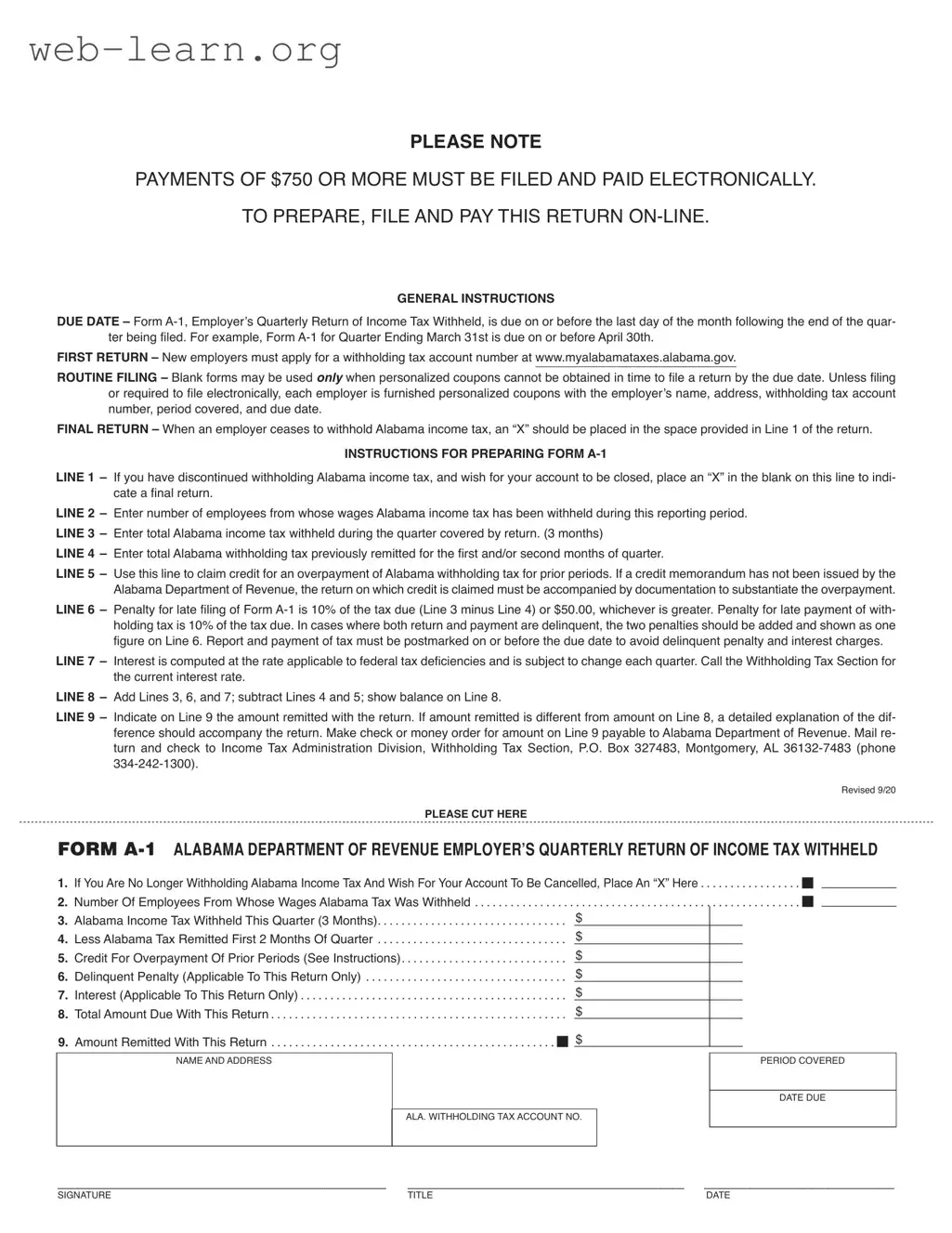

The Alabama A-1 form serves as the Employer’s Quarterly Return of Income Tax Withheld, an essential document for employers in Alabama to report the income tax withheld from their employees' wages. This form must be filed electronically for payments of $750 or more, ensuring a streamlined process for both employers and the state. Each quarter, employers are required to submit this form by the last day of the month following the end of the quarter. For instance, if the quarter ends on March 31st, the form is due by April 30th. New employers need to establish a withholding tax account number before they can file. The A-1 form includes several lines where employers report critical information, such as the number of employees from whom tax was withheld, the total amount of tax withheld during the quarter, and any penalties or interest due for late filing. Additionally, if an employer ceases to withhold Alabama income tax, they can indicate this by marking the appropriate box on the form. Proper completion of the A-1 form is crucial, as inaccuracies can lead to penalties. Understanding these requirements helps ensure compliance and facilitates smooth tax reporting.

| Fact Name | Description |

|---|---|

| Electronic Filing Requirement | Payments of $750 or more must be filed and paid electronically. |

| Due Date | Form A-1 is due on or before the last day of the month following the end of the quarter being filed. |

| New Employer Registration | New employers must apply for a withholding tax account number through the Alabama Department of Revenue's website. |

| Final Return Indication | Employers must place an “X” in Line 1 if they have ceased to withhold Alabama income tax. |

| Penalty for Late Filing | A penalty of 10% of the tax due or $50.00, whichever is greater, applies for late filing of Form A-1. |

Filling out the Alabama A-1 form is an important task for employers who need to report income tax withheld from employees' wages. Following the correct steps ensures compliance with state regulations and helps avoid penalties. Below are the steps to accurately complete the form.

What is the Alabama A-1 Form?

The Alabama A-1 Form is the Employer’s Quarterly Return of Income Tax Withheld. Employers use this form to report the amount of Alabama income tax withheld from employees' wages during a quarter. It is essential for maintaining compliance with Alabama tax regulations.

When is the A-1 Form due?

The A-1 Form is due on or before the last day of the month following the end of the quarter being reported. For instance, if you are reporting for the quarter ending March 31st, the form must be submitted by April 30th.

How can new employers obtain a withholding tax account number?

New employers must apply for a withholding tax account number through the Alabama Department of Revenue's website at www.myalabamataxes.alabama.gov. This account number is necessary to file the A-1 Form.

What should I do if I am no longer withholding Alabama income tax?

If you have ceased withholding Alabama income tax, you must indicate this on Line 1 of the A-1 Form by placing an "X" in the designated space. This action will signal the Alabama Department of Revenue to close your withholding account.

What are the penalties for late filing and payment?

For late filing, a penalty of 10% of the tax due (calculated as Line 3 minus Line 4) or a minimum of $50.00 will apply, whichever is greater. Late payment incurs a similar 10% penalty. If both the return and payment are late, both penalties are combined and shown as one total on Line 6.

How is interest on late payments calculated?

Interest on late payments is computed at the rate applicable to federal tax deficiencies. This rate may change quarterly, so it is advisable to contact the Withholding Tax Section for the current interest rate.

What information do I need to complete the A-1 Form?

Where do I send the completed A-1 Form and payment?

Mail the completed A-1 Form along with your payment to the following address: Income Tax Administration Division, Withholding Tax Section, P.O. Box 327483, Montgomery, AL 36132-7483. Ensure your payment is made out to the Alabama Department of Revenue.

Can I file the A-1 Form electronically?

Yes, employers must file and pay electronically if the payment is $750 or more. The Alabama Department of Revenue provides an online platform for preparing, filing, and paying the A-1 Form.

Filling out the Alabama A-1 form can seem straightforward, but many people make common mistakes that can lead to delays or penalties. One frequent error is not submitting the form electronically when required. If your payment is $750 or more, it must be filed and paid electronically. Ignoring this requirement can result in complications and potential fines.

Another common mistake is missing the due date. The A-1 form is due on the last day of the month following the end of the quarter. For example, if the quarter ends on March 31st, the form must be submitted by April 30th. Failing to meet this deadline can lead to late penalties, which can be costly.

Many individuals also overlook the necessity of applying for a withholding tax account number if they are new employers. This step is crucial, and without it, you cannot properly fill out the form. Make sure to register at www.myalabamataxes.alabama.gov before attempting to file.

When it comes to the details on the form, inaccuracies can be a big issue. For instance, some people forget to fill in the number of employees from whom Alabama income tax has been withheld in Line 2. This information is essential for the state to process your return accurately.

Another mistake occurs on Line 3, where individuals might miscalculate the total Alabama income tax withheld during the quarter. It’s important to double-check your figures to avoid discrepancies that could lead to further complications.

Claiming a credit for overpayment on Line 5 can also trip people up. If you haven’t received a credit memorandum from the Alabama Department of Revenue, you must include documentation to support your claim. Failing to do so can result in your return being flagged or delayed.

In addition, some filers neglect to account for penalties and interest on Lines 6 and 7. It’s essential to understand that these can add up quickly if your return or payment is late. Always calculate these amounts accurately to avoid surprises.

Another common oversight is not providing a detailed explanation when the amount remitted on Line 9 differs from the total due on Line 8. This can raise red flags with the tax authorities and may result in further inquiries.

Finally, many people forget to mail their return and payment to the correct address. Ensure that you send it to the Income Tax Administration Division, Withholding Tax Section, at the specified P.O. Box in Montgomery. A simple mistake in the mailing address can lead to delays in processing your return.

By being aware of these common mistakes, you can navigate the Alabama A-1 form with greater confidence and accuracy. Take your time, review your entries, and ensure you meet all requirements to avoid unnecessary issues.

When filing the Alabama A-1 form, several other documents and forms may be required to ensure compliance with state regulations. Each of these forms serves a specific purpose in the reporting and payment process. Below is a list of commonly used forms alongside the Alabama A-1 form.

Understanding these forms and their purposes is crucial for compliance with Alabama tax regulations. Timely and accurate filing can help avoid penalties and ensure that employees receive their proper tax documentation. Always consult with a tax professional or legal advisor if there are any uncertainties about the filing process.

When filling out the Alabama A-1 form, it is crucial to follow specific guidelines to ensure your submission is accurate and timely. Here are five important do's and don'ts to keep in mind:

Following these guidelines will help you avoid unnecessary penalties and ensure your filing process is smooth. Act promptly to meet all deadlines and requirements.

Understanding the Alabama A-1 form is crucial for employers in Alabama. However, there are several misconceptions that can lead to confusion. Here are ten common misunderstandings:

Being informed about these misconceptions can help employers navigate their responsibilities more effectively and avoid unnecessary penalties.

Here are key takeaways regarding the Alabama A-1 form: