals incorrectly assume that they do not owe tax and thus do not need to file the form. If there is any tax due, the form must be completed and submitted. It’s essential to use the worksheet provided with the form to determine if any tax is owed. Ignoring this step can lead to unnecessary complications down the line.

Another common error is neglecting to include the correct information on the payment voucher. Organizations must ensure that they include their California corporation number or Federal Employer Identification Number (FEIN) on the check or money order. Omitting this information can delay processing and lead to confusion about the payment.

Additionally, some filers do not keep a copy of the completed worksheet and the submitted form for their records. This is important because having these documents can help resolve any future issues with the Franchise Tax Board. Maintaining accurate records is essential for any organization.

Lastly, failing to understand the requirements for Electronic Funds Transfer (EFT) can lead to errors. Corporations that meet certain thresholds must remit all payments through EFT. Those who do not comply may face a non-compliance penalty. It’s crucial to be aware of these requirements and plan accordingly to avoid unnecessary penalties.

When dealing with the California 3539 form, several other documents often accompany it to ensure compliance with state tax regulations. Understanding these forms can help streamline the filing process and avoid potential penalties. Below is a list of key documents that may be used alongside the California 3539 form.

By familiarizing yourself with these forms, you can navigate the complexities of California tax regulations more effectively. Each document plays a vital role in ensuring that corporations and exempt organizations meet their filing obligations and avoid unnecessary penalties. Always keep these forms handy during the tax season to ensure a smooth filing process.

The California Form FTB 3539 is an important document for corporations and exempt organizations seeking an automatic extension to file their tax returns. Several other forms share similar functions or requirements. Here’s a list of eight documents that are similar to the California 3539 form, along with a brief explanation of how they are alike:

Understanding these forms can help ensure compliance with tax obligations and avoid unnecessary penalties. Always check the specific requirements for each form to ensure proper filing.

When filling out the California 3539 form, there are specific actions you should take and avoid to ensure a smooth process. Here’s a list of what to do and what not to do:

Following these guidelines will help you navigate the California 3539 form more effectively.

Understanding the California Form 3539 can be challenging, especially with the various rules and requirements involved. Here are some common misconceptions that can lead to confusion:

Many believe that only corporations need to file Form 3539. However, exempt organizations are also required to use this form if they owe taxes.

Some assume that filing this form grants an extension for tax payments. In reality, it only extends the time to file the return, not to pay any taxes owed.

It's a common belief that taxes must be paid when submitting Form 3539. If you do not owe any taxes, there is no need to file or pay anything at that time.

Some think that Form 3539 is only applicable for the current tax year. In fact, it can be used for prior years if certain conditions are met.

Many people believe that Form 3539 can be filed at any time. However, it must be submitted by the original due date of the tax return to qualify for the extension.

There is a misconception that all corporations and exempt organizations are required to file electronically. Only those meeting specific criteria must use electronic funds transfer.

Some think that filing an extension with the IRS negates the need to file Form 3539. However, California has its own requirements, and filing with the IRS does not automatically extend your California filing deadline.

By clarifying these misconceptions, individuals and organizations can better navigate the complexities of tax filing in California. Understanding the rules surrounding Form 3539 can help ensure compliance and avoid unnecessary penalties.

Here are some key takeaways about filling out and using the California 3539 form: