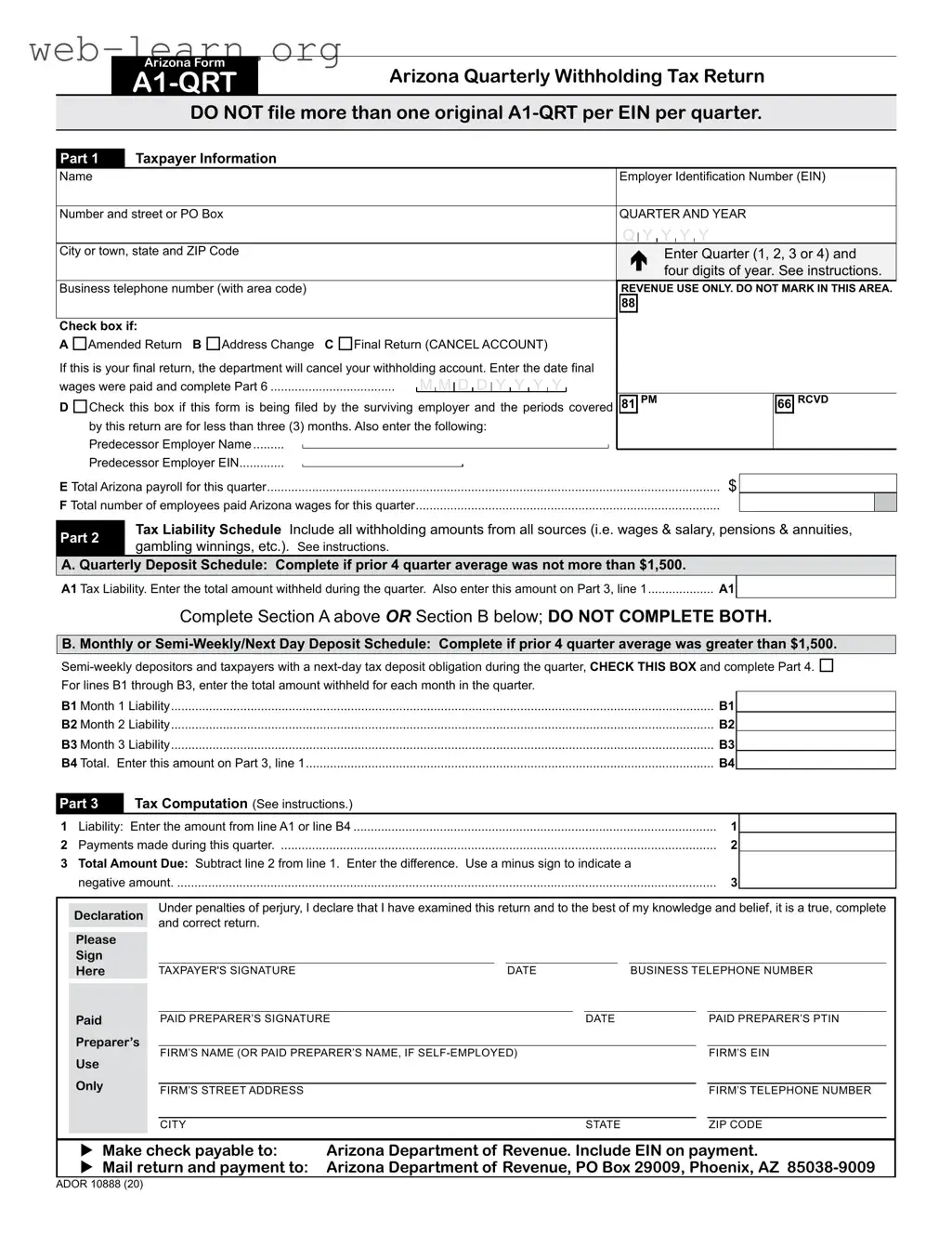

The Arizona Tax Return Form A1-QRT is essential for employers who need to report and remit withholding tax for employees working in the state. This form is specifically designed for quarterly reporting and must be submitted for each quarter of the calendar year, regardless of whether any tax was withheld during that period. Key sections of the form include taxpayer information, tax liability schedules, and tax computation. Employers must provide details such as their Employer Identification Number (EIN), business address, and total Arizona payroll for the quarter. The form also allows for adjustments, such as marking it as an amended return or indicating if it is a final return due to changes in business status. Importantly, the A1-QRT consolidates various withholding amounts from wages, pensions, and other income sources, ensuring that employers accurately reconcile their tax obligations. With specific instructions for deposit schedules based on the employer's withholding history, the A1-QRT helps maintain compliance with Arizona tax laws while facilitating the timely payment of withheld taxes.

| Fact Name | Details |

|---|---|

| Form Purpose | The Arizona Form A1-QRT is used by employers to report and reconcile Arizona income tax withheld from employees' wages during a calendar quarter. |

| Filing Frequency | Employers must file the A1-QRT form every quarter, even if no taxes were withheld during that period. This ensures compliance with state regulations. |

| Deposit Schedule | The deposit schedule for withholding taxes depends on the average amount withheld in the previous four quarters. Employers with lower amounts may file quarterly, while others may need to file monthly or semi-weekly. |

| Final Return Notification | If an employer is ceasing operations or canceling their withholding account, they must indicate this by checking the appropriate box on the form. This helps the state update their records accurately. |

| Governing Laws | The filing and requirements for the A1-QRT are governed by Arizona Revised Statutes (A.R.S.) § 43-401 and related tax procedures, ensuring adherence to state tax laws. |

Completing the Arizona Tax Return Form A1-QRT involves several steps to ensure accurate reporting of withholding tax for your business. Follow the instructions carefully to avoid any errors that may lead to complications with your tax filings.

After completing the form, ensure all information is accurate and submit it by the due date to avoid penalties. Keep a copy for your records. If you have any questions or need assistance, consult the Arizona Department of Revenue website or contact their office directly.

Form A1-QRT is the Arizona Quarterly Withholding Tax Return. Employers must use this form to report and remit Arizona income tax withheld from wages paid to employees for services performed in Arizona. It’s essential because it reconciles the amounts withheld during the quarter and ensures compliance with Arizona tax laws. Employers must file this form even if no tax was withheld during the quarter. In such cases, a zero withholding liability must be reported.

All employers, except those who remit on an annual basis, must file Form A1-QRT. This includes employers who remit on quarterly, monthly, semi-weekly, or next-day schedules. Even if an employer did not withhold any Arizona income tax during a quarter, they are still required to file this form. It’s crucial to maintain compliance and avoid penalties.

Form A1-QRT is due on specific dates based on the quarter:

If any due date falls on a Saturday, Sunday, or legal holiday, the return will be considered timely if filed by the next business day. Employers who made all payments on time during the prior quarter may be eligible for a 10-day extension.

Form A1-QRT reconciles all Arizona withholding amounts averaging more than $200 per quarter. This includes taxes withheld from wages, pensions, and gambling winnings. Employers must treat all withheld amounts as if they were from wages paid to employees. If federal forms like Form 941 or Form 945 are filed, one A1-QRT should be submitted to reconcile the total Arizona withholding for the quarter.

Filling out the Arizona Tax Return form can be a straightforward process, but many individuals make common mistakes that can lead to complications. One frequent error is neglecting to check the appropriate box for amended returns or final returns. This oversight can result in confusion for the Arizona Department of Revenue and may delay processing.

Another common mistake is failing to enter the correct Employer Identification Number (EIN). The EIN is crucial for identifying the business, and any discrepancies can cause significant issues in tax processing. Additionally, not providing complete taxpayer information, such as the business address or telephone number, can lead to unnecessary delays or rejection of the return.

Many people also overlook the importance of accurately calculating their total Arizona payroll for the quarter. Inaccurate payroll figures can lead to incorrect tax liabilities, which may result in penalties or interest. Furthermore, some individuals mistakenly complete both the Quarterly Deposit Schedule and the Monthly or Semi-Weekly Deposit Schedule. It is vital to choose only one of these sections based on the business's prior withholding activity.

Missing the due date for filing the return is another frequent error. Employers should be aware of the specific deadlines for each quarter. If a return is submitted late, it may incur penalties and interest. Additionally, some filers fail to keep copies of their submitted forms and supporting documents. Retaining these records is essential for future reference and potential audits.

Finally, individuals often forget to sign and date the return. A missing signature can render the form invalid, leading to complications in processing. It is also important to ensure that any payments are made correctly and on time, as delays can result in additional fees. Avoiding these common mistakes can streamline the tax filing process and ensure compliance with Arizona tax laws.

When filing your Arizona Tax Return, there are several other forms and documents that you may need to complete. These documents help ensure that all tax obligations are met and provide necessary information to the Arizona Department of Revenue. Below is a list of five common forms and documents often used alongside the Arizona Tax Return form.

Understanding these forms and documents can help streamline the filing process and ensure compliance with Arizona tax laws. Always check for the most current requirements and consult with a tax professional if needed.

When filling out the Arizona Tax Return form (A1-QRT), it is essential to follow specific guidelines to ensure accuracy and compliance. Here are nine key things to remember:

By adhering to these guidelines, you can navigate the Arizona Tax Return process more smoothly and avoid potential pitfalls.

Understanding the Arizona Tax Return form can be challenging. Several misconceptions exist that may lead to confusion. Here are four common misconceptions explained:

By clarifying these misconceptions, employers can ensure compliance and avoid potential pitfalls associated with the Arizona Tax Return form.

Key Takeaways for Filling Out and Using the Arizona Tax Return Form A1-QRT