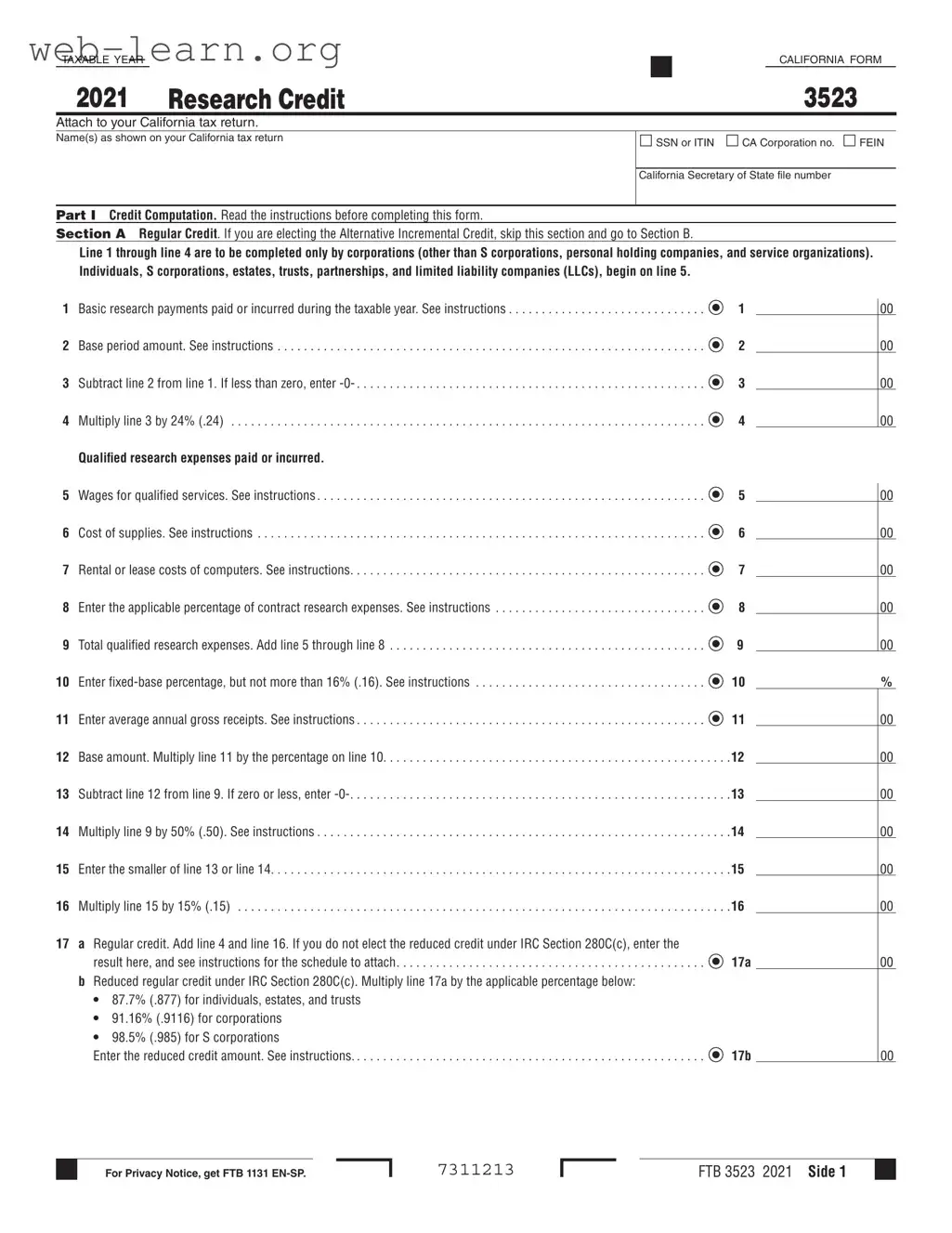

The California Form 3523 is a crucial document for businesses seeking to claim research credits on their state tax returns. This form is specifically designed for the taxable year 2020 and serves as a means for corporations and certain other entities to report their qualified research expenses. It includes two main sections: the Regular Credit and the Alternative Incremental Credit. In the Regular Credit section, businesses calculate their basic research payments and determine their eligible expenses, which can include wages, supplies, and rental costs related to research activities. The Alternative Incremental Credit section provides an alternative pathway for claiming credits, particularly beneficial for those who may not qualify under the regular provisions. Additionally, the form requires entities to provide their identification details, such as Social Security Numbers or Federal Employer Identification Numbers, ensuring proper tracking and compliance. Completing this form accurately can lead to significant tax savings, making it an essential part of the financial planning process for businesses engaged in research and development in California.

| Fact Name | Detail |

|---|---|

| Purpose | The California 3523 form is used to claim the Research Credit for qualified research expenses on the California tax return. |

| Eligibility | Corporations, individuals, S corporations, estates, trusts, partnerships, and LLCs can complete this form, depending on the section. |

| Sections | The form includes two main sections: Section A for Regular Credit and Section B for Alternative Incremental Credit. |

| Credit Calculation | The credit is calculated based on qualified research expenses, with different methods outlined for corporations and individuals. |

| Governing Law | This form is governed by California Revenue and Taxation Code Section 23609. |

| Filing Requirement | Taxpayers must attach the completed 3523 form to their California tax return when claiming the research credit. |

Filling out the California 3523 form involves a series of steps that require accurate information about your research credits. Ensure you have all necessary documents and figures ready before starting the process. Follow the steps below to complete the form correctly.

Once you have filled out the form, review all entries for accuracy. Attach the completed form to your California tax return and ensure you keep copies for your records. If you have any questions or need further assistance, consider consulting a tax professional.

The California 3523 form is used to claim the Research Credit for the taxable year. This form is specifically designed for businesses engaging in qualified research activities in California. By completing this form, eligible taxpayers can reduce their state tax liability based on their research expenditures.

Corporations, individuals, S corporations, estates, trusts, partnerships, and limited liability companies (LLCs) that have incurred qualified research expenses during the taxable year should consider filing this form. However, it’s important to note that certain entities, such as personal holding companies and service organizations, may not be eligible.

Qualified research expenses include costs associated with basic research payments, wages for qualified services, costs of supplies, and rental or lease costs of computers used in research activities. These expenses must be directly related to the research conducted to qualify for the credit.

The Regular Credit is calculated based on a percentage of the increase in qualified research expenses compared to a base period amount. In contrast, the Alternative Incremental Credit allows taxpayers to claim a credit based on a percentage of their qualified research expenses without needing to establish a base period. Taxpayers must choose one method to claim their credit and cannot use both.

To calculate the Research Credit, taxpayers must complete the relevant sections of the form based on their chosen credit method. For the Regular Credit, follow the steps outlined in Section A, while for the Alternative Incremental Credit, complete Section B. Each section provides specific lines to fill out based on your qualified research expenses and other relevant financial information.

IRC Section 280C(c) allows taxpayers to elect a reduced credit amount if they have received a federal tax deduction for the same research expenses. This section provides a percentage to apply to the calculated credit, which may be beneficial for some taxpayers, depending on their overall tax situation.

Yes, if you have unused research credits, you can carry them over to future tax years. The California 3523 form includes a section for calculating credit carryovers, allowing you to apply any remaining credits against your tax liability in subsequent years.

When filing the California 3523 form, you must attach it to your California tax return. Additionally, any supporting documentation that verifies your qualified research expenses should be kept on file in case of an audit. While not required to be submitted with the form, having this documentation ready is crucial for substantiating your claim.

For more detailed information, including instructions for completing the form, you can visit the California Franchise Tax Board's official website. They provide resources, guidelines, and contact information for any questions you may have regarding the Research Credit and the California 3523 form.

Filling out the California 3523 form can be a daunting task, and many individuals make common mistakes that can lead to delays or rejections. One frequent error is not reading the instructions thoroughly before starting. The form contains specific guidelines that are essential for accurate completion. Skipping this step can result in miscalculations or missing information.

Another common mistake is failing to provide the correct identification numbers. Individuals often overlook the need to include their Social Security Number (SSN) or Individual Taxpayer Identification Number (ITIN), while corporations must ensure their California Corporation number or Federal Employer Identification Number (FEIN) is accurate. Missing or incorrect identification can lead to processing issues.

Many people also struggle with the credit computation sections. For example, in Section A, Line 1 through Line 4 should only be filled out by corporations, but individuals and other entities mistakenly complete these lines. Understanding which sections apply to your specific entity type is crucial for correct submission.

Another area where errors occur is in the calculations. When subtracting values or multiplying percentages, simple arithmetic mistakes can lead to incorrect figures. This is particularly important in lines that involve multiplying by percentages, such as Line 4 and Line 16. Taking the time to double-check these calculations can prevent unnecessary complications.

Additionally, individuals often forget to include all relevant qualified research expenses. Lines 5 through 8 require detailed entries for wages, supplies, and other costs. Omitting any of these can result in an inaccurate total on Line 9, affecting the overall credit amount.

Another mistake is not entering the average annual gross receipts correctly. Line 11 requires accurate reporting of gross receipts, which can be tricky. If this figure is incorrect, it can significantly impact the calculations that follow.

People also sometimes neglect to attach the required schedules. If you do not elect the reduced credit under IRC Section 280C(c), specific schedules must accompany the form. Failing to include these can delay processing or lead to disqualification from receiving the credit.

Finally, many individuals overlook the importance of reviewing their completed form before submission. A final check can catch any overlooked mistakes, such as missing signatures or incomplete lines. Taking this extra step can save time and ensure a smoother filing process.

The California Form 3523 is essential for claiming research credits on your tax return. However, it is often accompanied by various other forms and documents that help provide additional information or support your claims. Below is a list of these documents, each serving a unique purpose in the process.

Understanding these additional forms can help ensure a smooth and accurate filing process. Each document plays a critical role in supporting your claims and ensuring compliance with California tax laws. If you have questions about any of these forms, consider seeking assistance to clarify your needs and obligations.

The California Form 3523 is primarily used for claiming the Research Credit for taxable years. Several other documents serve similar purposes in different contexts. Below are four documents that share similarities with the California 3523 form:

When filling out the California Form 3523, there are several important guidelines to follow. Below is a list of things you should and shouldn't do:

Here is a list of misconceptions about the California 3523 form, along with clarifications for each:

Filling out the California 3523 form can be a crucial step for businesses seeking to claim research credits. Understanding its components is essential for accurate completion and effective use. Here are key takeaways regarding the form: