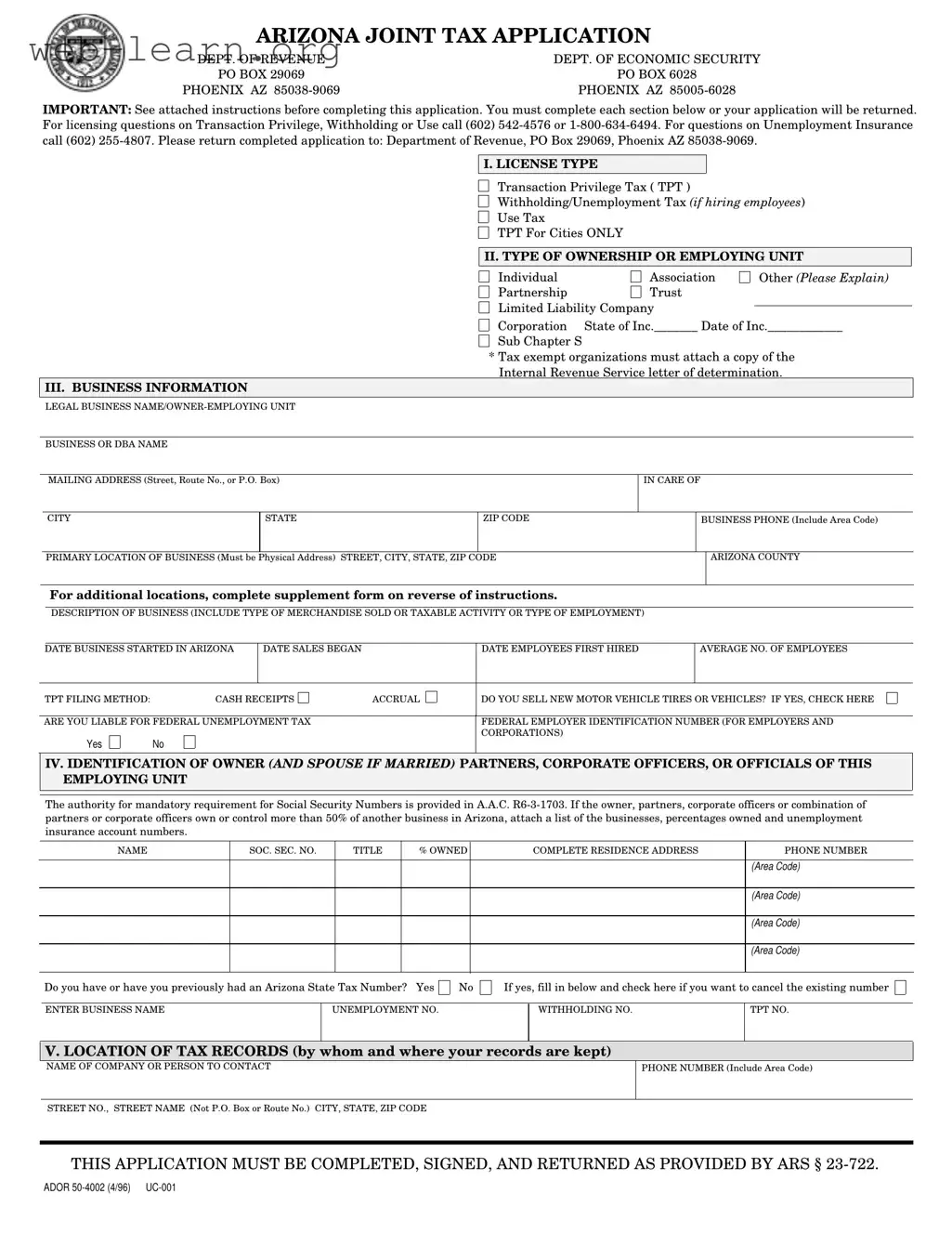

The Arizona Joint Tax Application form is a crucial document for businesses operating within the state. This form serves multiple purposes, including licensing new businesses, changing ownership structures, and ensuring compliance with various tax obligations. Applicants must select the appropriate license type, which may include Transaction Privilege Tax (TPT), Withholding/Unemployment Tax, or Use Tax. It is essential to accurately fill out each section, as incomplete applications will be returned. The form requires detailed business information, such as the legal business name, primary location, and a description of the business activities. Additionally, it asks for ownership details and the identification of key individuals involved in the business. This includes partners, corporate officers, and any previous owners if applicable. The form also outlines the fees associated with the TPT license and emphasizes the importance of signing the application under penalty of perjury. Understanding the requirements and completing the Arizona Joint Tax Application accurately is vital for businesses to operate legally and efficiently in Arizona.

| Fact Name | Details |

|---|---|

| Purpose | The Arizona Joint Tax Application is used for licensing new businesses, changing ownership, or updating existing business licenses. |

| Governing Law | This application is governed by Arizona Revised Statutes (ARS) § 23-722. |

| Contact Information | For questions regarding Transaction Privilege Tax, Withholding, or Use Tax, contact the Arizona Department of Revenue at (602) 542-4576 or 1-800-634-6494. |

| Required Information | Applicants must provide details such as legal business name, ownership type, business address, and tax identification numbers. |

| Fees | There is a fee of $12 per location for Transaction Privilege Tax licenses; no fees apply for Withholding, Use, or Unemployment Tax registrations. |

Completing the Arizona Joint Tax Application form is a straightforward process, but it requires attention to detail. Each section must be filled out accurately to avoid delays or rejections. Follow these steps carefully to ensure your application is submitted correctly.

The Arizona Joint Tax Application form is used to apply for various tax licenses, including Transaction Privilege Tax (TPT), Withholding Tax, and Unemployment Tax. It is necessary for businesses operating in Arizona to complete this application to ensure compliance with state tax regulations.

Any individual or entity planning to conduct business activities in Arizona that are subject to state taxes must complete this application. This includes new businesses, existing businesses changing ownership, or businesses adding locations.

The application requires detailed information, including:

There are no fees for Withholding, Unemployment, or Use Tax registrations. For Transaction Privilege Tax licenses, a fee of $12 per location applies, along with any applicable city fees. The total amount due must be calculated and submitted with the application.

The completed application should be mailed to the Arizona Department of Revenue at PO Box 29069, Phoenix, AZ 85038-9069. It is important to ensure that the application is signed and all sections are completed to avoid delays or rejections.

If you are acquiring an existing business, you must indicate this on the application and provide details about the previous owner. If you acquire all or part of the business, you may be eligible for the previous owner’s unemployment tax rate.

The description of the business is critical as it determines the transaction privilege tax rate applicable to your business. It also helps the state in economic forecasting and understanding the nature of business activities within Arizona.

Filling out the Arizona Joint Tax Application form can be a straightforward process, but there are common mistakes that applicants often make. Understanding these pitfalls can help ensure that your application is completed correctly and submitted without delays.

One frequent error is failing to complete all required sections. Each part of the application must be filled out; otherwise, the application will be returned. This includes providing accurate business information, ownership details, and tax identification numbers. Omitting even a small detail can lead to significant delays in processing.

Another common mistake is not providing the correct business name. Applicants often confuse the legal business name with the "doing business as" (DBA) name. It is crucial to enter the exact legal name as registered with the state, as discrepancies can cause complications with licensing.

Many applicants also overlook the importance of accurate contact information. Providing a mailing address that differs from the physical business location can create confusion. Ensure that the mailing address is current and clearly indicated to avoid miscommunication.

Inaccurate reporting of dates is another significant issue. Applicants frequently enter incorrect dates for when the business started or when sales began. These dates are essential for determining tax obligations and compliance, so they must be precise.

Misunderstanding the filing method can lead to errors as well. The application requires you to choose between cash receipts and accrual methods for tax reporting. Selecting the wrong method can affect how taxes are calculated and reported, leading to potential penalties.

Many applicants forget to include their federal employer identification number (EIN) when applying for unemployment tax coverage. This number is vital for identifying your business for tax purposes. Failing to provide it can delay the approval of your application.

Additionally, neglecting to sign the application can result in immediate rejection. The application must be signed by individuals legally responsible for the business. Ensure that all required signatures are present before submission.

Some individuals also mistakenly assume that they do not need to provide information about previous owners when acquiring an existing business. If applicable, this section must be completed to avoid complications with tax rates and liabilities.

Lastly, miscalculating fees can lead to delays in processing. Applicants must accurately calculate state and city fees based on the number of locations. Double-checking these calculations can prevent unnecessary complications and ensure timely processing of the application.

By being aware of these common mistakes, applicants can improve their chances of a smooth application process. Thoroughly reviewing the form and following the instructions can save time and reduce frustration.

The Arizona Joint Tax Application form is an essential document for businesses operating within the state. Alongside this form, several other documents are commonly required to ensure compliance with state tax regulations. Below is a list of these documents, each serving a specific purpose in the application process.

These documents play a crucial role in the tax application process in Arizona. Ensuring that all necessary forms are completed and submitted can help streamline the licensing and compliance process for businesses.

The Arizona Joint Tax Application form shares similarities with several other important documents related to business and tax registration. Each of these documents serves a specific purpose in the process of establishing and maintaining a business in Arizona. Below is a list of six documents that are similar to the Arizona Joint Tax Application form, along with an explanation of how they are alike.

When filling out the Arizona Joint Tax Application form, it’s essential to follow certain guidelines to ensure a smooth process. Here are some important dos and don'ts:

This form can also be used for changing ownership or updating existing business information.

All types of ownership, including partnerships and corporations, must fill out this form if they engage in taxable activities.

Only the Transaction Privilege Tax (TPT) incurs fees; there are no fees for withholding, use, or unemployment tax registrations.

Providing a Social Security Number is mandatory for owners and key officials as per Arizona regulations.

A physical address is required for the primary location of the business; P.O. Boxes are not acceptable.

The application must be signed by all individuals legally responsible for the business, not just one person.

This form is not for consolidating licenses; a separate update form must be requested for that purpose.

Previous state tax numbers must be disclosed on the application if applicable, especially if you wish to cancel them.

Each city may have different licensing requirements and fees, so it is important to check with local authorities.

Supporting documents, such as IRS letters for tax-exempt organizations, must be included if applicable.

Key Takeaways for Filling Out the Arizona Joint Tax Application Form

Following these guidelines will help streamline the application process and ensure compliance with Arizona tax regulations.