The Arkansas ET-1 form plays a critical role in the state's tax reporting framework, specifically for sales and excise taxes. This form is designed for reporting all state and local taxes levied under the Gross Receipts (Sales) Tax and Compensating Use Tax Acts. Taxpayers must round all figures to the nearest whole dollar, ensuring accuracy in their submissions. The form includes sections for various types of taxes, such as Gross Receipts Tax, Food Tax, Manufacturing Utility Tax, and Aviation Tax, among others. Each section guides users through reporting their taxable sales, calculating the gross tax due, and applying any eligible discounts or credits. The ET-1 form also allows for the reporting of local sales and use taxes, ensuring that all obligations are met for both state and local jurisdictions. Additionally, taxpayers can file amended returns if necessary, making it a versatile tool for compliance. With the introduction of the Arkansas Taxpayer Access Point (ATAP), managing tax accounts has become more streamlined, offering online access to tax-related information and services. Understanding the ET-1 form is essential for Arkansas businesses to navigate their tax responsibilities effectively.

| Fact Name | Fact Description | Governing Law |

|---|---|---|

| Purpose of ET-1 | The ET-1 form is used to report all state and local taxes under the Gross Receipts (Sales) Tax and Compensating Use Tax Acts. | Arkansas Code Annotated § 26-52-101 et seq. |

| Filing Method | Taxpayers can file their ET-1 form online through the Arkansas Taxpayer Access Point (ATAP) for convenience. | Arkansas Code Annotated § 26-18-101 et seq. |

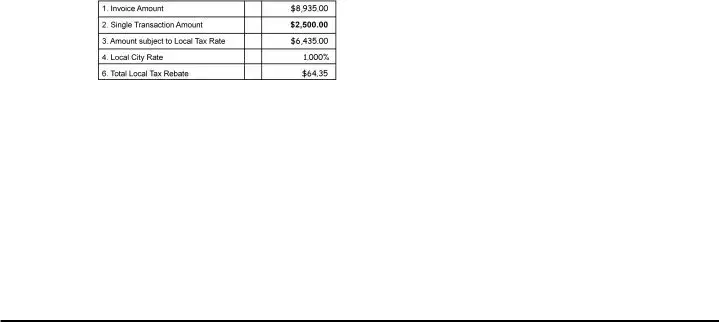

| Discount Eligibility | A 2% discount is available for timely filed reports if full payment is made, capped at $1,000. | Arkansas Code Annotated § 26-52-507. |

| Amended Returns | Taxpayers can file an amended return by checking the "Amended Return" box and providing an explanation for changes. | Arkansas Code Annotated § 26-18-303. |

Filling out the Arkansas ET-1 form can seem daunting at first, but by following a series of straightforward steps, you can complete it accurately. This form is essential for reporting various state and local taxes, and ensuring that all required information is submitted correctly will help you avoid any potential issues.

After completing these steps, review the form for accuracy. It’s essential to ensure all calculations are correct and that all required information is included. Once verified, you can submit the form to the Arkansas Department of Finance and Administration, either by mail or electronically through the Arkansas Taxpayer Access Point (ATAP).

What is the Arkansas ET-1 form?

The Arkansas ET-1 form is an excise tax return used to report state and local taxes under the Gross Receipts (Sales) Tax and Compensating Use Tax Acts. This form is essential for businesses operating in Arkansas to ensure compliance with tax obligations. It encompasses various tax types, including sales tax, food tax, and manufacturing utility tax, among others.

Who needs to file the ET-1 form?

Any business or individual who sells taxable goods or services in Arkansas is required to file the ET-1 form. This includes in-state sellers and out-of-state sellers making sales into Arkansas. If you have taxable sales or purchases during the reporting period, you must complete and submit this form.

How do I complete the ET-1 form?

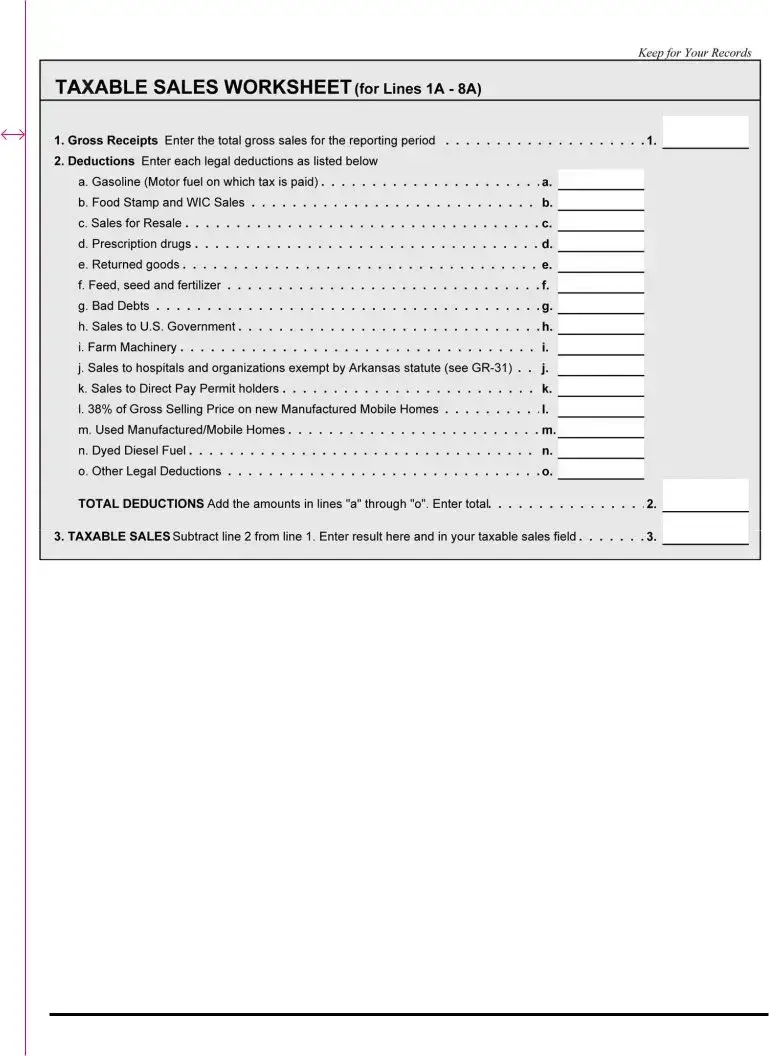

To complete the ET-1 form, start by gathering your taxable sales data from the Taxable Sales Worksheet. Ensure that all figures are rounded to the nearest whole dollar. Use blue or black ink for clarity. The form consists of various sections where you will report different types of taxes, such as gross receipts tax and food tax. Follow the instructions carefully for each line, and remember to calculate any applicable discounts or credits.

What discounts are available when filing the ET-1 form?

If you file your report by the 20th of the month due and make full payment, you may qualify for a 2% discount on certain state taxes. However, this discount cannot exceed $1,000. Be sure to calculate this discount accurately and include it on the appropriate lines of the form.

Can I amend my ET-1 form if I made a mistake?

Yes, you can amend your ET-1 form if necessary. To do this, check the "Amended Return" box at the top of the form and complete it as you would for an original submission. Attach a letter explaining the changes and the reasons behind them. It's important to include this explanation to avoid delays in processing your amended return.

What is the Arkansas Taxpayer Access Point (ATAP)?

The Arkansas Taxpayer Access Point (ATAP) is an online service that provides taxpayers with secure access to their tax accounts. Through ATAP, you can file and amend returns, make payments, and view your tax account information anytime, day or night. If you haven’t signed up yet, visit atap.arkansas.gov to create your account and explore the available services.

Where can I find more information about the taxes reported on the ET-1 form?

For detailed information about the various taxes reported on the ET-1 form, you can visit the Arkansas Department of Finance and Administration's website at www.arkansas.gov/salestax. Additionally, you can contact their office directly at (501) 682-7104 for any specific questions or assistance you may need.

Filling out the Arkansas ET-1 form can be a straightforward process, but many individuals make common mistakes that can lead to delays or inaccuracies in their tax submissions. One significant error occurs when taxpayers fail to round figures correctly. The instructions clearly state that all figures must be rounded to the nearest whole dollar. For instance, amounts with cents below 50 should be dropped, while amounts of 50 cents or more should be rounded up. Neglecting this rule can result in discrepancies in the total tax due.

Another frequent mistake is using the wrong ink color. The form specifically instructs users to complete it in blue or black ink only. Using pencil or any other color can render the form invalid, leading to potential processing issues. It is essential to adhere to this guideline to ensure that the form is accepted without complications.

Additionally, many individuals overlook the importance of checking for pre-printed information on the form. Failing to verify the accuracy of pre-printed names, addresses, or account numbers can lead to misfiled returns. Taxpayers should always double-check these details before submission to avoid any potential issues with their tax accounts.

Another common error involves the calculation of discounts. Taxpayers often miscalculate the 2% discount allowed for timely submissions. This discount applies only if the report is postmarked by the 20th of the month due, and the full payment is made with the report. If the discount exceeds the maximum allowable amount, it can lead to incorrect tax calculations.

Lastly, many taxpayers forget to sign the form. The signature of a responsible party is required for the return to be valid. Without a signature, the form cannot be processed, which can result in penalties or additional fees. It is vital to ensure that the form is signed before submission to avoid any unnecessary complications.

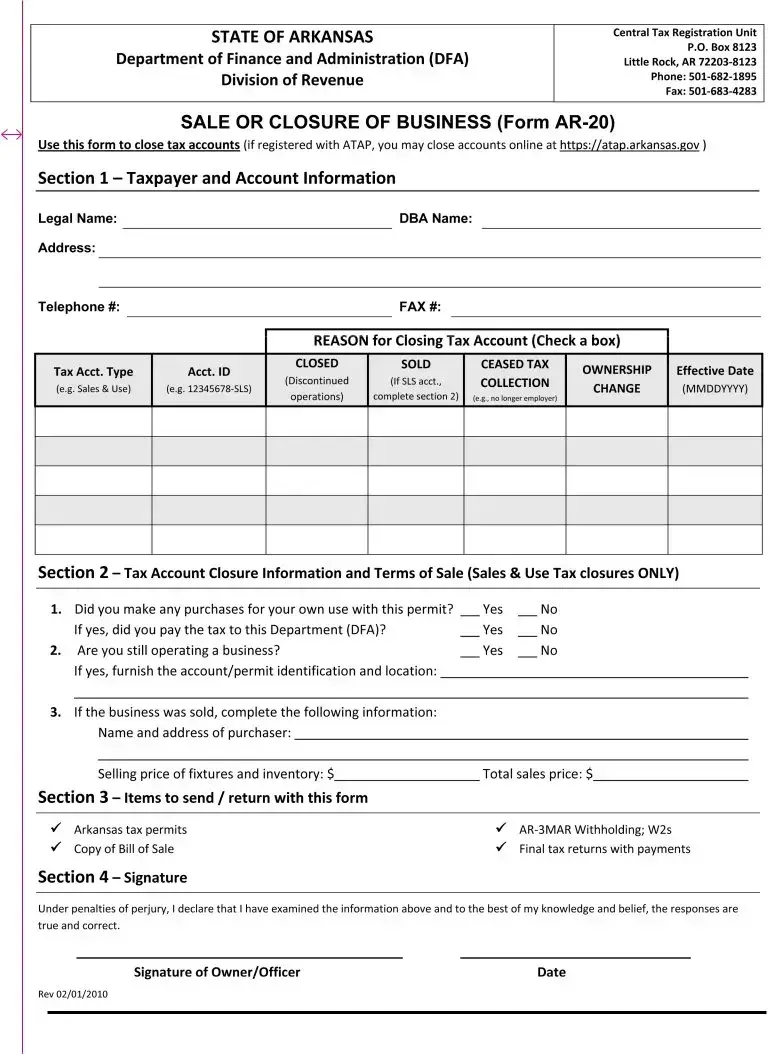

The Arkansas ET-1 form is a crucial document for reporting state and local taxes related to sales and use. Alongside this form, several other documents and forms are commonly utilized to ensure compliance with Arkansas tax regulations. Below is a list of these documents, each with a brief description.

Understanding these forms and documents is essential for taxpayers in Arkansas to maintain compliance and effectively manage their tax obligations. Utilizing these resources can streamline the reporting process and minimize errors.

When filling out the Arkansas ET-1 form, it’s important to follow certain guidelines to ensure accuracy and compliance. Here’s a list of things to do and avoid:

Misconceptions about the Arkansas ET-1 form can lead to confusion and mistakes in tax reporting. Here are nine common misunderstandings, along with clarifications to help you navigate this important document.

Understanding these misconceptions can help ensure accurate tax reporting and compliance with Arkansas tax laws. Always consult the official guidelines or a tax professional if you have questions.

Understanding the Arkansas ET-1 Form is crucial for accurate tax reporting. Here are some key takeaways to help you navigate the process: