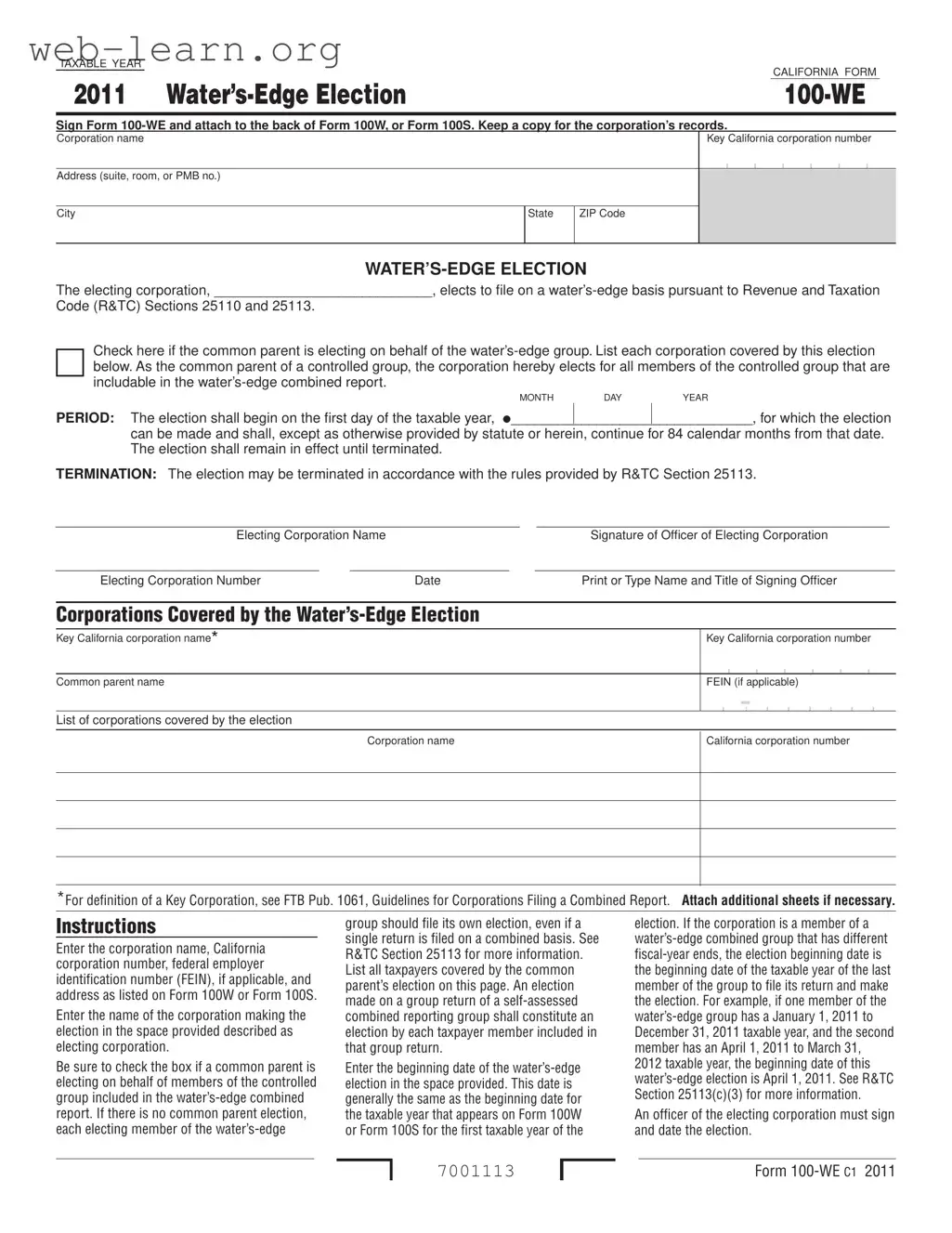

The California 100 We form, officially known as the Water's-Edge Election form, plays a crucial role for corporations operating within California's tax framework. This form allows corporations to elect to file their taxes on a water’s-edge basis, which can significantly affect their tax liabilities. When a corporation opts for this election, it indicates its intention to include only certain income derived from sources within the United States, thereby potentially reducing its overall taxable income. The form requires the corporation to provide essential information such as its name, California corporation number, and address. It also necessitates the identification of any common parent corporation making the election on behalf of a controlled group. The election period typically commences on the first day of the taxable year and lasts for 84 months unless terminated earlier according to specific regulations. Corporations must carefully list all members included in this election, ensuring compliance with the Revenue and Taxation Code sections governing such filings. Proper completion of the form is critical, as it not only affects the corporation’s tax obligations but also requires the signature of an authorized officer, solidifying the corporation's commitment to the election. Understanding the nuances of the California 100 We form is essential for corporations looking to navigate the complexities of state taxation effectively.

| Fact Name | Details |

|---|---|

| Purpose | The California Form 100-WE is used for corporations electing to file on a water’s-edge basis, allowing for a combined report of income from certain foreign and domestic corporations. |

| Governing Laws | This form is governed by the California Revenue and Taxation Code, specifically Sections 25110 and 25113. |

| Filing Requirement | Corporations must attach Form 100-WE to either Form 100W or Form 100S and retain a copy for their records. |

| Election Duration | The water’s-edge election begins on the first day of the taxable year and lasts for 84 calendar months unless terminated earlier. |

| Termination Rules | Corporations can terminate the election according to the rules set forth in R&TC Section 25113. |

| Common Parent Election | If a common parent corporation elects on behalf of a controlled group, it must check the appropriate box on the form to indicate this choice. |

Filling out the California 100 We form requires careful attention to detail. This form is essential for corporations electing to file on a water's-edge basis. Follow these steps to ensure accurate completion.

Once completed, attach the 100 We form to the back of Form 100W or Form 100S. Remember to keep a copy for your records. This will help ensure that all necessary information is readily available for future reference.

What is the California 100 We form?

The California 100 We form, also known as Form 100-WE, is used by corporations to elect to file on a water's-edge basis. This election allows corporations to report their income based on a specific set of rules outlined in California's Revenue and Taxation Code. By making this election, corporations can potentially benefit from certain tax advantages.

Who needs to file the 100 We form?

Any corporation that wishes to elect for a water's-edge combined report must file this form. If a corporation is part of a controlled group, the common parent can file on behalf of all members. Each member of the group that wants to make this election should be listed on the form.

What is the duration of the water's-edge election?

The water's-edge election begins on the first day of the taxable year specified in the form. This election will continue for a total of 84 calendar months, unless terminated earlier according to the rules provided by the Revenue and Taxation Code. It remains in effect until the corporation decides to terminate it.

How do I terminate the water's-edge election?

To terminate the water's-edge election, a corporation must follow the guidelines set forth in R&TC Section 25113. This may involve submitting a notice or specific documentation to the appropriate tax authority. It's important to ensure that all steps are followed correctly to avoid any complications.

What information is required to complete the 100 We form?

When completing the 100 We form, you'll need to provide several key pieces of information:

Make sure to check the box if a common parent is making the election on behalf of the group.

Who should sign the 100 We form?

An officer of the electing corporation must sign and date the form. This signature is crucial, as it verifies that the information provided is accurate and that the corporation is officially making the election. Ensure that the name and title of the signing officer are printed or typed clearly on the form.

Filling out the California 100 We form can be a straightforward process, but there are common mistakes that many people make. Avoiding these pitfalls can save time and ensure compliance. One frequent error is not providing complete information about the corporation. Each section requires specific details, including the corporation name, California corporation number, and address. Missing any of these details can lead to delays or even rejection of the form.

Another mistake is failing to check the box for a common parent when applicable. If a common parent is electing on behalf of the water’s-edge group, it’s crucial to indicate this clearly. Omitting this step can lead to confusion about which entities are included in the election, potentially complicating the filing process.

Many individuals also overlook the importance of accurately entering the beginning date of the water’s-edge election. This date should align with the taxable year stated on Form 100W or Form 100S. If there are multiple members with different fiscal year ends, it’s essential to use the date that corresponds to the last member’s taxable year. Miscalculating this date can result in significant issues down the line.

Additionally, people often forget to list all corporations covered by the election. It’s vital to include every taxpayer that falls under the common parent’s election. Leaving out a corporation can invalidate the election for the entire group, leading to potential tax liabilities.

Signing the form is another crucial step that is sometimes neglected. An officer of the electing corporation must sign and date the election. Without this signature, the form is not valid, and the election cannot take effect. This oversight can easily be avoided by double-checking the form before submission.

Lastly, many filers fail to keep a copy of the completed form for their records. Retaining a copy is essential for future reference, especially if questions arise regarding the election. It’s a simple step that can prevent headaches later on. By being mindful of these common mistakes, you can navigate the California 100 We form process with confidence and ease.

The California Form 100-WE is essential for corporations electing to file on a water’s-edge basis. However, it is often accompanied by several other forms and documents that facilitate compliance with state tax regulations. Below is a list of common forms used in conjunction with the California 100-WE form, each serving a distinct purpose in the tax filing process.

Each of these forms plays a critical role in ensuring compliance with California tax laws. They provide a framework for corporations to accurately report their financial activities and manage their tax obligations effectively. Understanding the purpose of each document can help corporations navigate the complexities of tax filing in California.

The California Form 100 We is a specific document used by corporations to elect to file on a water’s-edge basis. Here are ten other documents that share similarities with the California 100 We form, along with explanations of how they are alike:

When filling out the California 100 We form, it is important to follow specific guidelines to ensure accuracy and compliance. Here are six things you should and shouldn't do:

Many people have misunderstandings about the California Form 100-WE, which is used for the Water’s-Edge Election. Here are some common misconceptions:

Understanding these misconceptions can help corporations navigate the filing process more effectively. It is crucial to be informed and ensure compliance with California tax regulations.

When filling out and using the California 100-WE form, consider the following key takeaways:

By following these guidelines, you can ensure that the form is completed correctly and that your corporation complies with California tax regulations.