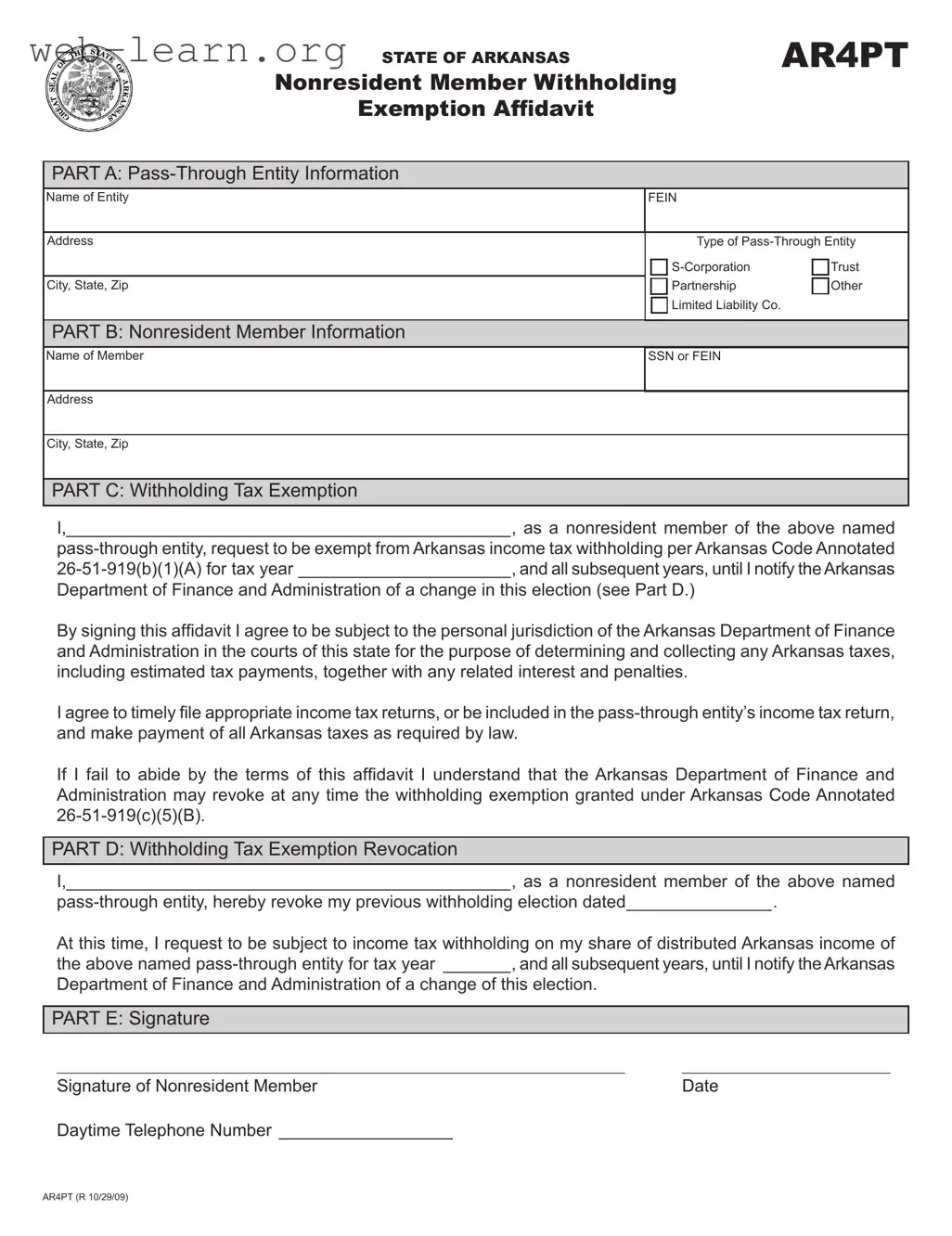

Navigating the complexities of tax obligations can be a daunting task, especially for nonresident members of pass-through entities in Arkansas. The Arkansas AR4PT form serves as a crucial tool for these individuals, allowing them to request an exemption from state income tax withholding on their share of distributed Arkansas income. This form is divided into several parts, each tailored to gather specific information. In the first section, pass-through entities, such as S-Corporations, partnerships, and limited liability companies, provide essential details about their organization. The subsequent section captures vital information about the nonresident member, including their name and identification number. Perhaps the most significant aspect of the AR4PT form is the withholding tax exemption request, where nonresident members can assert their eligibility for exemption under Arkansas law. Additionally, the form includes provisions for revoking a previous exemption, ensuring that members can adjust their tax status as needed. By understanding the ins and outs of the AR4PT form, nonresident members can better manage their tax responsibilities and ensure compliance with Arkansas tax regulations.

| Fact Name | Details |

|---|---|

| Purpose of the Form | The Arkansas AR4PT form allows nonresident members of pass-through entities to request an exemption from Arkansas income tax withholding. |

| Governing Law | This form is governed by Arkansas Code Annotated 26-51-919(b)(1)(A), which outlines the withholding requirements for nonresident members. |

| Eligibility for Exemption | Nonresident members who receive distributions from a pass-through entity can claim an exemption by submitting the completed AR4PT form. |

| Revocation of Exemption | A nonresident member can revoke their withholding exemption by completing Part D of the AR4PT form and notifying the pass-through entity. |

| Retention of Records | Pass-through entities are required to retain the original AR4PT forms and provide copies to the Arkansas Department of Finance and Administration upon request. |

| Annual Reporting Requirement | Pass-through entities must report the names, addresses, and identification numbers of nonresident members who have submitted the AR4PT form on an annual basis. |

| Submission Method | The AR4PT form must be submitted to the pass-through entity, which will then manage the filing with the Arkansas Department of Finance and Administration. |

Completing the Arkansas AR4PT form is essential for nonresident members of pass-through entities who wish to claim an exemption from state income tax withholding. This form must be filled out carefully and submitted to the appropriate pass-through entity to ensure compliance with Arkansas tax regulations.

The Arkansas AR4PT form is a Nonresident Member Withholding Exemption Affidavit. It allows nonresident members of pass-through entities, such as partnerships and S-corporations, to request an exemption from Arkansas income tax withholding on their share of distributed Arkansas income. This form must be completed and submitted to the pass-through entity to claim the exemption.

Any nonresident member receiving a distribution of Arkansas income from a pass-through entity can fill out the AR4PT form. This includes individuals who are part of partnerships, S-corporations, limited liability companies, and trusts that have Arkansas income.

The form consists of several parts that require specific information:

A nonresident member can claim the exemption by completing Parts A, B, C, and E of the AR4PT form. After filling out the form, it must be submitted to the pass-through entity. If the member has previously claimed an exemption and wishes to revoke it, they must complete Parts A, B, D, and E instead.

If any information in Parts A or B changes, the nonresident member must file a new AR4PT form with the pass-through entity. This ensures that the entity has the most current information for tax purposes.

If a nonresident member fails to comply with the terms of the AR4PT form, the Arkansas Department of Finance and Administration may revoke the withholding exemption. This could result in the member being subject to Arkansas income tax withholding on their share of distributed income.

The pass-through entity must retain the original AR4PT forms and provide copies to the Arkansas Department of Finance and Administration upon request. Additionally, they must report the names, addresses, and identification numbers of all nonresident members who have submitted the form on an annual basis.

Pass-through entities must file the nonresident member affidavit information on a CD or diskette using a specified format. This includes a spreadsheet or database format. The filing must be done by the due date of the entity’s income tax return, including extensions. If a hardship exists, a request for a waiver can be submitted to the Department.

Filling out the Arkansas AR4PT form can be a straightforward process, but several common mistakes can lead to complications. One significant error occurs when individuals fail to provide complete information in Parts A and B. Each section requires specific details about both the pass-through entity and the nonresident member. Omitting any of this information can result in delays or rejections of the form.

Another frequent mistake involves incorrect identification numbers. Nonresident members must include their Social Security Number (SSN) or Federal Employer Identification Number (FEIN) accurately. A simple typo in these numbers can lead to issues with tax filings and compliance, causing unnecessary stress and potential penalties.

People often overlook the requirement to sign the affidavit. Part E clearly states that the nonresident member must provide a signature and date. Without this, the form is incomplete and cannot be processed. It's essential to double-check that all necessary signatures are present before submission.

Additionally, some individuals misinterpret the exemption request. The affidavit must explicitly state the desire for an exemption from Arkansas income tax withholding. Failing to clearly indicate this can result in automatic withholding, negating the purpose of submitting the form.

Another common error is neglecting to update the affidavit when information changes. If there are any changes to the details provided in Parts A or B, a new affidavit must be submitted. Many people forget this requirement, leading to complications in tax reporting and compliance.

Finally, misunderstanding the revocation process can create issues. If a nonresident member wishes to revoke a previous exemption, they must complete Parts A, B, D, and E. Confusion about this process can lead to continued withholding when it is not desired, causing frustration and potential financial impact.

The Arkansas AR4PT form is essential for nonresident members of pass-through entities seeking exemption from Arkansas income tax withholding. When filing this form, several other documents may also be necessary to ensure compliance with state tax regulations. Below is a list of commonly used forms and documents that often accompany the AR4PT.

Understanding these additional forms and documents can help nonresident members navigate their tax obligations more effectively. Properly completing and submitting the AR4PT and its accompanying forms ensures compliance and helps avoid potential issues with the Arkansas Department of Finance and Administration.

The Arkansas AR4PT form serves a specific purpose in the context of tax withholding for nonresident members of pass-through entities. Several other documents share similarities with the AR4PT form, primarily in their function of managing tax obligations and exemptions. Below is a list detailing these documents and how they relate to the AR4PT form.

Each of these documents plays a crucial role in the management of tax obligations for nonresident individuals or entities, highlighting the importance of proper documentation in ensuring compliance with tax laws.

When filling out the Arkansas AR4PT form, it’s essential to approach the task with care. Here are four important do's and don'ts to keep in mind:

Misconceptions about the Arkansas AR4PT form can lead to confusion for nonresident members and pass-through entities. Here are eight common misconceptions explained:

Filling out the Arkansas AR4PT form can seem daunting, but understanding its key elements can make the process smoother. Here are some important takeaways to keep in mind:

By following these guidelines, you can navigate the AR4PT form with confidence and ensure compliance with Arkansas tax regulations.