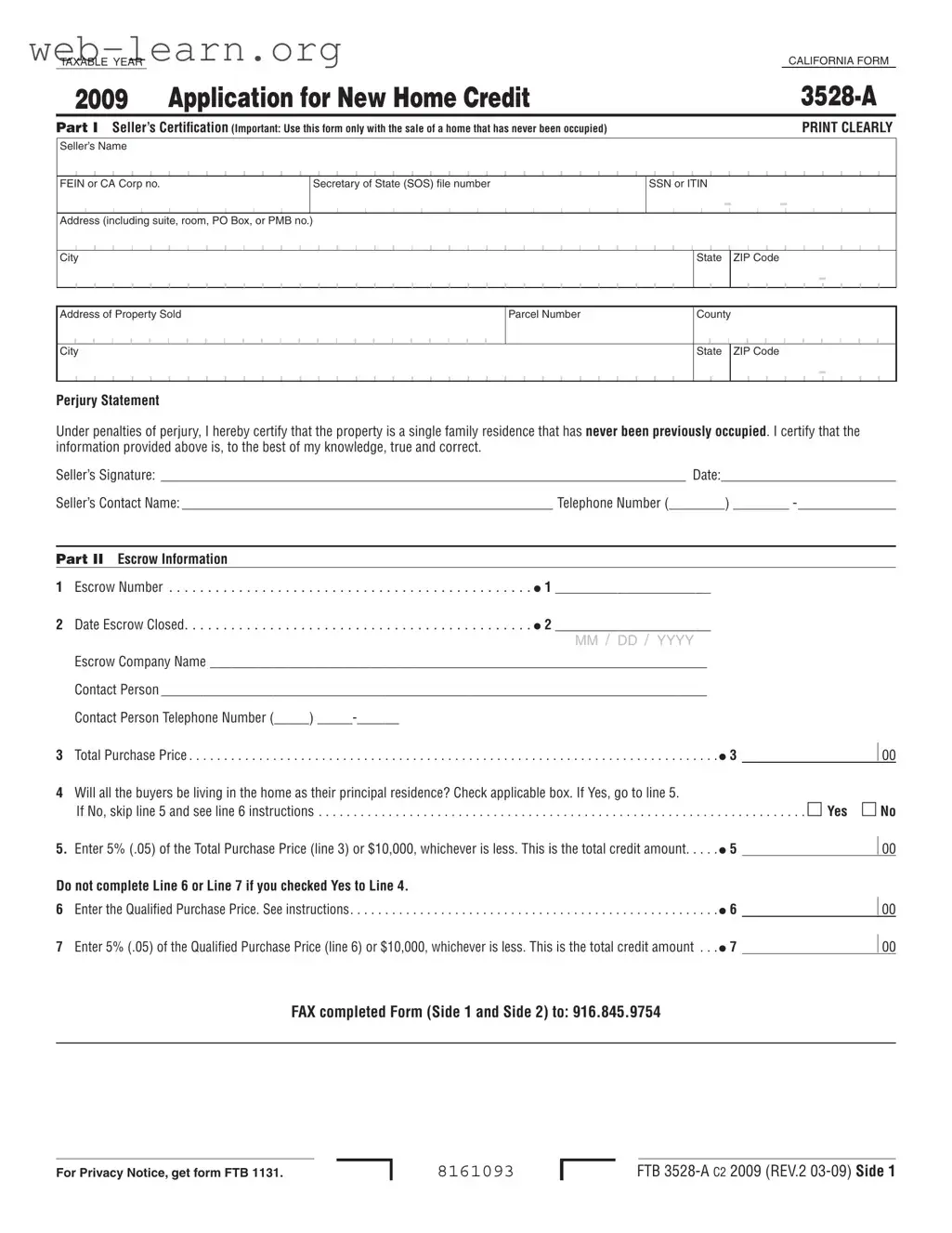

The California 3528 A form, officially known as the Application for New Home Credit, is a critical document for individuals purchasing a newly constructed home that has never been occupied. This form is specifically designed for transactions occurring between March 1, 2009, and March 1, 2010. It enables eligible buyers to claim a tax credit against their net tax, equal to 5% of the purchase price or a maximum of $10,000, whichever is lower. The form consists of several parts, including a Seller’s Certification, which requires the seller to affirm that the property is a single-family residence that has not been previously occupied. Buyers must complete their sections, providing personal information and confirming their intent to occupy the home as their principal residence for a minimum of two years. Escrow information is also required, detailing the escrow number, closing date, and total purchase price. Proper completion and timely submission of the form to the Franchise Tax Board (FTB) are essential for claiming the credit. Failure to adhere to these guidelines can result in the loss of potential tax benefits.

| Fact Name | Details |

|---|---|

| Purpose | The California Form 3528-A is used to apply for the New Home Credit for the sale of a home that has never been occupied. |

| Eligibility | Only sellers of new homes can use this form. The buyer must intend to live in the home as their principal residence for at least two years. |

| Credit Amount | The credit is equal to 5% of the purchase price or $10,000, whichever is less. This credit cannot be carried over to future years. |

| Governing Law | The form is governed by the California Revenue and Taxation Code (R&TC) Section 17059. |

Filling out the California 3528 A form is a straightforward process, but it requires attention to detail to ensure accuracy. This form is necessary for individuals selling a new home that has never been occupied. Once the form is completed, it will be submitted to the Franchise Tax Board (FTB) to apply for the New Home Credit. Below are the steps to guide you through filling out the form.

After completing the form, it is essential to fax it to the FTB at 916.845.9754 within one week of closing escrow. A copy should also be provided to the buyer. Ensure that all information is accurate and clearly written to avoid any delays in processing.

The California 3528 A form, also known as the Application for New Home Credit, is a document used to apply for a tax credit when selling a new home that has never been occupied. This form is specifically designed for sellers who are selling a single-family residence to eligible buyers who intend to use the property as their principal residence.

Eligibility for using the 3528 A form is limited to sellers of new homes that have never been occupied. Buyers must also qualify as individuals who intend to live in the home for at least two years as their principal residence. The credit is available for sales occurring between March 1, 2009, and March 1, 2010.

In Part I, the seller must provide their name, address, and identification number (such as SSN or ITIN). Additionally, the seller certifies that the property being sold is a single-family residence that has never been occupied. This section must be signed and dated by the seller to validate the information provided.

Part II requires details about the escrow process, including the escrow number, the date escrow closed, and the name of the escrow company. Sellers must also provide the total purchase price of the home and indicate whether all buyers will be living in the home as their principal residence. This section helps establish the transaction's legitimacy and eligibility for the credit.

If not all buyers will be living in the home as their principal residence, the seller must skip to line 6 to calculate the qualified purchase price. This requires determining the ownership percentages of only those buyers who will occupy the home. The credit will then be based on this adjusted figure.

The credit amount is determined by calculating 5% of the total purchase price or $10,000, whichever is less. If all buyers will occupy the home, the seller can directly enter the credit amount. If not, the qualified purchase price must be calculated first, and then 5% of that amount will be taken or the $10,000 limit will apply.

Once the form is completed, the escrow person must fax the form to the Franchise Tax Board (FTB) within one week of the close of escrow. A copy should also be provided to the buyer. The FTB will process the application on a first-come, first-served basis, and sellers will receive confirmation regarding the allocation of the tax credit.

No, the credit cannot be carried over to future years. It must be claimed on a timely filed tax return for the year in which the purchase of the qualified principal residence is made. The credit is nonrefundable and cannot reduce regular tax below the tentative minimum tax.

Filling out the California Form 3528-A can be a straightforward process, but many people make common mistakes that can lead to delays or complications. Understanding these pitfalls can help ensure that your application is processed smoothly.

One frequent error occurs in the Seller’s Certification section. Sellers often forget to provide complete and accurate information, such as their full name, address, and identification numbers. Omitting or incorrectly entering these details can cause significant delays in processing. It's crucial to double-check that all fields are filled out clearly and correctly.

Another common mistake involves the Escrow Information. Many applicants fail to enter the correct escrow number or the date escrow closed. This information is essential for tracking your application. If the escrow company does not provide this information accurately, it could lead to complications down the line.

Additionally, people often misinterpret the Principal Residence question. Some applicants mistakenly check "Yes" when they should select "No." This can lead to errors in calculating the credit amount. Understanding the definitions and requirements for a principal residence is vital to avoid this mistake.

In the calculation of the Total Purchase Price, errors frequently occur. Buyers sometimes miscalculate the total, either including or excluding certain fees. This can lead to incorrect credit amounts being claimed. Always ensure that you are using the correct figures as outlined in the instructions.

Furthermore, many applicants overlook the requirement to submit the form within one week after closing escrow. Failing to meet this deadline can result in losing the opportunity to claim the credit. Mark your calendar and set reminders to avoid this issue.

Finally, some individuals neglect to round their figures correctly. The instructions specify rounding cents to the nearest whole dollar. Errors in rounding can lead to discrepancies in the credit claimed. Pay careful attention to this detail to ensure accuracy.

By being aware of these common mistakes, you can navigate the process more effectively and increase your chances of a successful application. Take your time, review the form thoroughly, and don’t hesitate to seek assistance if needed.

The California Form 3528 A serves a specific purpose in facilitating tax credits for the sale of newly constructed homes that have never been occupied. However, several other forms and documents often accompany this form to ensure a smooth transaction and compliance with state regulations. Below is a list of commonly used documents in conjunction with the California 3528 A form.

In summary, the California 3528 A form is just one component of a broader set of documents necessary for a successful real estate transaction. Each document plays a vital role in ensuring compliance with state regulations and protecting the interests of all parties involved in the home buying process.

The California Form 3528-A is an important document used in real estate transactions, particularly for claiming the New Home Credit. Several other documents share similarities with this form, particularly in their purpose or the information they collect. Here is a list of eight documents that are similar to the California 3528-A form:

Each of these documents serves a specific purpose within the tax system, yet they share common elements with the California Form 3528-A, particularly in their focus on eligibility, certification, and the collection of personal and property-related information.

When filling out the California 3528 A form, it's essential to ensure accuracy and compliance. Here are seven important things to do and avoid during the process:

Misconceptions about the California 3528 A form can lead to confusion for both sellers and buyers. Here are eight common misconceptions along with clarifications:

Here are some key takeaways about filling out and using the California 3528 A form: