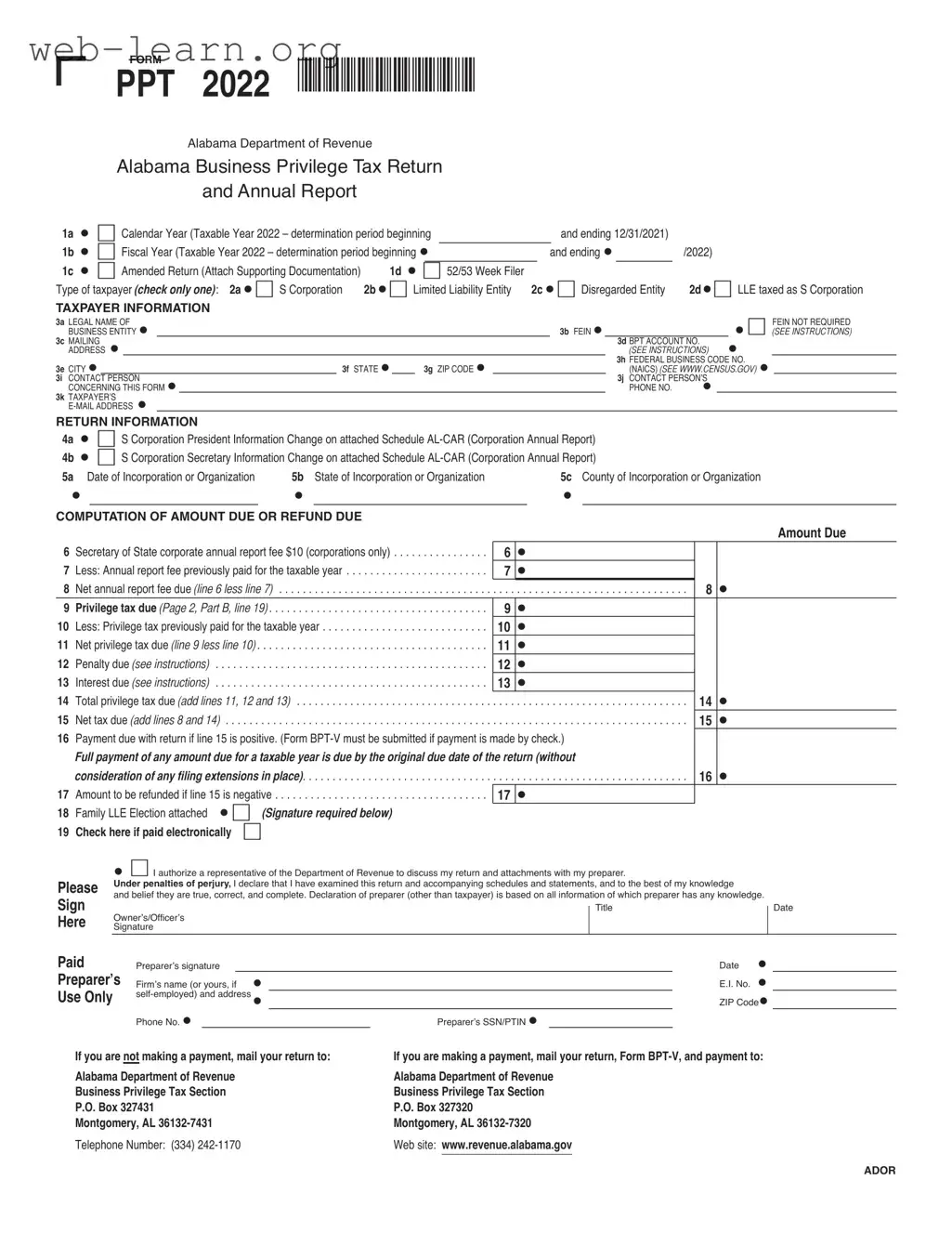

The Alabama Business Privilege Tax Return, commonly referred to as the Alabama PPT form, serves as a crucial document for various business entities operating within the state. This form is primarily used by S Corporations, Limited Liability Entities (LLEs), and Disregarded Entities to report their annual business privilege tax obligations. The form includes sections for taxpayer information, such as legal name, federal employer identification number (FEIN), and contact details, ensuring that the Alabama Department of Revenue can accurately process the return. Key components of the form also encompass the computation of amounts due or refunds, allowing businesses to calculate their net annual report fee and privilege tax due. Additionally, it provides a structured approach for reporting any changes in corporate officer information and includes provisions for penalties and interest on late payments. The Alabama PPT form must be submitted by the original due date of the return, with specific instructions for electronic payments and mailing addresses for submissions. Understanding the nuances of this form is essential for compliance and effective financial management for businesses in Alabama.

| Fact Name | Description |

|---|---|

| Form Title | Alabama Business Privilege Tax Return and Annual Report |

| Tax Year | This form is for the taxable year 2021, covering the determination period from January 1, 2021, to December 31, 2021. |

| Filing Types | Taxpayers can file as an S Corporation, Limited Liability Entity, Disregarded Entity, or an LLE taxed as an S Corporation. |

| Annual Report Fee | Corporations must pay a corporate annual report fee of $10 when filing this form. |

| Payment Due Date | Full payment of any amount due must be made by the original due date of the return, without considering any filing extensions. |

| Governing Law | The Alabama Business Privilege Tax is governed by Title 40, Chapter 14 of the Code of Alabama. |

| Contact Information | For inquiries, taxpayers can call the Alabama Department of Revenue at (334) 242-1170. |

Completing the Alabama PPT form is an important step for businesses to fulfill their tax obligations. Follow these steps carefully to ensure that all required information is accurately provided. Once the form is filled out, it must be submitted by the appropriate deadline to avoid any penalties.

The Alabama PPT form, or Business Privilege Tax Return and Annual Report, is a document that businesses in Alabama must file annually. This form is used to report the business privilege tax, which is a tax on the privilege of doing business in Alabama. It is essential for corporations and certain other entities to comply with state regulations and avoid penalties.

Generally, S Corporations, Limited Liability Entities (LLEs), and Disregarded Entities must file the Alabama PPT form. Each entity type has specific requirements and tax calculations. It is crucial to identify the correct type of taxpayer when completing the form to ensure compliance with Alabama tax laws.

Payments are due by the original due date of the return. If a business owes taxes, it must submit the payment along with the PPT form. Failure to pay on time can result in penalties and interest charges. If the amount due is negative, the taxpayer may be eligible for a refund.

The amount due is calculated by completing several sections of the form. Key components include:

Ensure that all previous payments are deducted from the total to determine the net amount due. Accurate calculations are critical to avoid issues with the Alabama Department of Revenue.

Filling out the Alabama Business Privilege Tax Return and Annual Report form can be a straightforward process, but mistakes often occur. One common error is failing to select the correct type of taxpayer. The form provides options such as S Corporation, Limited Liability Entity, and Disregarded Entity. Selecting the wrong option can lead to incorrect tax calculations and potential penalties.

Another frequent mistake involves providing incomplete or inaccurate taxpayer information. This includes the legal name of the business entity, Federal Employer Identification Number (FEIN), and contact details. Omissions or errors in this section can delay processing and result in miscommunication with the Alabama Department of Revenue.

Additionally, many individuals overlook the requirement to attach supporting documentation when necessary. For instance, if filing an amended return or claiming certain deductions, relevant documents must be included. Failing to provide these documents can lead to rejection of the return or the denial of deductions.

People also often miscalculate the amounts due or refund amounts. This can happen when individuals fail to correctly sum the figures on the form or neglect to account for previously paid taxes. Careful attention to each line item is essential to ensure accurate calculations and compliance with tax obligations.

Lastly, some filers neglect to sign the form before submission. A signature is required to validate the return and affirm that the information provided is true and complete. Without a signature, the form may be considered invalid, leading to further complications in the filing process.

The Alabama Business Privilege Tax Return, commonly referred to as the PPT form, is essential for various business entities operating in Alabama. Alongside this form, there are several other documents that businesses may need to file or reference to ensure compliance with state regulations. Below is a list of these forms and documents, each described to provide a clearer understanding of their purpose.

Understanding these forms and their purposes is vital for businesses to navigate the tax landscape in Alabama effectively. Properly completing and submitting the required documents can help ensure compliance and avoid potential penalties.

IRS Form 1065: This form is used by partnerships to report income, deductions, gains, and losses. Like the Alabama PPT form, it requires detailed information about the entity's financial status and tax obligations.

IRS Form 1120S: This form is for S Corporations to report income and expenses. Similar to the Alabama PPT form, it includes sections for reporting tax due and information about shareholders.

Alabama Corporate Income Tax Return (Form 20C): Corporations in Alabama use this form to report income and calculate tax liability. Both forms require details on business income and deductions to determine tax obligations.

Alabama Annual Report (Form BPT): This report is required for businesses operating in Alabama and is similar in that it collects information about the business's financial activities and status for the year.

State Business License Application: This application is necessary for businesses to operate legally within Alabama. Like the Alabama PPT form, it requires information about the business structure and operations.

Alabama Sales Tax Return (Form ST-1): Businesses use this form to report and pay sales tax. Both forms require accurate reporting of financial data and compliance with state regulations.

When filling out the Alabama Business Privilege Tax Return and Annual Report (PPT form), it is essential to follow certain guidelines to ensure accuracy and compliance. Below is a list of dos and don'ts that can help streamline the process.

Adhering to these guidelines can help avoid common pitfalls and ensure that the filing process goes smoothly. Always double-check your entries for accuracy and completeness before submission.

This form is applicable to various entities, including S Corporations, Limited Liability Entities (LLEs), and Disregarded Entities. Each type of entity has specific requirements, but all must comply with the form's regulations.

Filing the form does not automatically result in a refund. The amount due or refund is determined by the calculations on the form. If the net tax due is positive, payment is required.

Full payment of any amount due must be made by the original due date of the return. Extensions do not apply to payment deadlines, so timely submission is crucial to avoid penalties.

All qualifying entities, regardless of revenue, must file the PPT form if they fall under the specified categories. Even minimal income can trigger a filing requirement.

Key Takeaways for Filling Out and Using the Alabama PPT Form