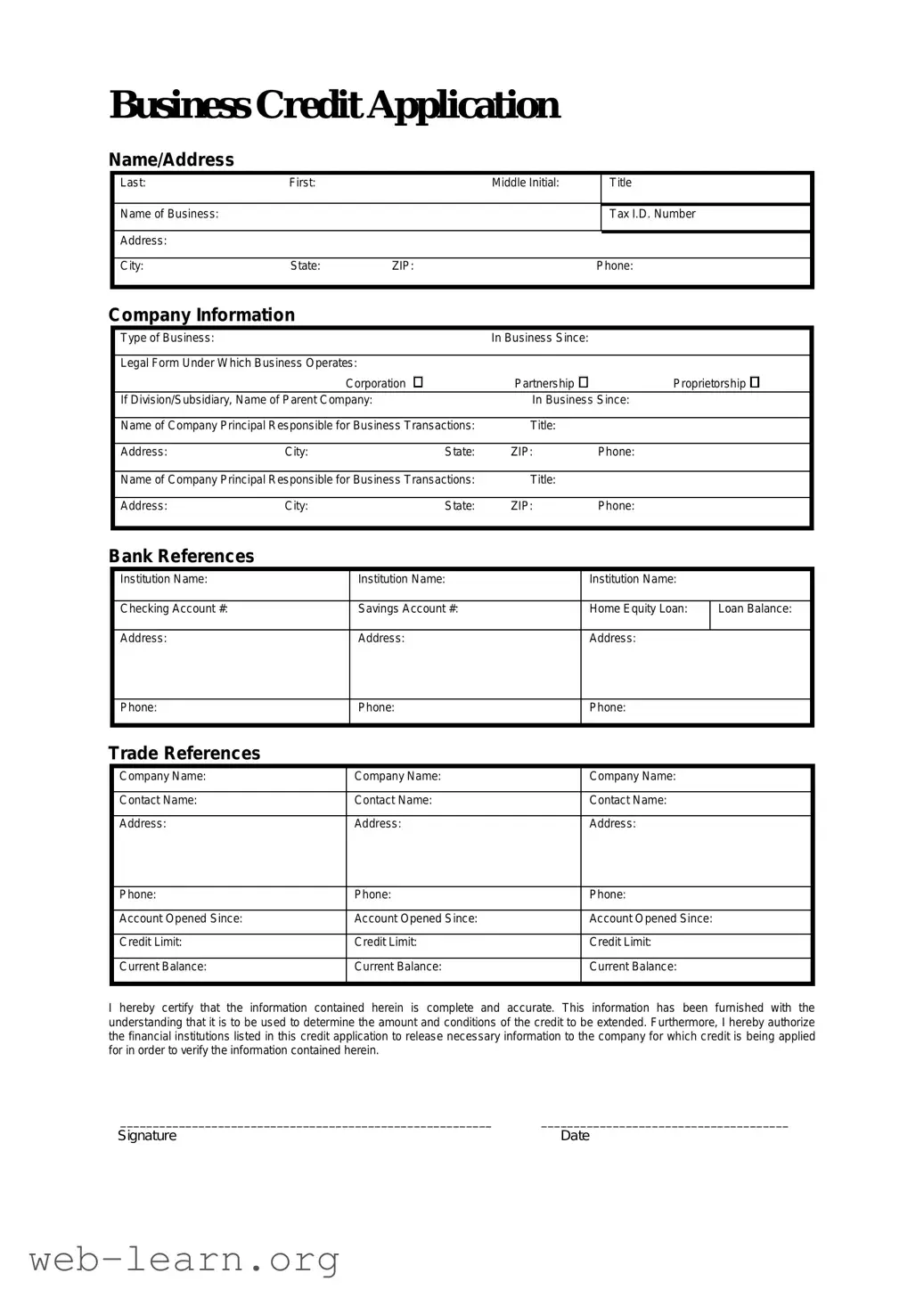

The Business Credit Application form serves as a critical document that facilitates the evaluation of a business's creditworthiness for establishing trade credit. This form typically includes essential information such as the legal name of the business, tax identification number, and business address. Additionally, it often requires details about ownership, including the names of owners or partners, as well as their respective personal guarantees. Financial details reflect the business's stability, encompassing average monthly sales, bank references, and trade references that can attest to the company's credit history. Furthermore, the application may also inquire about the nature of the business, its years of operation, and any existing lines of credit with other suppliers. By collecting this information, the form aids lenders and suppliers in making informed decisions regarding extension of credit, thereby fostering a trusted relationship between the business and its potential creditors.

Business Credit Application

Name/Address

Last: |

First: |

|

Middle Initial: |

|

Title |

|

|

|

|

|

|

Name of Business: |

|

|

|

|

Tax I.D. Number |

|

|

|

|

|

|

Address: |

|

|

|

|

|

|

|

|

|

|

|

City: |

State: |

ZIP: |

|

Phone: |

|

|

|

|

|

|

|

Company Information

|

Type of Business: |

|

|

|

In Business Since: |

|

|

|

|

|

|

|

|

|

|

||

|

Legal Form Under Which Business Operates: |

|

|

|

|

|||

|

|

|

Corporation |

Partnership |

Proprietorship |

|

||

|

If Division/Subsidiary, Name of Parent Company: |

In Business Since: |

|

|||||

|

|

|

|

|

|

|

||

|

Name of Company Principal Responsible for Business Transactions: |

Title: |

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

Address: |

City: |

|

State: |

ZIP: |

Phone: |

|

|

|

|

|

|

|

|

|

||

|

Name of Company Principal Responsible for Business Transactions: |

Title: |

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

Address: |

City: |

|

State: |

ZIP: |

Phone: |

|

|

|

|

|

|

|

|

|

|

|

Bank References |

|

|

|

|

|

|

|

|

|

Institution Name: |

|

|

Institution Name: |

|

Institution Name: |

||

|

|

|

|

|

|

|

|

|

|

Checking Account #: |

|

|

Savings Account #: |

|

Home Equity Loan: |

ILoan Balance: |

|

|

Address: |

|

|

Address: |

|

Address: |

|

|

Phone:

Phone:

Phone:

Trade References

Company Name: |

Company Name: |

Company Name: |

|

|

|

Contact Name: |

Contact Name: |

Contact Name: |

|

|

|

Address: |

Address: |

Address: |

|

|

|

Phone: |

Phone: |

Phone: |

|

|

|

Account Opened Since: |

Account Opened Since: |

Account Opened Since: |

|

|

|

Credit Limit: |

Credit Limit: |

Credit Limit: |

|

|

|

Current Balance: |

Current Balance: |

Current Balance: |

|

|

|

I hereby certify that the information contained herein is complete and accurate. This information has been furnished with the understanding that it is to be used to determine the amount and conditions of the credit to be extended. Furthermore, I hereby authorize the financial institutions listed in this credit application to release necessary information to the company for which credit is being applied for in order to verify the information contained herein.

_________________________________________________________ ______________________________________

Signature |

Date |

| Fact Name | Description |

|---|---|

| Purpose | A Business Credit Application form is used by companies to apply for credit or financing from vendors or financial institutions. |

| Required Information | The form typically requests information such as business name, address, ownership details, financial history, and references. |

| Legal Compliance | Depending on the state, the form may need to comply with specific regulations, such as those outlined in the Uniform Commercial Code (UCC). |

| Approval Process | Submission of the application initiates a review process. The lender or vendor evaluates the application based on the provided information. |

After receiving the Business Credit Application form, you will need to complete it carefully to ensure that all required information is provided. This is an important step in establishing a credit account with a business. Take your time to fill in the form accurately and double-check your information before submitting.

Once you have completed the form, review all entries for accuracy. This step is crucial, as any discrepancies could delay the processing of your application. After ensuring everything is correct, submit the form according to the provided instructions, and await further communication regarding your credit status.

What is the Business Credit Application form?

The Business Credit Application form is a document that companies fill out to apply for credit with a lender or supplier. This form helps creditors assess the financial health and creditworthiness of a business.

Why do I need to fill out the Business Credit Application form?

Completing the Business Credit Application is essential for obtaining credit. It provides lenders with necessary information about your business, including its credit history, financial status, and ability to repay debts. This helps them make informed lending decisions.

What information is usually required on the form?

Typically, you will need to provide:

How long does it take to process the application?

The processing time for a Business Credit Application can vary. Many lenders strive to review and respond to applications within a few days. However, it may take longer depending on the complexity of the application and the lender's internal procedures.

Is there a fee for submitting the application?

Most lenders do not charge a fee for submitting a Business Credit Application. However, it's important to read the terms and conditions provided by the lender to understand any hidden costs or requirements that may apply.

What happens if my application is denied?

If your application is denied, the lender will usually provide a reason for the decision. This feedback can be beneficial as it may highlight areas that need improvement. You may also request a copy of your credit report, which can help you understand the denial better.

Can I appeal a denied application?

Yes, many lenders allow you to appeal a denied Business Credit Application. Prepare a revised application that addresses the concerns raised in the rejection. Providing additional information or documentation may improve your chances of approval.

How often should I update my application?

It is wise to update your Business Credit Application regularly, especially when there are significant changes in your financial situation or business structure. You may also need to resubmit or update the application when applying with a new lender.

Where can I find the Business Credit Application form?

The Business Credit Application form can usually be found on the websites of lenders or financial institutions. Many offer downloadable versions of the form, while others may prompt you to fill it out online. If unsure, contact the lender directly for assistance.

Filling out a Business Credit Application form can be straightforward, but it is common to make mistakes that can delay the process. One frequent error is providing inaccurate information. This can include incorrect addresses, phone numbers, or business names. It’s essential to double-check all entries for accuracy to avoid confusion later.

Another mistake is failing to include all necessary documentation. Applicants should attach relevant financial statements, tax returns, and any other required documents. Missing information might lead to an incomplete application, which can harm a business's chances of getting credit.

Providing insufficient details about the business structure can also pose problems. Whether it's a sole proprietorship, partnership, or corporation, clearly indicating this information helps lenders assess the application accurately. Without clarity, the decision process may take longer.

Many applicants overlook their personal credit history. Lenders often review the personal credit scores of business owners, especially for small businesses. Neglecting to disclose this information may result in missed opportunities for credit approval.

Some individuals fail to check their application for spelling errors and typos. Simple mistakes can create a negative impression on lenders. Taking the time to proofread is a crucial step in presenting a professional application.

Another common mistake involves not listing all authorized signers. It is important to include all individuals authorized to make financial decisions on behalf of the business. Omitting this information can cause frustration and delays.

Providing vague answers to questions can also lead to misunderstandings. Lenders appreciate clear and specific responses. This aids in making informed decisions, so taking the time to be precise is beneficial.

Some applicants underestimate the importance of explaining the purpose of the credit request. A clear statement about how the funds will be used helps lenders understand the business's needs. This could impact the likelihood of credit approval.

Improperly estimating the desired credit amount is another frequent oversight. Applicants should have a clear idea of how much credit they need and why. This should be backed by realistic projections to strengthen the request.

Finally, neglecting to sign and date the application can render it invalid. It's essential to check that all necessary signatures are included before submission. A missing signature can cause delays in processing the application.

When applying for credit as a business, it's essential to accompany your Business Credit Application form with several other documents. These documents not only strengthen your application but also provide lenders with a comprehensive picture of your business's financial health. Here are five key forms and documents often used in conjunction with the application.

By preparing these additional forms and documents, you can enhance your Business Credit Application and potentially improve your chances of obtaining credit. Each document plays a pivotal role in providing the lender with a clearer understanding of your business’s financial situation and future potential.

Loan Application Form: Like the Business Credit Application, a loan application gathers detailed financial and personal information to assess creditworthiness.

Credit Line Request Form: This document requests the establishment of a credit line. Both forms evaluate financial stability and repayment capability.

Supplier Credit Application: Similar to a Business Credit Application, this form is used by suppliers to evaluate a business’s credit history before extending credit terms.

Partnership Agreement: While different in purpose, a partnership agreement includes financial disclosures and commitments, similar to the business credit application.

Vendor Application Form: This document collects information that helps vendors determine the risk of extending credit, akin to the information gathered in a business credit application.

Commercial Lease Application: Both forms request financial information and previous payment history to assess the applicant's reliability.

Business License Application: While primarily focused on obtaining a license, this application may also request financial data to ensure the business is in good standing.

Insurance Application: Similar in that it assesses risk, this form gathers financial data and business history to determine eligibility for coverage.

When filling out a Business Credit Application form, it’s important to be thorough and accurate. Here are some important dos and don’ts to keep in mind:

The Business Credit Application form is a crucial document for companies seeking to establish credit with suppliers and creditors. However, several misconceptions surround this form that can lead to confusion. Here are eight common misconceptions explained.

This is not true. Both small and large businesses can benefit from a Business Credit Application. It's essential for any business looking to build or maintain credit.

While completing the form is necessary to apply, it does not automatically guarantee approval. Creditors evaluate various factors, including credit history and financial stability.

It's a common belief that only business credit matters. However, creditors may consider the owner's personal credit history, especially for smaller businesses.

Inaccuracies can lead to complications or outright rejection of the application. Always ensure the information is correct and up to date.

Some think once the application is submitted, there’s no further action required. In reality, businesses should regularly update their information to reflect changes.

While financial details are important, the form also requests information regarding business structure, ownership, and operational history.

Many assume that the form is complex and hard to understand. In fact, most forms are straightforward and designed for easy completion. Assistance is available if difficulties arise.

Some believe that the application does not need a review. Taking the time to double-check can prevent errors that may delay the approval process.

Understanding these misconceptions can help you navigate the Business Credit Application process confidently. By ensuring you have accurate information and a clear understanding of the expectations, you can improve your chances of obtaining the credit your business needs.

Filling out and using a Business Credit Application form is crucial for establishing credit relationships with suppliers and lenders. Here are key takeaways to keep in mind:

By adhering to these guidelines, businesses can improve their chances of receiving favorable credit terms and establishing solid financial partnerships.

What Is P45 in Uk - It consists of three parts: Part 1 for HM Revenue & Customs, Part 1A for the employee, and Parts 2 and 3 for the new employer.

Medicaid Prior Authorization Form - Pdf - Prescribers should attach medical justification if needed for the request.