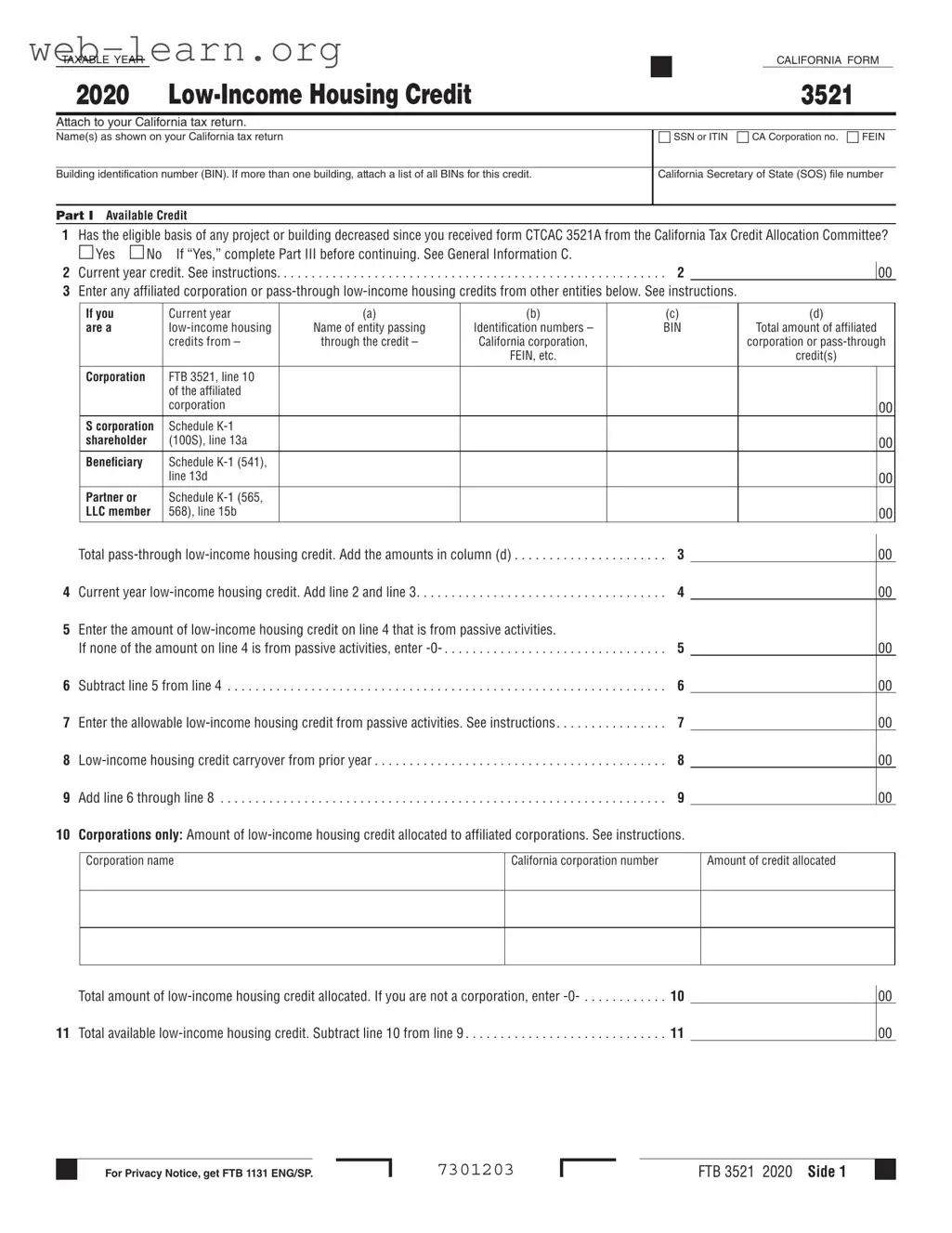

The California Form 3521 is an essential document for those claiming the Low-Income Housing Credit on their state tax returns. This form must be attached to your California tax return and includes crucial information about your eligibility and the credits available to you. It requires details such as your name, Social Security Number (SSN) or Individual Taxpayer Identification Number (ITIN), and building identification numbers (BINs) for any projects involved. The form breaks down available credits, allowing you to report current year credits, affiliated credits from other entities, and any carryover amounts from previous years. Additionally, if there has been a decrease in the eligible basis of any project, you will need to complete a specific section to recalculate your basis. Understanding how to accurately fill out this form can significantly impact your tax benefits, making it a vital part of the tax filing process for low-income housing projects in California.

| Fact Name | Details |

|---|---|

| Form Purpose | The California Form 3521 is used to claim the Low-Income Housing Credit for eligible projects. |

| Governing Law | This form is governed by California Revenue and Taxation Code Section 17058. |

| Filing Requirement | Taxpayers must attach Form 3521 to their California tax return to claim the credit. |

| Eligibility Criteria | To qualify, the project must meet specific low-income housing requirements set by the California Tax Credit Allocation Committee. |

| Credit Calculation | The credit amount is determined based on the eligible basis of the building and any applicable percentages. |

Completing the California Form 3521 requires careful attention to detail. This form is essential for reporting low-income housing credits on your California tax return. Once you have filled it out, ensure that you attach it to your tax return before submission.

What is the California Form 3521?

The California Form 3521 is used to claim the Low-Income Housing Credit for the taxable year. This form must be attached to your California tax return. It helps property owners and developers reduce their tax liability by providing credits for investing in low-income housing projects.

Who needs to file Form 3521?

Individuals or corporations that have invested in qualifying low-income housing projects must file Form 3521. If you have received a form CTCAC 3521A from the California Tax Credit Allocation Committee, you are likely eligible to claim this credit.

What information do I need to complete Form 3521?

You will need several pieces of information to complete the form, including:

What should I do if my project's eligible basis has decreased?

If the eligible basis of your project or building has decreased since you received Form CTCAC 3521A, you must complete Part III of the form. This section allows you to recalculate the basis and determine the allowable credit.

How do I calculate my current year low-income housing credit?

The current year low-income housing credit is calculated by adding the amounts from line 2 and line 3 of the form. Line 2 pertains to your current year credit, while line 3 includes any affiliated corporation or pass-through credits you may have received.

What is a carryover credit?

A carryover credit allows you to apply any unused low-income housing credit to future tax years. If you claim a credit but do not use the entire amount, you can carry over the remaining credit to offset taxes in subsequent years.

What do I do if I am not a corporation?

If you are not a corporation, you will need to enter -0- in the sections of the form that ask for corporation-specific information, such as the amount of low-income housing credit allocated to affiliated corporations. Ensure that you still complete the relevant sections for individual claimants.

Where can I find additional instructions for Form 3521?

Additional instructions for completing Form 3521 can be found in the official guidelines provided by the California Franchise Tax Board (FTB). These guidelines will help you navigate the form and ensure that you are claiming the correct amounts.

How do I submit Form 3521?

Form 3521 should be submitted along with your California tax return. Ensure that all sections of the form are completed accurately to avoid delays or issues with your tax filing.

Filling out the California Form 3521 can be a straightforward process, but many people make common mistakes that can lead to delays or issues with their tax returns. Understanding these pitfalls can help ensure that your application is completed correctly.

One frequent mistake is failing to provide accurate identification numbers. The form requires your Social Security Number (SSN) or Individual Taxpayer Identification Number (ITIN), as well as the California Corporation number or Federal Employer Identification Number (FEIN) if applicable. Omitting or incorrectly entering these numbers can lead to significant complications, including processing delays.

Another common error involves the building identification number (BIN). If you have more than one building, it’s essential to attach a list of all BINs associated with the credit. Neglecting to do this can result in the form being returned for correction, which can slow down the credit allocation process.

Many individuals also overlook the question regarding the decrease in the eligible basis of any project or building. If the answer is "Yes," it is crucial to complete Part III of the form before proceeding. Skipping this step can lead to inaccuracies in your credit calculation.

When it comes to calculating the current year credit, some filers forget to refer to the instructions. The instructions provide guidance on how to accurately determine the credit amount, and failing to follow them can lead to incorrect figures being reported on the form.

In the section for affiliated corporation or pass-through low-income housing credits, people often miscalculate or misreport the total amounts. It’s vital to ensure that the amounts in column (d) are accurately totaled, as any discrepancies can affect the final credit calculation.

Another mistake is related to the passive activities credit. Some filers do not correctly identify the amount of low-income housing credit that comes from passive activities. If none of the amount on line 4 is from passive activities, you should enter -0-. Not doing so can create confusion in your credit computation.

Additionally, when entering the allowable low-income housing credit from passive activities, some individuals forget to consult the instructions. This can lead to errors that affect the overall credit calculation, potentially resulting in a lower credit than you are entitled to.

Finally, corporations must be cautious when allocating credits to affiliated corporations. If you are not a corporation, it’s essential to enter -0- on line 10. Misunderstanding this requirement can lead to incorrect reporting, which may complicate your tax situation.

By being aware of these common mistakes, you can improve your chances of successfully completing the California Form 3521. Careful attention to detail and following the provided instructions can make a significant difference in ensuring your low-income housing credit is processed smoothly.

The California Form 3521 is specifically used for claiming the Low-Income Housing Credit. However, there are several other forms and documents that are commonly associated with this process. Understanding these documents can help ensure that all necessary information is provided and that the application process runs smoothly.

Each of these forms and documents plays a role in the overall process of claiming the Low-Income Housing Credit in California. Ensuring that all necessary paperwork is completed and submitted can help facilitate a smoother application process and improve the chances of a successful claim.

When filling out the California Form 3521, it is important to follow certain guidelines to ensure accuracy and compliance. Here’s a list of things to do and avoid:

Misconceptions about the California Form 3521 can lead to confusion and errors in tax reporting. Here are nine common misunderstandings:

When filling out and using the California 3521 form, consider the following key takeaways: