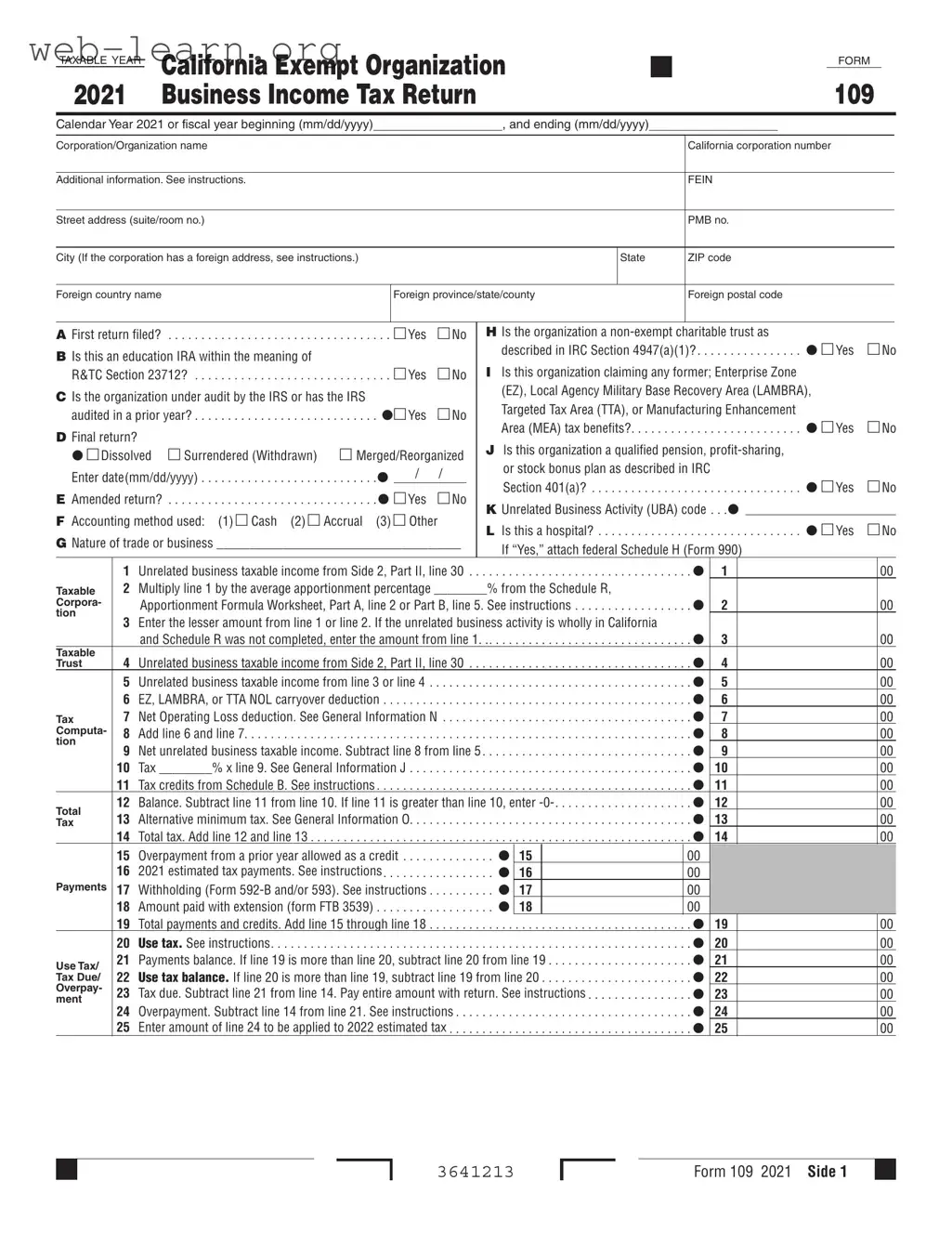

The California Form 109 is an essential document for organizations operating within the state that are classified as exempt entities. It serves as the California Exempt Organization Business Income Tax Return, specifically designed for the reporting of unrelated business income. This form is crucial for organizations that engage in activities not directly related to their exempt purposes, as it helps determine any tax liabilities stemming from those activities. The form includes various sections that require organizations to provide their basic information, such as their name, address, and federal employer identification number (FEIN). Additionally, it prompts organizations to indicate if they are filing their first return, claiming specific tax benefits, or undergoing an audit by the IRS. The form also addresses different accounting methods and includes sections for reporting unrelated business taxable income, deductions, and applicable tax credits. Organizations must carefully navigate the various schedules attached to the form, which detail income sources, deductions, and apportionment formulas necessary for accurate reporting. Understanding the nuances of Form 109 is vital for compliance and ensuring that organizations meet their tax obligations while maximizing their benefits under California law.

| Fact Name | Fact Description |

|---|---|

| Purpose | The California 109 form is used by exempt organizations to report unrelated business income and calculate any applicable taxes for the taxable year. |

| Taxable Year | The form can be completed for either the calendar year or a fiscal year, which must be specified at the top of the document. |

| Filing Requirement | Organizations must file this form if they have any unrelated business taxable income, as defined by the Internal Revenue Code. |

| Governing Laws | This form is governed by the California Revenue and Taxation Code, specifically under Sections 23701g, 23701i, and 23701n. |

| Non-Exempt Status | Organizations must indicate if they are a non-exempt charitable trust, which affects their tax obligations and filing requirements. |

| Amendments | If an organization needs to correct a previously filed return, they can indicate this by checking the 'Amended return' box on the form. |

Filling out the California 109 form requires careful attention to detail. It’s important to gather all necessary information before you start. This form is crucial for organizations to report their taxable income and related details for the year. Follow the steps below to complete the form accurately.

The California Form 109 is a tax return specifically designed for exempt organizations, including charities and non-profits, to report their unrelated business income. This form allows these organizations to comply with California tax regulations while ensuring that they accurately report any income that may be subject to taxation.

Organizations that are classified as tax-exempt under federal law but engage in unrelated business activities must file Form 109. If your organization generates income from activities that are not substantially related to its exempt purpose, you will need to report that income using this form.

Form 109 requires various pieces of information, including:

Accurate and complete information is crucial to ensure compliance and avoid potential penalties.

Typically, Form 109 must be filed by the 15th day of the 5th month after the end of the organization’s taxable year. For organizations operating on a calendar year, this means the deadline is May 15. If the deadline falls on a weekend or holiday, it is extended to the next business day.

Yes, if an organization discovers an error after filing Form 109, it can submit an amended return. This is done by marking the box indicating that it is an amended return and providing the corrected information. It’s important to file the amendment as soon as possible to avoid penalties.

Failing to file Form 109 can lead to significant consequences, including penalties and interest on any unpaid taxes. Additionally, the organization may lose its tax-exempt status if it consistently fails to comply with tax filing requirements. It’s crucial for organizations to meet their filing obligations to maintain their exempt status and avoid financial repercussions.

Completing the California 109 form can be a daunting task, and many people make common mistakes that can lead to delays or penalties. One frequent error occurs when individuals fail to provide accurate information about their organization. This includes incorrect names, addresses, or tax identification numbers. Such inaccuracies can cause significant issues, including the potential for miscommunication with tax authorities.

Another common mistake is neglecting to indicate whether the organization is filing its first return. Marking this box incorrectly can lead to confusion regarding the organization's status and tax obligations. It is crucial to ensure that this section is completed accurately to avoid complications.

Many filers also overlook the importance of selecting the correct accounting method. The California 109 form allows for cash, accrual, or other methods. Choosing the wrong method can affect the reported income and, consequently, the tax liability. Therefore, it is essential to review the accounting methods carefully before making a selection.

In addition, some individuals mistakenly assume that they do not need to attach additional schedules or documents when required. For example, if the organization is a hospital, it must include federal Schedule H. Failing to provide necessary attachments can result in the return being deemed incomplete, leading to delays in processing.

Another pitfall is related to the calculation of unrelated business taxable income. Many filers miscalculate this figure, either by not including all relevant income sources or by incorrectly applying deductions. This error can significantly impact the overall tax liability and should be approached with caution.

Furthermore, it is not uncommon for individuals to misreport tax credits. The California 109 form allows for various credits, but failing to calculate or report these accurately can lead to overpayment or underpayment of taxes. Filers should ensure they understand the credits available and how to apply them correctly.

People also often forget to sign and date the form. An unsigned return is considered invalid and may lead to penalties or rejection by the tax authorities. It is a simple yet critical step that should not be overlooked.

Lastly, many filers fail to keep copies of their completed forms and supporting documents. This can create problems if questions arise later or if the organization is audited. Maintaining thorough records is essential for future reference and compliance.

The California 109 form is an essential document for organizations that need to report their business income for tax purposes. Along with this form, several other documents may be required to ensure compliance and accuracy in reporting. Below is a list of commonly used forms and documents that complement the California 109 form, each serving a specific purpose in the tax reporting process.

In summary, these additional forms and schedules work in conjunction with the California 109 form to provide a comprehensive view of an organization’s financial activities. By carefully preparing and submitting these documents, organizations can ensure they meet tax obligations while maximizing potential benefits.

When filling out the California 109 form, here are nine important things to do and avoid:

Misconception 1: The California 109 form is only for for-profit organizations.

In reality, this form is specifically designed for exempt organizations, including non-profits. It helps them report unrelated business taxable income, which is important for maintaining their tax-exempt status.

Misconception 2: Filing the California 109 form is optional for all organizations.

This is not true. If an exempt organization has unrelated business income, it is required to file the California 109 form. Failing to do so can lead to penalties and loss of tax-exempt status.

Misconception 3: The form is the same as the federal 990 form.

While both forms serve similar purposes, they are distinct documents. The California 109 form is tailored to meet state requirements, whereas the federal 990 form is for federal tax reporting. Each has its own set of instructions and requirements.

Misconception 4: All income reported on the California 109 form is taxable.

This is misleading. Only unrelated business income is taxable. Income generated from the organization’s primary exempt activities is not subject to tax and should not be reported on this form.

Misconception 5: Once filed, the California 109 form cannot be amended.

In fact, organizations can file an amended return if they discover errors or need to make changes. It’s important to correct any mistakes to ensure compliance and maintain accurate records.

When filling out and using the California 109 form, organizations should keep the following key takeaways in mind: