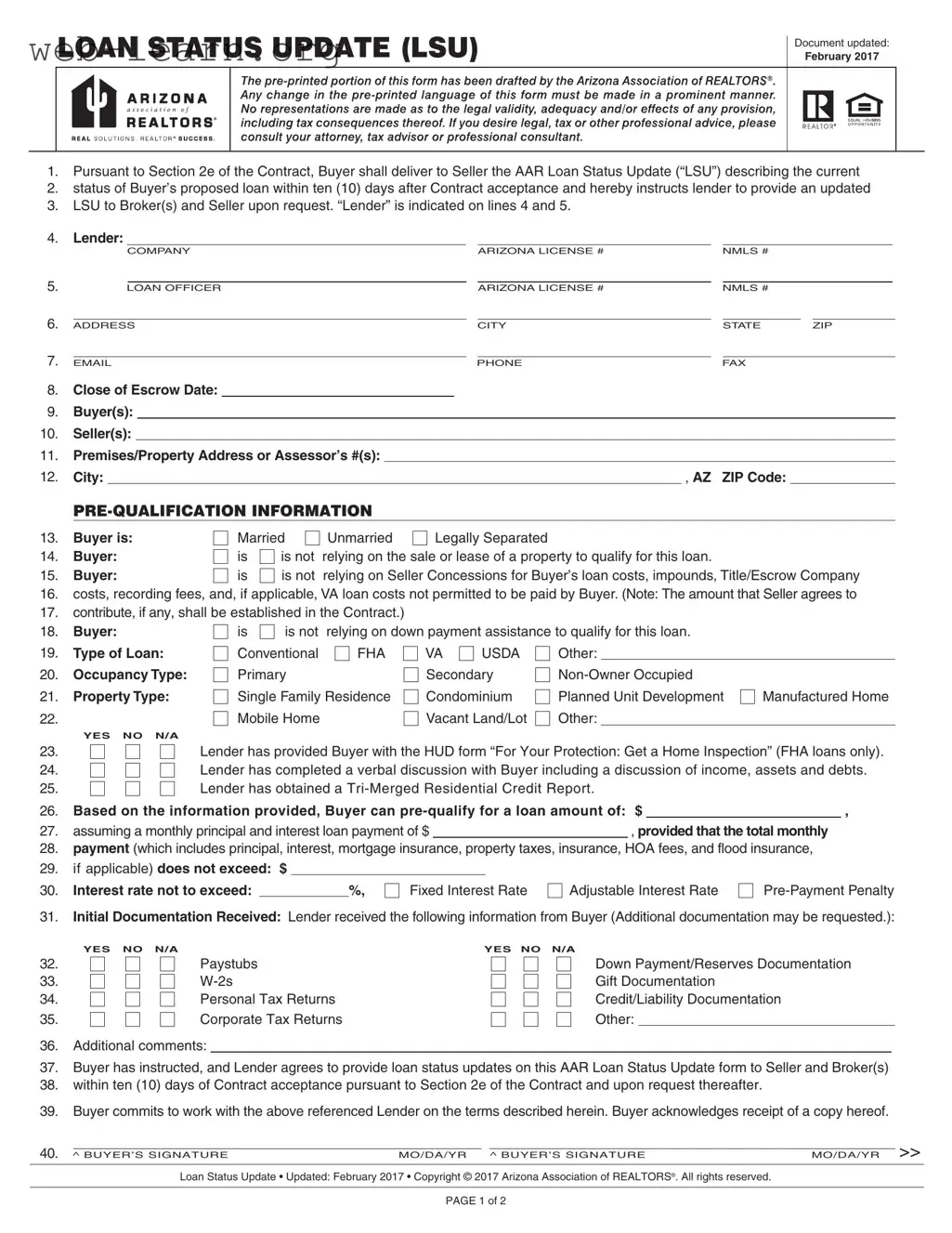

The Arizona Loan Status Update (LSU) form is a crucial document in the home-buying process, providing essential information about a buyer's loan status to both the seller and the broker. This form must be delivered within five days of contract acceptance, ensuring timely communication regarding the buyer's financing. Key sections of the LSU include details about the lender, the type of loan, and the buyer's financial qualifications. It outlines whether the buyer is relying on seller concessions and includes pre-qualification information that helps assess the buyer's ability to secure financing. Additionally, the form tracks the progress of the loan application, from initial documentation to closing, ensuring all parties are informed of any updates. The lender is responsible for providing updates upon request, fostering transparency throughout the transaction. Overall, the LSU is designed to streamline communication and facilitate a smoother closing process for all involved.

| Fact Name | Details |

|---|---|

| Document Purpose | The Loan Status Update (LSU) is used to inform the seller about the current status of the buyer's proposed loan. |

| Submission Timeline | Buyers must deliver the LSU to the seller within five days after the acceptance of the contract. |

| Governing Law | This form is governed by Arizona law, specifically under the guidelines set forth by the Arizona Association of REALTORS®. |

| Lender Information | The form requires the lender's name, license number, and contact details, ensuring transparency in the loan process. |

| Loan Types | Buyers can indicate various loan types including Conventional, FHA, VA, and USDA, allowing for flexibility in financing options. |

| Occupancy Type | The form allows buyers to specify the occupancy type of the property, such as primary residence or investment property. |

| Documentation Requirements | Buyers must provide initial documentation to the lender, including paystubs and tax returns, to facilitate the loan approval process. |

Filling out the Arizona Loan Status Update (LSU) form is an essential step in the loan process. This form ensures that all parties involved are informed about the current status of the loan. Timely completion is crucial, as it must be submitted within five days after the acceptance of the contract.

What is the Arizona LSU form?

The Arizona Loan Status Update (LSU) form is a document used to provide updates on the status of a buyer's proposed loan during a real estate transaction. It ensures that both the seller and broker are informed about the loan process and any changes that may occur.

When must the LSU be submitted?

The buyer is required to submit the LSU to the seller within five (5) days after the acceptance of the contract. This timeline helps maintain transparency and keeps all parties informed of the loan status.

Who is responsible for completing the LSU?

The buyer is responsible for providing the necessary information in the LSU. Additionally, the lender must complete certain sections of the form, particularly regarding loan approval and documentation.

What information is included in the LSU?

The LSU includes details such as:

What happens if the buyer relies on the sale of another property to qualify for the loan?

If the buyer is relying on the sale or lease of another property, they must indicate this on the LSU. This information is crucial for the lender to assess the buyer's financial situation and loan eligibility.

What types of loans can be indicated on the LSU?

The LSU allows for various loan types, including:

What is the significance of the buyer's signature on the LSU?

The buyer's signature on the LSU indicates their acknowledgment of the information provided and their intention to proceed with the lender as described in the form. It serves as a formal agreement between the buyer and the lender.

How does the LSU facilitate communication between parties?

The LSU facilitates communication by requiring the lender to provide updates to the seller and brokers within five days of contract acceptance and upon request thereafter. This ensures that all parties are kept informed throughout the loan process.

What are the consequences of not submitting the LSU on time?

Failure to submit the LSU within the specified timeframe could lead to delays in the transaction process. It may also affect the buyer's credibility and relationship with the seller and lender.

Can the LSU be amended after submission?

Yes, the LSU can be amended if there are changes in the loan status or other relevant information. It is important to keep all parties updated to avoid misunderstandings or complications in the transaction.

Filling out the Arizona Loan Status Update (LSU) form can be straightforward, but many people make common mistakes that can lead to delays or complications in the loan process. One frequent error is failing to provide accurate lender information. Lines 4 and 5 require specific details about the lender, including the company name and license number. If this information is incorrect or missing, it can hinder communication and processing.

Another mistake is neglecting to sign the document. The form requires the buyer's signature at the end. Without it, the lender cannot proceed with the loan application. Buyers should ensure they sign and date the form appropriately, as this confirms their intent to move forward with the loan.

Some individuals overlook the importance of selecting the correct type of loan and occupancy type. Section 18 and 19 of the form require clear choices regarding these options. Choosing incorrectly can lead to confusion and may affect the loan terms. Buyers should carefully consider their situation and select the options that accurately reflect their needs.

In addition, failing to provide complete pre-qualification information can be detrimental. Section 13 through 21 asks for crucial details about the buyer's marital status, reliance on property sales, and loan costs. Incomplete responses can raise red flags for lenders and delay the approval process.

Many also forget to include the necessary documentation. Lines 30 to 35 list various documents that the lender may require. If these documents are not provided, it can lead to further requests and slow down the process. Buyers should ensure they have all necessary paperwork ready before submitting the form.

Another common error is not keeping track of deadlines. The form specifies that the LSU must be delivered within five days after contract acceptance. Missing this deadline can create complications and potentially jeopardize the loan agreement. Timeliness is crucial in real estate transactions.

Buyers sometimes fail to communicate effectively with their lenders. Section 23 emphasizes the importance of a verbal discussion about income, assets, and debts. If this conversation does not happen, the lender may not fully understand the buyer's financial situation, leading to potential issues later on.

Lastly, not reviewing the completed form before submission can lead to avoidable mistakes. Buyers should take the time to double-check all entries for accuracy and completeness. A thorough review can prevent many of the common pitfalls associated with filling out the Arizona LSU form.

The Arizona Loan Status Update (LSU) form is a crucial document in the home buying process, providing essential information about the buyer's loan status. Alongside the LSU, several other forms and documents are commonly used to ensure a smooth transaction. Below is a brief overview of four key documents that often accompany the LSU.

Understanding these documents can significantly enhance the home buying experience. Each plays a vital role in ensuring that all parties are informed and protected throughout the transaction process. Familiarity with these forms will help buyers navigate their mortgage journey with confidence.

The Arizona Loan Status Update (LSU) form is an essential document in real estate transactions, particularly when it comes to tracking the status of a buyer's loan. Several other documents share similar purposes or functions in the context of real estate and loan processing. Below is a list of ten such documents, highlighting their similarities with the Arizona LSU form.

Understanding these documents can empower buyers and sellers to navigate the complexities of real estate transactions more effectively. Each serves a unique purpose, yet they all contribute to a clearer picture of the loan process and property acquisition.

When filling out the Arizona Loan Status Update (LSU) form, it's important to follow certain guidelines. Here’s a list of things you should and shouldn't do:

By following these guidelines, you can help ensure that the LSU form is completed correctly and efficiently.

1. The LSU is only for FHA loans. This is incorrect. The Loan Status Update (LSU) applies to various loan types, including Conventional, VA, USDA, and others, not just FHA loans.

2. Buyers can submit the LSU at any time. This misconception overlooks the requirement. Buyers must deliver the LSU within five days after contract acceptance, as specified in the contract.

3. The lender automatically provides updates without a request. While lenders are instructed to provide updates, they do so upon request from the buyer, broker, or seller.

4. The LSU is a binding contract. The LSU is not a contract but a status update document. It provides information about the loan process without creating binding obligations.

5. Buyers do not need to provide any documentation. Buyers are required to submit initial documentation, including paystubs and tax returns, as part of the loan process.

6. The LSU guarantees loan approval. The LSU does not guarantee approval. It merely reflects the current status of the loan application and any conditions that need to be met.

7. All lenders follow the same timeline. Each lender may have different processes and timelines for completing loan updates and approvals, so timelines can vary significantly.

When filling out the Arizona Loan Status Update (LSU) form, there are several important points to keep in mind to ensure a smooth process. Here are ten key takeaways:

By following these guidelines, buyers can navigate the LSU process more effectively, ensuring that their loan status updates are accurate and timely.