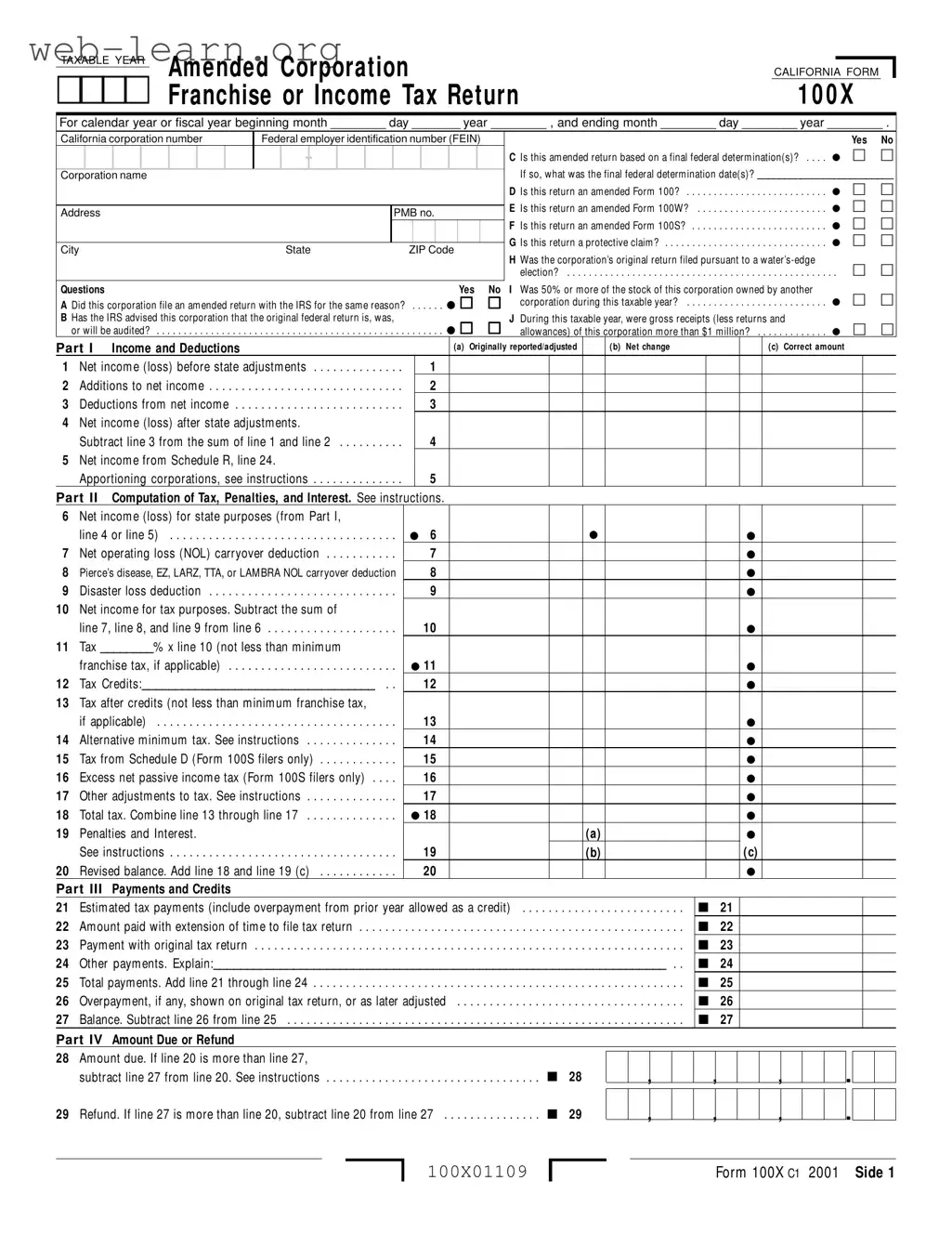

The California 100X form serves as a critical tool for corporations seeking to amend their previously filed tax returns. Designed specifically for California's franchise or income tax purposes, this form allows businesses to correct errors, report changes, or claim refunds related to their original tax filings. Corporations must indicate the taxable year for which they are amending their return, as well as provide essential identifying information, including their California corporation number and federal employer identification number (FEIN). The form contains a series of questions to determine the nature of the amendment, such as whether it is based on a final federal determination or if it is a protective claim. Additionally, it includes sections for reporting income, deductions, and any adjustments to tax liabilities, along with the computation of penalties and interest. The 100X form also requires a detailed explanation of the changes made, ensuring transparency and clarity in the amendment process. Understanding the nuances of this form is vital for corporations aiming to navigate California's tax landscape effectively and ensure compliance with state regulations.

| Fact Name | Details |

|---|---|

| Purpose of Form | The California 100X form is used to amend a previously filed Corporation Franchise or Income Tax Return (Form 100, 100W, or 100S). |

| Filing Deadline | Corporations must file Form 100X within four years from the original due date of the tax return or the date the tax return was filed, whichever is later. |

| Governing Law | This form is governed by the California Revenue and Taxation Code, particularly Sections 19306 and 23221. |

| Protective Claims | The form can be filed as a protective claim for refund, which allows corporations to claim a refund while certain issues are still under dispute. |

| IRS Changes | If the IRS makes changes to a corporation's federal return, those changes must be reported to the Franchise Tax Board (FTB) within six months of the final federal determination. |

| Minimum Franchise Tax | Even if a corporation has no tax liability, it may still be subject to a minimum franchise tax, which must be considered when filing. |

| Payment Instructions | If tax is due, checks should be made payable to the Franchise Tax Board, and the corporation number along with the taxable year should be noted on the payment. |

| Refund Process | Refunds should be mailed to the FTB at a designated address if the amended return results in an overpayment or no amount due. |

| Signature Requirement | The amended return must be signed by an authorized officer of the corporation, declaring the accuracy of the information provided. |

Filling out the California 100X form is an important step for corporations seeking to amend their previously filed tax returns. Completing this form accurately ensures that any changes to income, deductions, or credits are properly reported to the Franchise Tax Board. Below are the steps to guide you through the process of filling out the form.

What is the California 100X form?

The California 100X form is an amended corporation franchise or income tax return. Corporations use this form to correct errors or make changes to a previously filed Form 100, Form 100W, or Form 100S. It allows corporations to amend their tax filings for various reasons, including adjustments to income, deductions, or tax credits.

When should a corporation file the 100X form?

A corporation should file the 100X form after submitting its original tax return. The amended return must be filed within four years from the original due date, the date the tax return was filed, or within one year from the date the tax was paid, whichever is later. This ensures that any adjustments are made in a timely manner.

How does a corporation determine if it needs to file a 100X form?

If a corporation discovers that it made mistakes on its original tax return, it should consider filing a 100X form. Common reasons include changes in income, deductions, or credits that were not reported correctly. Additionally, if the IRS audits the original return and makes adjustments, the corporation must report these changes to the Franchise Tax Board (FTB) using the 100X form.

What information is required to complete the 100X form?

To complete the 100X form, a corporation must provide its California corporation number, federal employer identification number (FEIN), and details about the original return. This includes the taxable year, the corporation's name and address, and specific line items that are being amended. A clear explanation of the changes made must also be included.

Where should the 100X form be filed?

The filing location for the 100X form depends on whether there is an amount due or a refund. If the amended return results in a refund or no amount due, it should be mailed to:

If there is an amount due, the form should be sent to:

What should a corporation do if it disagrees with the IRS's adjustments?

If a corporation disagrees with the IRS's adjustments, it can file a protective claim using the 100X form. This claim allows the corporation to seek a refund while the dispute is being resolved. It is important to file this claim before the statute of limitations expires.

Are there penalties for not filing the 100X form when required?

Yes, failing to file the 100X form when necessary can result in penalties and interest. The FTB may assess penalties for underreporting income or failing to report changes made by the IRS. It is crucial to address any discrepancies promptly to avoid additional charges.

Can a corporation change its filing status using the 100X form?

No, the 100X form cannot be used to change a corporation's filing status, such as switching from a C corporation to an S corporation. To change the filing status, a different form, specifically Form FTB 3560, must be used.

What supporting documents are needed when filing the 100X form?

When filing the 100X form, corporations must attach any supporting documents that explain the changes made. This includes copies of federal schedules if changes were made to the federal return, as well as any other relevant forms and schedules that support the adjustments being reported.

Filling out the California 100X form can be a complex process. One common mistake is failing to check the correct boxes for the type of amended return being filed. This includes distinguishing between Form 100, Form 100W, and Form 100S. Not marking the appropriate box can lead to delays or rejections.

Another frequent error is neglecting to provide the correct California corporation number and Federal Employer Identification Number (FEIN). These numbers are crucial for identifying the corporation and linking the amended return to the original filing. Missing or incorrect numbers can cause significant processing issues.

Many individuals also forget to include an explanation of changes made in Part V. This section requires a detailed account of what has changed and why. Omitting this information can lead to questions from the Franchise Tax Board (FTB) and potentially slow down the processing of the return.

Some filers make the mistake of not attaching necessary supporting documents. If changes were made to the federal return, relevant schedules must accompany the 100X form. Failure to provide these documents can result in the return being deemed incomplete.

Additionally, errors in calculating the amounts in columns (a), (b), and (c) are common. These columns require precise figures based on previous returns and adjustments. Miscalculations can lead to incorrect tax liabilities, which may trigger further penalties or interest.

Another issue arises when taxpayers do not sign the form. Both the officer of the corporation and the preparer must sign the return. A missing signature can result in the return being rejected by the FTB.

Some individuals also overlook the deadlines for filing the amended return. The 100X must be submitted within a specific timeframe after the original return has been filed. Missing this deadline can forfeit the right to claim a refund.

Furthermore, failing to indicate whether the amended return is based on a final federal determination can complicate matters. This information helps the FTB understand the context of the changes being made.

Lastly, some filers neglect to double-check their mailing addresses. If the return is sent to the wrong address, it can lead to delays or miscommunication. Ensuring that the correct address is used is vital for timely processing.

The California 100X form is an essential document for corporations seeking to amend their previously filed tax returns. Alongside this form, several other documents may also be required to ensure a complete and accurate filing. Below is a list of commonly used forms and documents that often accompany the California 100X form.

Each of these forms plays a vital role in the amendment process, ensuring that all financial information is accurately reported and that the corporation complies with both state and federal tax regulations. Careful attention to detail is essential when completing these documents.

Things to Do When Filling Out the California 100X Form:

Things Not to Do When Filling Out the California 100X Form:

This is incorrect. The 100X form is specifically for amending a previously filed tax return, not for changing the corporate filing status. For status changes, a different form must be used.

Not necessarily. Filing the 100X may lead to a refund if an overpayment is identified, but it does not guarantee one. The refund is contingent on the specifics of the amendment.

This is a common misunderstanding. The 100X should only be filed after the original return has been submitted and processed. There is a specific timeframe for filing amendments.

This is false. If the 100X is filed after the deadline, penalties may apply. It is essential to adhere to the filing timelines to avoid unnecessary fees.

This is incorrect. The 100X form is solely for California state tax returns. For federal amendments, a different form, such as the 1120X, should be used.

This is a misconception. It is required to provide detailed explanations for any changes made on the amended return. This helps clarify the reasons for the amendment.

As of now, the 100X form must be filed by mail. Electronic filing is not an option for this specific form, so ensure it is sent to the correct address.

This is not true. The FTB reviews all amendments and may request additional information or clarification before accepting the changes.

This is misleading. There are strict deadlines for filing the 100X. Generally, it must be filed within four years from the original due date or the date the return was filed, whichever is later.

The California 100X form is specifically designed for corporations that need to amend a previously filed California Corporation Franchise or Income Tax Return. This includes Forms 100, 100W, and 100S.

Filing the 100X form is essential if there were changes to the corporation's income, deductions, or any other relevant information that affects the tax liability.

Corporations must file the 100X within four years from the original due date of the tax return or the date the tax was paid, whichever is later. This is crucial to ensure that claims for refunds are valid.

When filling out the form, be sure to provide detailed explanations for any changes made. This includes referencing specific line numbers from both the original and amended returns.

If the amended return results in a refund, it should be mailed to the Franchise Tax Board at the designated address for refunds. Conversely, if there is an amount due, use the address for payments.

It’s important to include all necessary supporting documentation, such as federal schedules, to substantiate the changes being made on the 100X form.

Corporations must ensure that they check the appropriate boxes on the form to indicate the nature of the amendments being made, such as whether it is a protective claim or based on a final federal determination.