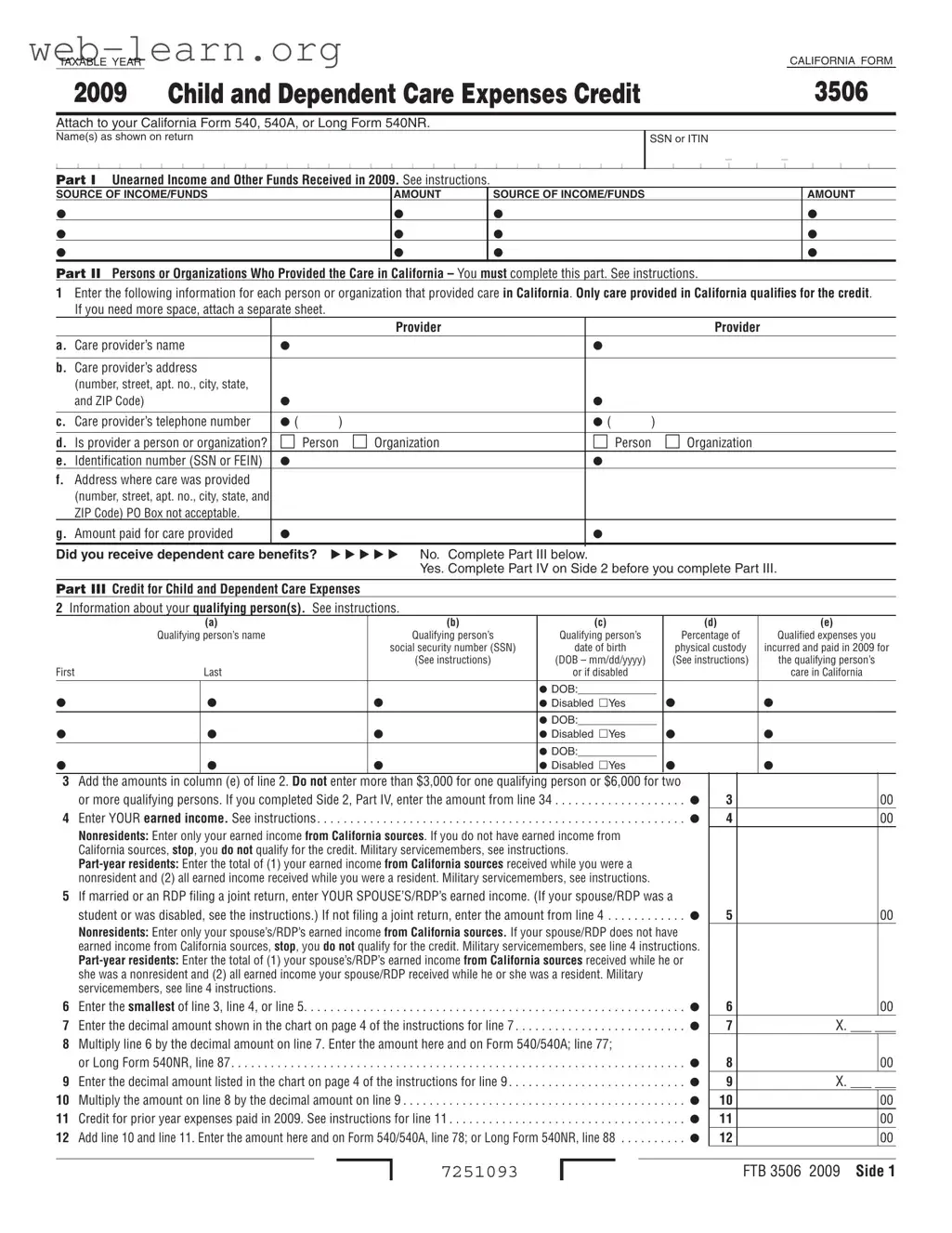

The California Form 3506 is a crucial document for taxpayers seeking to claim the Child and Dependent Care Expenses Credit. This form is specifically designed for individuals who have incurred expenses related to the care of qualifying persons, such as children or dependents, while they worked or looked for work. To successfully complete the form, it is necessary to provide detailed information about the care providers, including their names, addresses, and the amounts paid for care services. Additionally, the form requires taxpayers to report their earned income, which is essential for determining eligibility for the credit. It is important to note that only care provided in California qualifies for this credit. Taxpayers must also account for any dependent care benefits received, as these can affect the total credit amount. Completing the California Form 3506 accurately and thoroughly is vital, as it directly impacts the financial relief available to families managing childcare expenses.

| Fact Name | Details |

|---|---|

| Purpose | The California 3506 form is used to claim the Child and Dependent Care Expenses Credit for eligible taxpayers. |

| Eligibility | Taxpayers must have incurred qualifying child or dependent care expenses to work or look for work. |

| Filing Requirement | This form must be attached to California Form 540, 540A, or Long Form 540NR. |

| Income Limitations | The credit is limited to $3,000 for one qualifying person and $6,000 for two or more qualifying persons. |

| Care Provider Information | Taxpayers must provide details about the care provider, including their name, address, and identification number. |

| Dependent Care Benefits | If taxpayers received dependent care benefits, they must complete Part IV of the form. |

| Governing Law | The form is governed by California Revenue and Taxation Code Section 17052.6. |

Completing the California Form 3506 is an essential step for those seeking to claim the Child and Dependent Care Expenses Credit. This form must be attached to your California tax return, specifically Forms 540, 540A, or Long Form 540NR. Follow the steps below to accurately fill out the form.

After completing the form, attach it to your California tax return. Ensure that all necessary documentation is included to support your claims. Proper completion will facilitate the processing of your tax return and any credits you are eligible to receive.

What is the California 3506 form?

The California 3506 form is used to claim the Child and Dependent Care Expenses Credit. Taxpayers who have incurred expenses for the care of qualifying individuals while they work or look for work can use this form. It must be attached to California Form 540, 540A, or Long Form 540NR when filing taxes.

Who qualifies as a dependent for the credit?

A qualifying person typically includes a child under the age of 13 or a spouse or dependent who is physically or mentally incapable of self-care. The individual must live with the taxpayer for more than half the year, and the taxpayer must have incurred expenses related to their care in California.

What types of care expenses can be claimed?

Eligible expenses include payments made to care providers for services rendered while the taxpayer is working or seeking work. This can include daycare centers, babysitters, and other childcare services. However, expenses must have been paid for care provided in California to qualify for the credit.

How is the credit calculated?

The credit amount is determined by calculating the total qualifying expenses incurred, which is limited to $3,000 for one qualifying person and $6,000 for two or more. The taxpayer's earned income and that of their spouse (if filing jointly) are also considered. The smallest of these amounts, along with specific percentages from the tax tables, will determine the final credit amount.

Do I need to provide information about my care provider?

Yes, the form requires detailed information about each care provider, including their name, address, and identification number (such as a Social Security Number or Federal Employer Identification Number). This information is necessary to verify the legitimacy of the care expenses claimed.

What if I received dependent care benefits?

If the taxpayer received dependent care benefits through an employer, this must be reported on the form. The benefits will affect the calculation of the credit, and taxpayers must complete a separate section (Part IV) of the form to account for these benefits.

Can I claim expenses incurred in previous years?

Expenses from a previous year can only be claimed if they were paid in the current tax year and if the taxpayer did not previously claim the credit for those expenses. Specific instructions for handling prior year expenses are provided in the form guidelines.

What should I do if I have more questions about the form?

For additional questions or clarification, taxpayers can refer to the instructions included with the California 3506 form. It is also advisable to consult a tax professional or the California Franchise Tax Board for personalized assistance.

Filling out the California 3506 form can be a straightforward process, but many people make common mistakes that can lead to delays or issues with their tax credits. One frequent error is failing to provide complete information about the care provider. This section requires the name, address, and identification number of the care provider. If any of this information is missing or incorrect, it can jeopardize your eligibility for the credit.

Another mistake is not accurately reporting the amounts paid for care. It's essential to enter the correct figures in the designated spaces. If you underestimate or overestimate the amount, it can affect the total credit you receive. Always double-check your math to ensure that the amounts add up correctly.

People often overlook the requirement that only care provided in California qualifies for the credit. If you include expenses for care received outside of California, those amounts will not be considered. This is a critical detail that can easily be missed, so it’s important to verify the location of the care provided.

Additionally, many filers forget to indicate whether the care provider is an individual or an organization. This distinction is vital for processing your application. Leaving this question unanswered can lead to confusion and potential delays in receiving your credit.

Another common pitfall occurs when individuals do not provide the correct Social Security Number (SSN) or Federal Employer Identification Number (FEIN) for the care provider. This information is essential for the tax authorities to verify the legitimacy of the care provider. Without accurate identification numbers, the processing of your form may be stalled.

Lastly, some people fail to read the instructions thoroughly, which can lead to a variety of errors. Each section of the form has specific guidelines that must be followed. Ignoring these instructions can result in incomplete or incorrect submissions. Taking the time to read the guidelines can save you from unnecessary headaches later on.

When filing taxes in California, particularly when claiming the Child and Dependent Care Expenses Credit using the California 3506 form, several other documents may be required to support your application. Each of these documents serves a specific purpose and can help ensure that your tax return is accurate and complete. Below is a list of commonly used forms and documents that often accompany the California 3506 form.

Gathering these documents can help facilitate a smoother tax filing process. Each form and piece of documentation plays a role in substantiating your claims and ensuring compliance with California tax laws. Always consider consulting with a tax professional if you have questions or need assistance in preparing your tax return.

The California Form 3506 is used to claim the Child and Dependent Care Expenses Credit. Several other tax documents serve similar purposes in different contexts. Below is a list of eight documents that share similarities with Form 3506:

When filling out the California 3506 form, it is crucial to follow specific guidelines to ensure accuracy and compliance. Here are seven important dos and don'ts:

Understanding the California Form 3506 can be challenging, and several misconceptions may lead to confusion. Below are some common misunderstandings regarding this form:

This is not true. The form applies to any taxpayer who incurs child and dependent care expenses for qualifying individuals, which can include older children and dependents with disabilities.

Only care provided by eligible individuals or organizations qualifies for the credit. The care must be provided in California, and specific information about the provider must be included on the form.

Your earned income is a crucial factor in determining eligibility for the credit. The form requires you to report your income, and the credit amount is limited based on your earnings.

The credit is not automatic. You must complete the form and attach it to your California tax return to claim the credit. Failing to do so means you will not receive the benefit.

Expenses must be incurred in the taxable year for which you are filing. The form specifically asks for expenses incurred in the year stated on the form, so it is essential to keep accurate records.

Non-residents can only claim the credit if they have earned income from California sources. If you do not meet this criterion, you will not qualify for the credit.

Here are key takeaways about filling out and using the California 3506 form: